Answered step by step

Verified Expert Solution

Question

1 Approved Answer

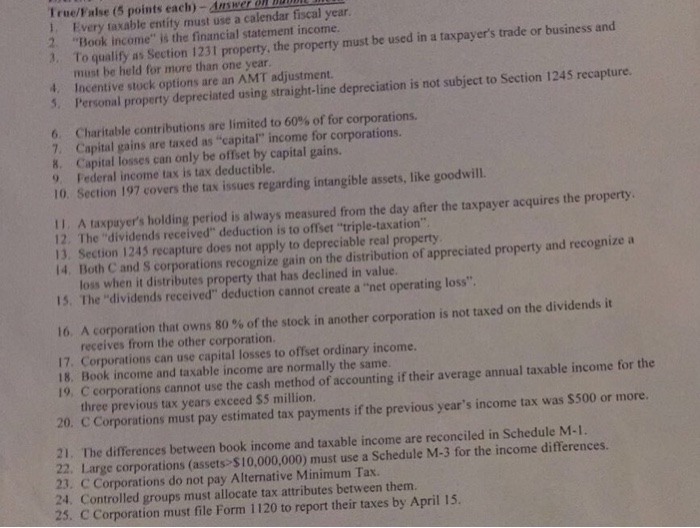

True/False (5 points each)-Answer 1, Every taxable entity must use a calendar fiscal year 2. Book income is the financial statement income. J. To qualifty

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Principles And Practice Of Auditing

Authors: George Puttick, Sandra Van Esch

7th Edition

0702137723, 978-0702137723