Urika Corp. manufactures a variety of kitchen and dining equipment from mixers and food processors to flatware, serving utensils, cooking utensils, and other items for

Urika Corp. manufactures a variety of kitchen and dining equipment from mixers and food processors to flatware, serving utensils, cooking utensils, and other items for consumer and commercial use. Urika went public in 1984 at $27/share on the market (netting $23/share for the firm) and began issuing dividends in 1990 without missing a year since then. Due to their low debt and wise reinvestment of earnings, today the company’s stock sells for $200/share.

As the company prepares for the next year, the President has tasked the senior leadership with finding major expansion projects in order take market share from industry leaders such as GE and Whirlpool’s subsidiary, KitchenAid. Over the past 5 years, the company has accumulated significant amounts of cash and other marketable assets to fund this expansion without materially affecting the firm’s debt or diluting the stockholder’s equity. The CFO has determined $22,500,000 will available in the 2012 capital budget to fund these new projects.

One project involves building the plant and equipment to equip and supply a new up-and-coming restaurant chain, Fast ‘N’ Healthy, which has been making great strides at competing with fast-food chains along the West coast, and wants to re-equip and re-model existing stores and open 200 new stores nationwide over the next four years. Mr. Tony Estabal, Senior Vice President for Business Development at Urika is certain Urika will secure the four-year contract with Fast ‘N’ Healthy due to Urika’s previous successful work with the restaurant, their cost savings measures, and their experience and reputation within the industry. To compete with other bidders, Urika is able to provide some cost breaks to the restaurant chain for other kitchen and dining supplies because Urika’s main plant is located near the restaurant chain’s main distribution warehouse. Even if Urika cannot under-bid competitors on price alone, other value-added benefits such as their existing relationship, reputation in the industry, and location would edge them over the competition. There is little to no risk of not securing this contract; therefore, this project has been given a priority “green light” status by the President and the corporation’s board.

PART 1 – PROJECT CBA MODELING

Urika would need to invest an estimated $6,786,000 for plant and equipment that would depreciate over 30 years. Although Urika would probably continue using the plant and equipment for future endeavors and further expansion by Fast ‘N’ Healthy, Tony has been instructed to make sure this project can stand on its own merits; therefore, a salvage or re-sale value for the Plant & Equipment has been estimated at $4,875,000 to be used as part of the exit strategy at termination of the contract.

Urika would also need to initially invest another $175,000 in working capital for materials. As the restaurant chain expands, Urika would need to ramp up manufacturing so that Working Capital is maintained at about 15% of Gross Revenues from the restaurant at the end of each period. Likewise, Direct Materials will cost about 15% of Gross Revenues. Since Urika hopes to continue this operation after the four years, the company will plan on having $450,000 in working capital at the end of four years, but this could be sold at book value if the operations cease.

The operation of the equipment from start to finish is expected to require six employees with a fully loaded (salaries, bonuses, benefits, taxes, etc.) cost of labor (COL) at about $74,250/year each. Tony wants to plan for 3% annual increases in the base COL.

Since this operation will be working at only about 50% of capacity in year one, additional labor will not be needed for the full four years of operations. However, by year three, estimated overtime will add another $.145 (or 14.5%) of every $1 of marginal revenue over $2.5M to the total COL (in other words, overtime for up to $2.5M in revenue = $0, but overtime for $2,500,001 is $0.145).

Overhead charged to the cost of goods sold will be assigned at a rate of 4% of Gross Revenue.

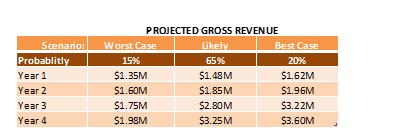

Because success of the restaurant’s expansion can affect the profitability as well as the scale of the projects, marketing analysts have provided the following revenue forecast for Urika based on the restaurant owner’s previous success and extensive market analysis. Mr. Estabal has asked you to weight Urika’s expected revenue streams based on the following:

Your Assignment:

PART 1 – COST BENEFIT ANALYSIS (20 points possible)

Create a cost-benefit analysis model of the project based on the above information to calculate the NPV and IRR to show that this project is worth pursuing. Since any of the values and rates provided above could change, make sure you provide a single point of input that will re-calculate the results if any of the assumptions change, including the estimate revenues and the probabilities of those revenues. You’ll also want to provide immediate feedback of key results so that if a manager changes one variable, he or she can immediately see the impact to key metrics.

Urika’s tax rate is currently 32% and their Weighted Average Cost of Capital is 5.5%. Urika’s CFO will not accept a project unless the IRR can hurdle 12%.

For this exercise, depreciate Plant & Equipment as if there will be no salvage value on a straight-line basis.

PART 2 – SCENARIO ANALYSIS (10 points)

Using your model from above, now create a scenario analysis report showing the yearly cash flows, NPV and IRR for the mutually exclusive scenarios that follow:

Scenario 1: The Probabilities for Worst, Probable and Best change to 25%/50%/25%

Scenario 2: Working Capital is changed to 18%

Scenario 3: Overtime changes to a 25% increase (vs. the 14.5%) per $1 of additional revenue

Scenario 4: P&E changes to $8.5M

Scenario 5: The Ultimate Worst Case: all four of the above at once.

PART 3 – FINANCIAL FORECASTING (20 points)

Using the historical financial statements provided, create pro forma financial statements of Urika Corporation using the following information for status quo operations and with the Fast ‘N’ Health project layered in as well.

For status quo, use the following assumptions or techniques:

1. Grow sales by 7% annually

2. Use the average percentage of sales to determine the cost of goods sold for current operations, then add the calculated cost of goods sold from the project’s CBA.

3. Use the Excel function TREND to determine Cash and SG&A using historical Sales as the independent variable (do not apply this to sales including Fast ‘N’ Healthy since all of the SG&A costs are already included in the project’s revenue stream).

4. Use the current Cost of Capital to determine the Interest Expense on debt and apply this to the average of LAST and CURRENT years’ balance is Notes, Current Portion of LT Debt, and LT Debt.

5. Use TREND to determine Accounts Receivable and Inventories with Sales as the independent variable; for this calculation, DO use total sales including revenue from the Fast ‘N’ Healthy project.

6. Include the project’s PP&E with the status quo’s PP&E.

7. Depreciation for status quo PP&E will be $5,855,000/year for all out-years. PLUS: Don’t forget to add depreciation from Fast ‘N’ Healthy to this.

8. Assume Other Non Current Assets are $35,000,000 flat for all out-years.

9. Assume $2M flat for Accounts Payable for all out-years.

10. Use the prior 5 years average Accrued Expenses, Notes Payable, and Other Non Current Liabilities, and keep them flat for all out-years.

11. Use $300,000 for the Current Portion of Long Term Debt, unless there is no long term debt

12. Long Term Debt – Reduce by the $300,000 Current Portion of Long Term Debt every year.

13. Other Non Current Liabilities – use the average of prior years and keep that flat.

14. Additional Paid-in-Capital is not expected to change at this point.

15. For Retained Earnings: determine the dividends paid in prior periods. Urika would like to grow dividends by 4% annually going forward.

16. Use Other Current Assets as appropriate as a plug to balance the Balance Sheet using the method I show you in class. ASK IF YOU DON’T KNOW!

Don’t forget to add in the effects of the Fast ‘N’ Healthy project.

Make sure your model and financial statements are professional in appearance and easy to navigate. Remember, a Senior Vice President will want to see and use your work when you’re finished!

PROJECTED GROSS REVENUE Worst Case Scenario: Probablitly Likely Best Case 15% $1.35M 65% 20% Year 1 $1.48M $1.62M Year 2 $1.60M $1.85M $1.96M Year 3 $1.75M $2.80M $3.22M Year 4 $1.98M $3.25M $3.60M

Step by Step Solution

3.45 Rating (155 Votes )

There are 3 Steps involved in it

Step: 1

Ans The data in the case is as tabulated below Plant and Equipment 6786000 Depreciation 30 Years SLM Salvage value 4875000 Value of plant for 4 yrs 1911000 Initial WC 175000 Of Gross Revenue from Hote...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Douglas Lind, William Marchal

16th Edition

78020522, 978-0078020520