Answered step by step

Verified Expert Solution

Question

1 Approved Answer

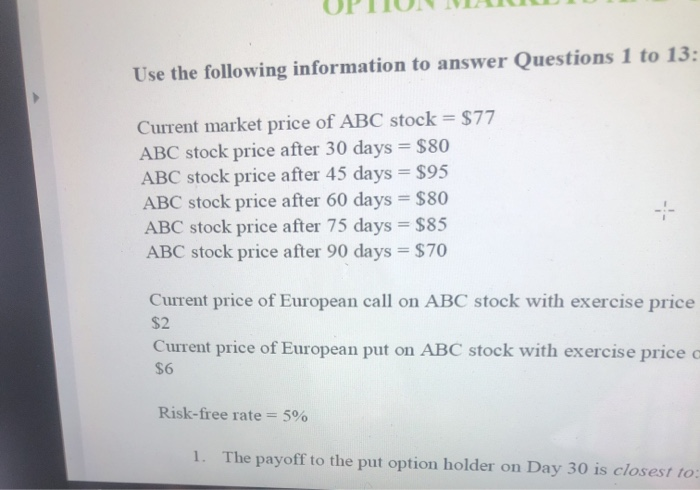

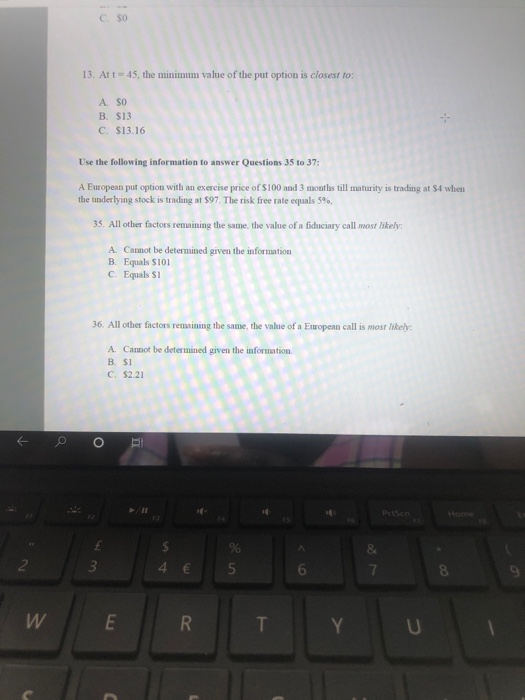

UPTIUNWATU Use the following information to answer Questions 1 to 13: Current market price of ABC stock = $77 ABC stock price after 30 days

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Report Of Johnstown Flood Finance Committee

Authors: Johnstown (Pa.) Flood Finance Committee, YA Pamphlet Collection

1st Edition

1246561557, 9781246561555