Answered step by step

Verified Expert Solution

Question

1 Approved Answer

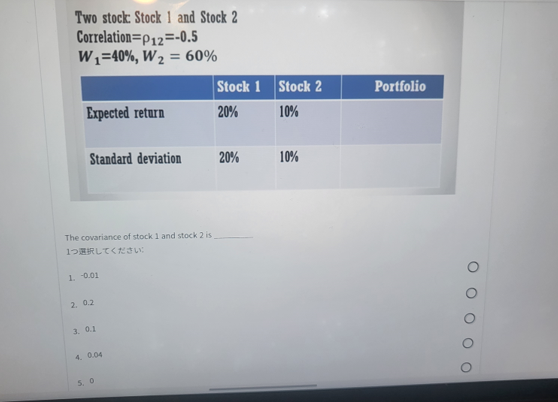

Two stock: Stock 1 and Stock 2 Correlation =12=0.5 W1=40%,W2=60% The covariance of stock 1 and stock 2 is 1: 1. -0.01 2. 0.2 3.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Impact Of Aircraft Sourcing And Financing On Financial Success A Strategic View On Basic Aircraft Sourcing And Financing Characteristics And Their Impact On A Stock Market And Long Term Financial Performance Of A Aircraft Operating And Holding Companies

Authors: Ralf Günther

1st Edition

3658240938,3658240946