Answered step by step

Verified Expert Solution

Question

1 Approved Answer

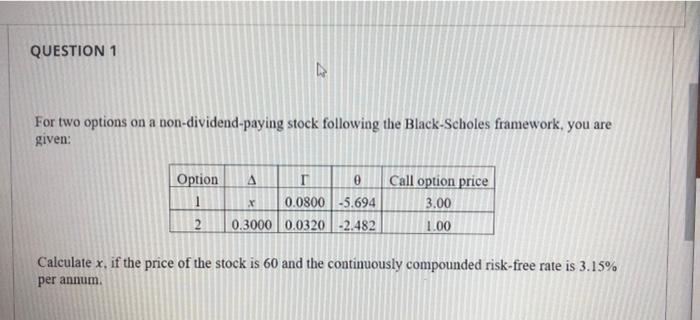

URGENT PLZ I WILL UPVOTE THANKS QUESTION 1 For two options on a non-dividend-paying stock following the Black-Scholes framework, you are given: Option 1 A

URGENT PLZ I WILL UPVOTE THANKS

QUESTION 1 For two options on a non-dividend-paying stock following the Black-Scholes framework, you are given: Option 1 A 0 Call option price x 0.0800-5.694 3.00 0.30000.0320-2.482 1.00 2. Calculate x, if the price of the stock is 60 and the continuously compounded risk-free rate is 3.15% per annum QUESTION 1 For two options on a non-dividend-paying stock following the Black-Scholes framework, you are given: Option 1 A 0 Call option price x 0.0800-5.694 3.00 0.30000.0320-2.482 1.00 2. Calculate x, if the price of the stock is 60 and the continuously compounded risk-free rate is 3.15% per annum

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fighting Fraud And Corruption At The World Bank A Critical Analysis Of The Sanctions System

Authors: Stefano Manacorda , Costantino Grasso

1st Edition

3319738232,3319738240