Answered step by step

Verified Expert Solution

Question

1 Approved Answer

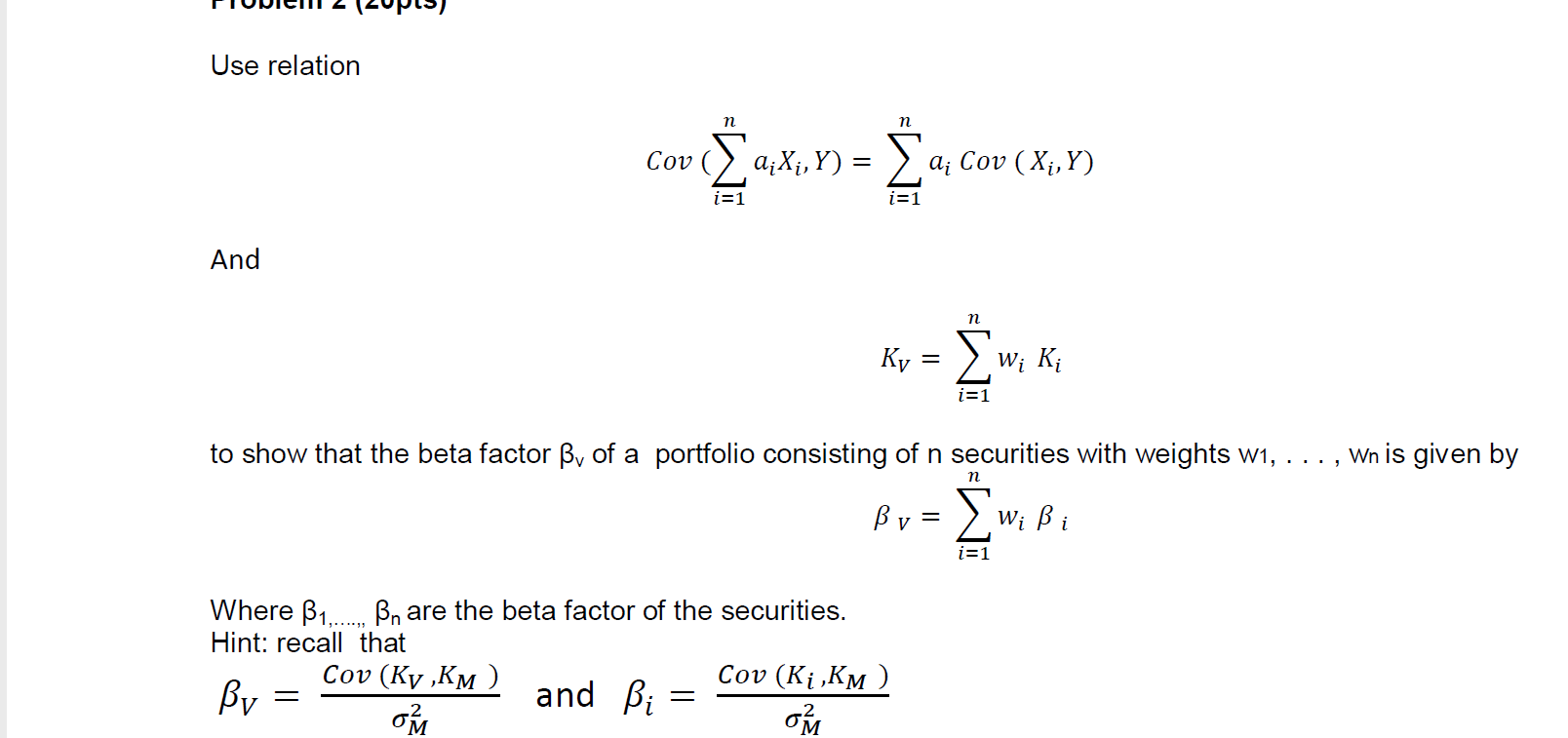

Use relation n n E Cov a;X,Y) = { = ai Cov (X,Y) i=1 And n K, = w, K, = i=1 to show that

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Technical Analysis For The Trading Professional Strategies And Techniques For Todays Turbulent Global Financial Markets

Authors: Constance M. Brown

2nd Edition

007175914X,0071759158