Question

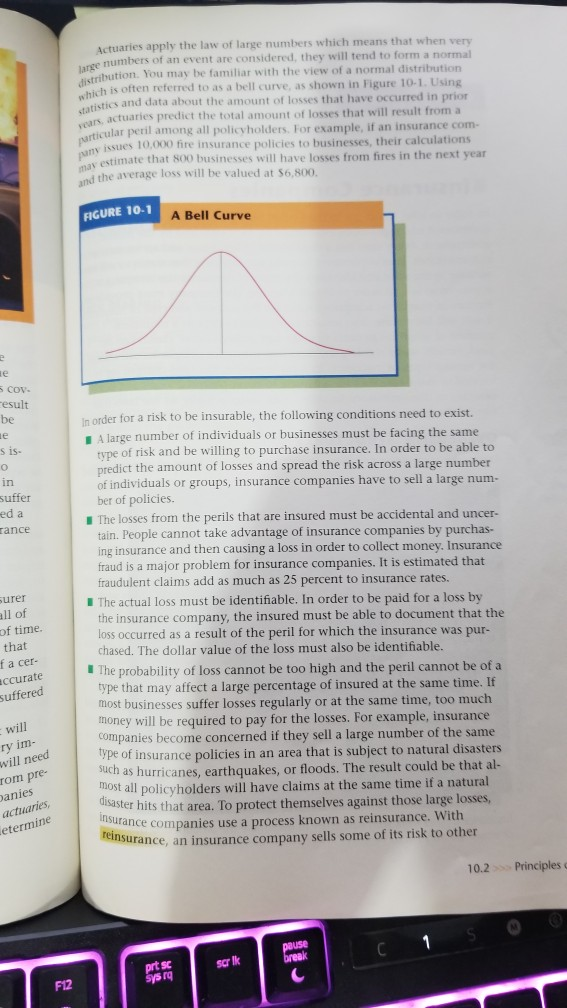

Use Figure 10-1 to describe how a bell curve represents the number and amount of damages that are likely to result from the number of

Use Figure 10-1 to describe how a bell curve represents the number and amount of damages that are likely to result from the number of fires that occur in a large number of businesses over several years. typing please. thank you.)

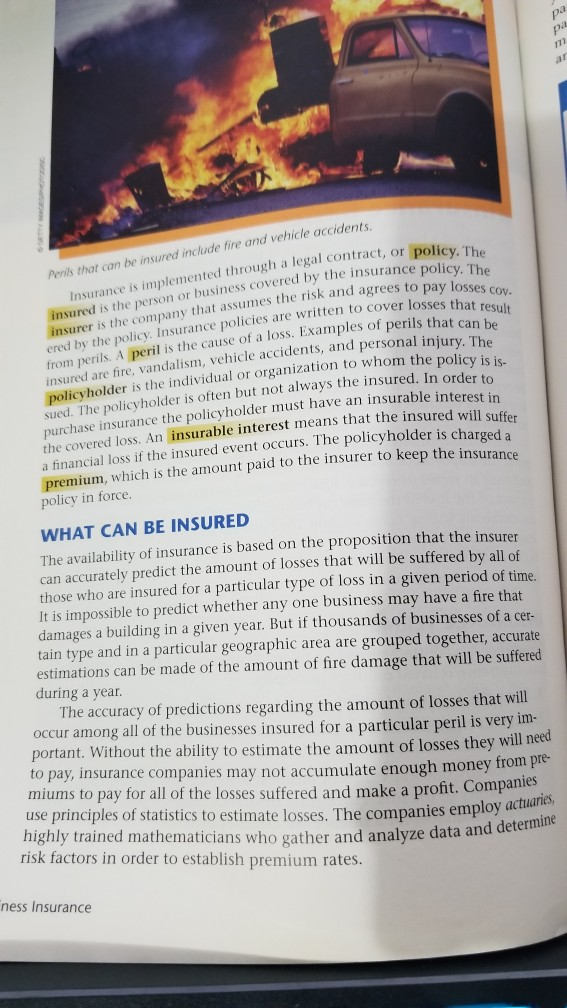

pa pa al Perils that can be insured include fire and vehicle accidents Insurance is implemented through a legal contract, or policy. The insured is the person or business covered by the insurance policy. The insurer is the company that assumes the risk and agrees to pay losses cov ered by the policy. Insurance policies are written to cover losses that result from perils. A peril is the cause of a loss. Examples of perils that can be insured are fire, vandalism, vehicle accidents, and personal injury. The policyholder is the individual or organization to whom the policy is is- sued. The policyholder is often but not always the insured. In order to purchase insurance the policyholder must have an insurable interest in the covered loss. An insurable interest means that the insured will suffer a financial loss if the insured event occurs. The policyholder is charged a premium, which is the amount paid to the insurer to keep the insurance policy in force. WHAT CAN BE INSURED The availability of insurance is based on the proposition that the insurer can accurately predict the amount of losses that will be suffered by all of those who are insured for a particular type of loss in a given period of time It is impossible to predict whether any one business may have a fire that damages a building in a given year. But if thousands of businesses of a cer- tain type and in a particular geographic area are grouped together, accurate estimations can be made of the amount of fire damage that will be suffered during a year. The accuracy of predictions regarding the amount of losses that will occur among all of the businesses insured for a particular peril is very im- portant. Without the ability to estimate the amount of losses they will need to pay, insurance companies may not accumulate enough money from pre- miums to pay for all of the losses suffered and make a profit. Companies use principles of statistics to estimate losses. The companies employ actuaries, highly trained mathematicians who gather and analyze data and determine risk factors in order to establish premium rates. ness Insurance Actuaries apply the law of large numbers which means that when very large numbers of an event are considered, they will tend to form a normal distribution. You may be familiar with the view of a normal distribution hich is often referred to as a bell curve, as shown in Figure 10-1. Using statistics and data about the amount of losses that have occurred in prior vears, actuaries predict the total amount of losses that will result from a particular peril among all policyholders. For example, if an insurance com- pany issues 10,000 fire insurance policies to businesses, their calculations may estimate that 800 businesses will have losses from fires in the next year and the average loss will be valued at $6,800, FIGURE 10-1 A Bell Curve e s cov- esult be In order for a risk to be insurable, the following conditions need to exist. e s is- A large number of individuals or businesses must be facing the same tvpe of risk and be willing to purchase insurance. In order to be able to predict the amount of losses and spread the risk across a large number of individuals or groups, insurance companies have to sell a large num- ber of policies. The losses from the perils that are insured must be accidental and uncer- tain. People cannot take advantage of insurance companies by purchas- ing insurance and then causing a loss in order to collect money. Insurance fraud is a major problem for insurance companies. It is estimated that fraudulent claims add as much as 25 percent to insurance rates. in suffer ed a rance surer all of of time. The actual loss must be identifiable. In order to be paid for a loss by the insurance company, the insured must be able to document that the loss occurred as a result of the peril for which the insurance was pur- chased. The dollar value of the loss must also be identifiable. The probability of loss cannot be too high and the peril cannot be of a type that may affect a large percentage of insured at the same time. If most businesses suffer losses regularly or at the same time, too much money will be required to pay for the losses. For example, insurance companies become concerned if they sell a large number of the same type of insurance policies in an area that is subject to natural disasters uch as hurricanes, earthquakes, or floods. The result could be that al- ost all policyholders will have claims at the same time if a natural disaster hits that area. To protect themselves against those large losses, insurance companies use a process known as reinsurance. With reinsurance, an insurance company sells some of its risk to other that f a cer- accurate suffered will ry im- will need rom pre- anies actuaries etermine 10.2 Principles pause break C 1 prt sc sys rq scr lk F12

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Crisis Labour Markets And Institutions

Authors: Sebastiano Fadda

1st Edition

1138901822,1136268502