Question

Under real world probability measure P, stock prices follow the two-step binomial tree processes. At each step, the stock moves up with probability 0.5, and

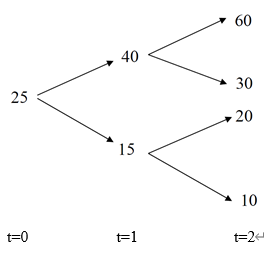

Under real world probability measure P, stock prices follow the two-step binomial tree processes. At each step, the stock moves up with probability 0.5, and moves down with probability 0.5. Assume that the risk-free interest rate is zero. For a European call option on this stock, let maturity T=2 and strike price K=25.

1Calculate the risk neutral probability for each path in the binomial tree.

2Calculate the option prices at time 0 and 1.

3Suppose Q is risk neutral measure, calculate Radon-Nikodym derivatives dQ/dP for each state.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

QFinance The Ultimate Resource

Authors: Various Authors

1st Edition

1849300003, 978-1849300001