Answered step by step

Verified Expert Solution

Question

1 Approved Answer

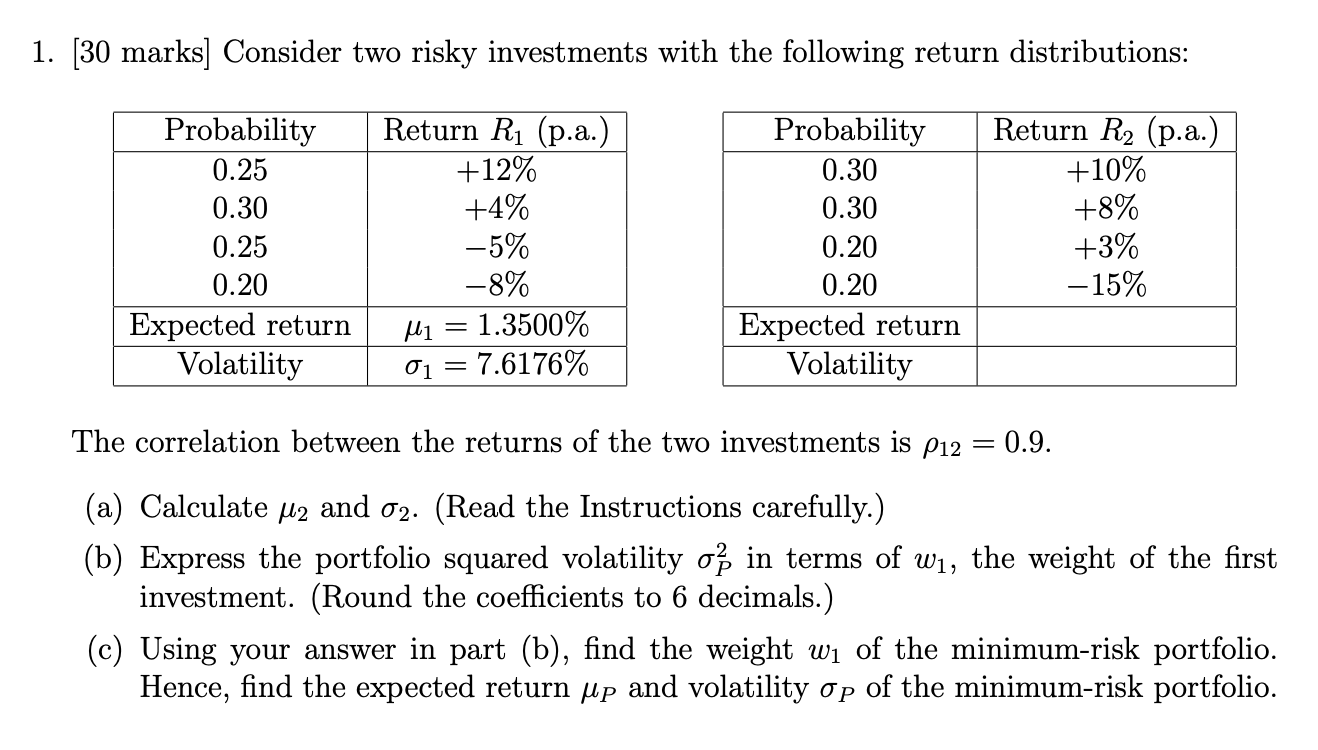

undefined 1. [30 marks] Consider two risky investments with the following return distributions: Probability 0.25 0.30 0.25 0.20 Expected return Volatility Return R1 (p.a.) +12%

undefined

undefined

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Protecting Main Street Measuring The Customer Experience In Financial Services For Business And Public Policy

Authors: Paul C. Lubin

1st Edition

1138864161,1136902546