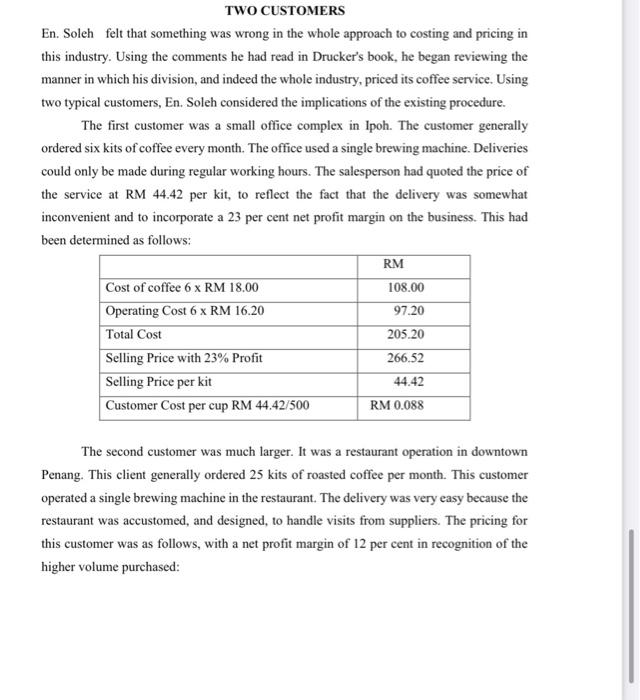

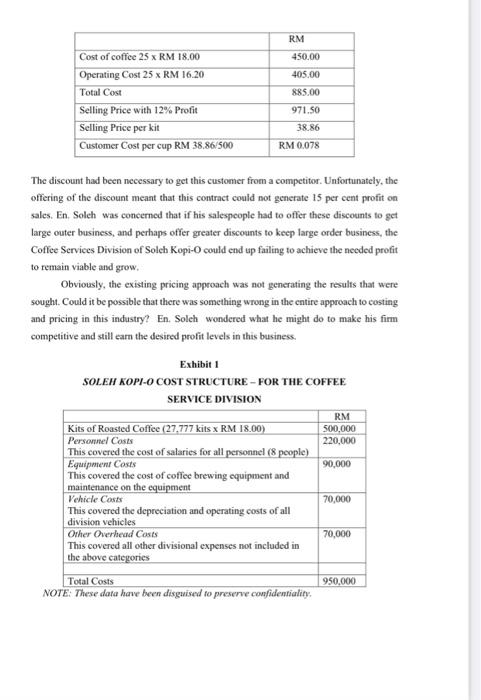

TWO CUSTOMERS En. Soleh felt that something was wrong in the whole approach to costing and pricing in this industry. Using the comments he had read in Drucker's book, he began reviewing the manner in which his division, and indeed the whole industry, priced its coffee service. Using two typical customers, En. Soleh considered the implications of the existing procedure. The first customer was a small office complex in Ipoh. The customer generally ordered six kits of coffee every month. The office used a single brewing machine. Deliveries could only be made during regular working hours. The salesperson had quoted the price of the service at RM 44.42 per kit, to reflect the fact that the delivery was somewhat inconvenient and to incorporate a 23 per cent net profit margin on the business. This had been determined as follows: RM Cost of coffee 6 x RM 18.00 108.00 Operating Cost 6 x RM 16.20 97.20 Total Cost 205.20 Selling Price with 23% Profit 266.52 Selling Price per kit 44.42 Customer Cost per cup RM 44.42/500 RM 0.088 The second customer was much larger. It was a restaurant operation in downtown Penang. This client generally ordered 25 kits of roasted coffee per month. This customer operated a single brewing machine in the restaurant. The delivery was very easy because the restaurant was accustomed, and designed, to handle visits from suppliers. The pricing for this customer was as follows, with a net profit margin of 12 per cent in recognition of the higher volume purchased: RM 450.00 405.00 885.00 Cost of coffee 25 x RM 18.00 Operating Cost 25 x RM 16.20 Total Cost Selling Price with 12% Profit Selling Price per kit Customer Cost per cup RM 38,86/500 971.50 38.86 RM 0.078 The discount had been necessary to get this customer from a competitor. Unfortunately, the offering of the discount meant that this contract could not generate 15 per cent profit on sales. En. Soleh was concerned that if his salespeople had to offer these discounts to get large outer business, and perhaps offer greater discounts to keep large order business, the Coffee Services Division of Solch Kopi-O could end up failing to achieve the needed profit to remain viable and grow. Obviously, the existing pricing approach was not generating the results that were sought. Could it be possible that there was something wrong in the entire approach to costing and pricing in this industry? En Soleh wondered what he might do to make his firm competitive and still earn the desired profit levels in this business. Exhibiti SOLEH KOPI-O COST STRUCTURE - FOR THE COFFEE SERVICE DIVISION RM 500,000 220,000 90,000 70,000 Kits of Roasted Coffee (27.777 kits x RM 18.00) Personnel Costs This covered the cost of salaries for all personnel (8 people) Equipment Costs This covered the cost of coffee brewing equipment and maintenance on the equipment Vehicle Costs This covered the depreciation and operating costs of all division vehicles Other Overhead Costs This covered all other divisional expenses not included in the above categories Total Costs NOTE: These data have been disguised to preserve confidentiality 70,000 950.000 (b) Refer to En. Soleh's analysis of the two typical customers. In your opinion, what is the main problem with the existing costing and pricing approach used by En. Soleh? Explain. were the matter you stated Pain TWO CUSTOMERS En. Soleh felt that something was wrong in the whole approach to costing and pricing in this industry. Using the comments he had read in Drucker's book, he began reviewing the manner in which his division, and indeed the whole industry, priced its coffee service. Using two typical customers, En. Soleh considered the implications of the existing procedure. The first customer was a small office complex in Ipoh. The customer generally ordered six kits of coffee every month. The office used a single brewing machine. Deliveries could only be made during regular working hours. The salesperson had quoted the price of the service at RM 44.42 per kit, to reflect the fact that the delivery was somewhat inconvenient and to incorporate a 23 per cent net profit margin on the business. This had been determined as follows: RM Cost of coffee 6 x RM 18.00 108.00 Operating Cost 6 x RM 16.20 97.20 Total Cost 205.20 Selling Price with 23% Profit 266.52 Selling Price per kit 44.42 Customer Cost per cup RM 44.42/500 RM 0.088 The second customer was much larger. It was a restaurant operation in downtown Penang. This client generally ordered 25 kits of roasted coffee per month. This customer operated a single brewing machine in the restaurant. The delivery was very easy because the restaurant was accustomed, and designed, to handle visits from suppliers. The pricing for this customer was as follows, with a net profit margin of 12 per cent in recognition of the higher volume purchased: RM 450.00 405.00 885.00 Cost of coffee 25 x RM 18.00 Operating Cost 25 x RM 16.20 Total Cost Selling Price with 12% Profit Selling Price per kit Customer Cost per cup RM 38,86/500 971.50 38.86 RM 0.078 The discount had been necessary to get this customer from a competitor. Unfortunately, the offering of the discount meant that this contract could not generate 15 per cent profit on sales. En. Soleh was concerned that if his salespeople had to offer these discounts to get large outer business, and perhaps offer greater discounts to keep large order business, the Coffee Services Division of Solch Kopi-O could end up failing to achieve the needed profit to remain viable and grow. Obviously, the existing pricing approach was not generating the results that were sought. Could it be possible that there was something wrong in the entire approach to costing and pricing in this industry? En Soleh wondered what he might do to make his firm competitive and still earn the desired profit levels in this business. Exhibiti SOLEH KOPI-O COST STRUCTURE - FOR THE COFFEE SERVICE DIVISION RM 500,000 220,000 90,000 70,000 Kits of Roasted Coffee (27.777 kits x RM 18.00) Personnel Costs This covered the cost of salaries for all personnel (8 people) Equipment Costs This covered the cost of coffee brewing equipment and maintenance on the equipment Vehicle Costs This covered the depreciation and operating costs of all division vehicles Other Overhead Costs This covered all other divisional expenses not included in the above categories Total Costs NOTE: These data have been disguised to preserve confidentiality 70,000 950.000 (b) Refer to En. Soleh's analysis of the two typical customers. In your opinion, what is the main problem with the existing costing and pricing approach used by En. Soleh? Explain. were the matter you stated Pain