Answered step by step

Verified Expert Solution

Question

1 Approved Answer

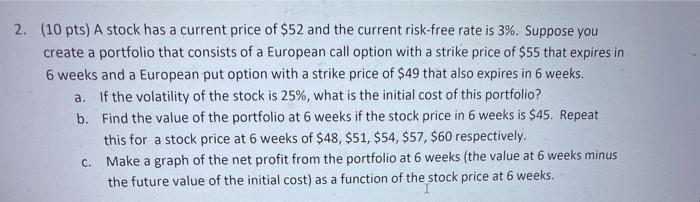

u can use R to make the graph 2. (10 pts) A stock has a current price of $52 and the current risk-free rate is

u can use R to make the graph

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Petromania Black Gold Paper Barrels And Oil Price Bubbles

Authors: Daniel O'Sullivan

1st Edition

1906659249,190665977X