Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Two securities, B1 and B2 are trading in the economy and their payoff structure and prices are given in the above. Suppose that annualized continuously

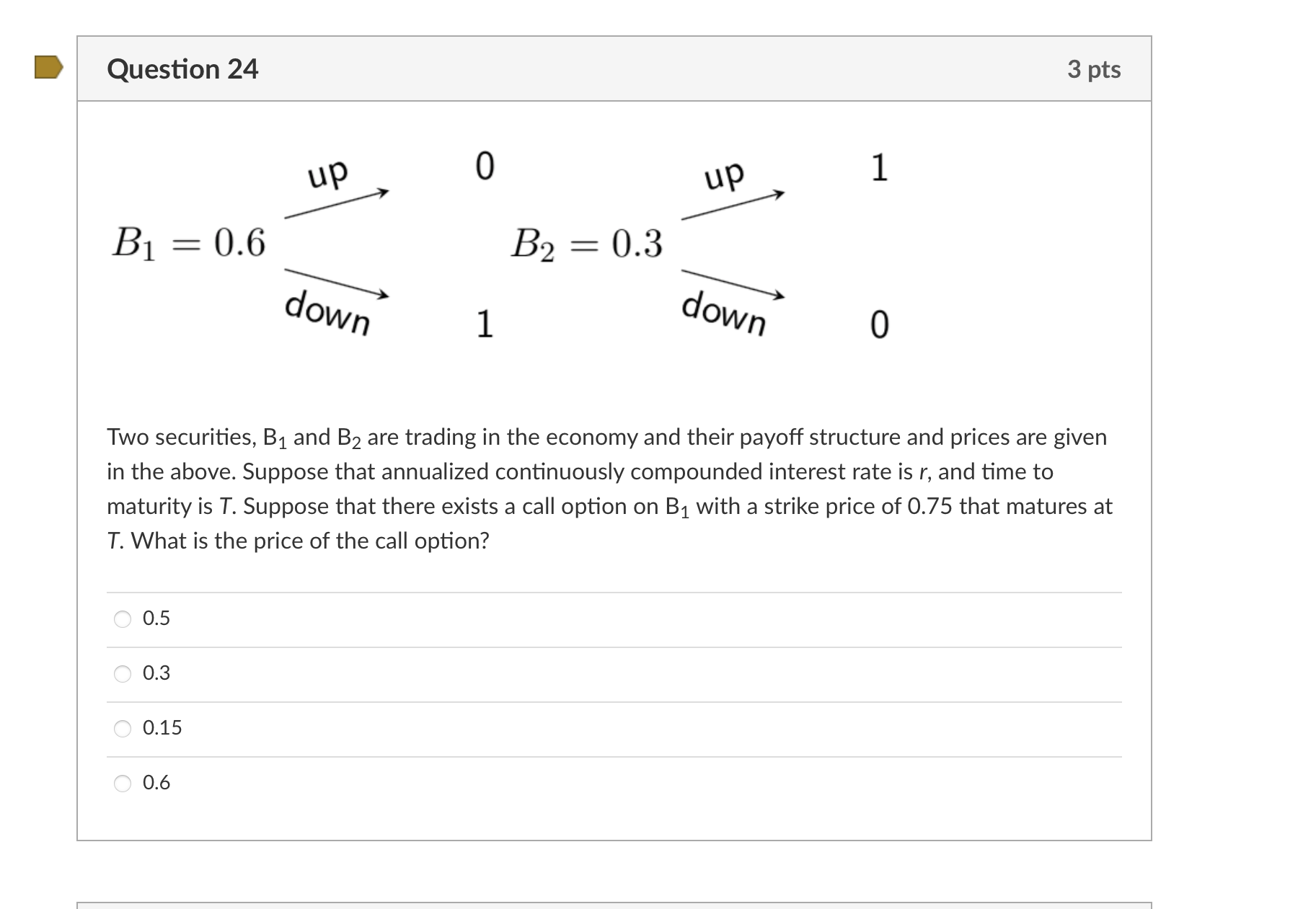

Two securities, B1 and B2 are trading in the economy and their payoff structure and prices are given in the above. Suppose that annualized continuously compounded interest rate is r, and time to maturity is T. Suppose that there exists a call option on B1 with a strike price of 0.75 that matures at T. What is the price of the call option? 0.5 0.3 0.15

Two securities, B1 and B2 are trading in the economy and their payoff structure and prices are given in the above. Suppose that annualized continuously compounded interest rate is r, and time to maturity is T. Suppose that there exists a call option on B1 with a strike price of 0.75 that matures at T. What is the price of the call option? 0.5 0.3 0.15 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Handbook Of Mutual Fund Investing

Authors: Barry G Dolgin

1st Edition

1456489704, 978-1456489700