Answered step by step

Verified Expert Solution

Question

1 Approved Answer

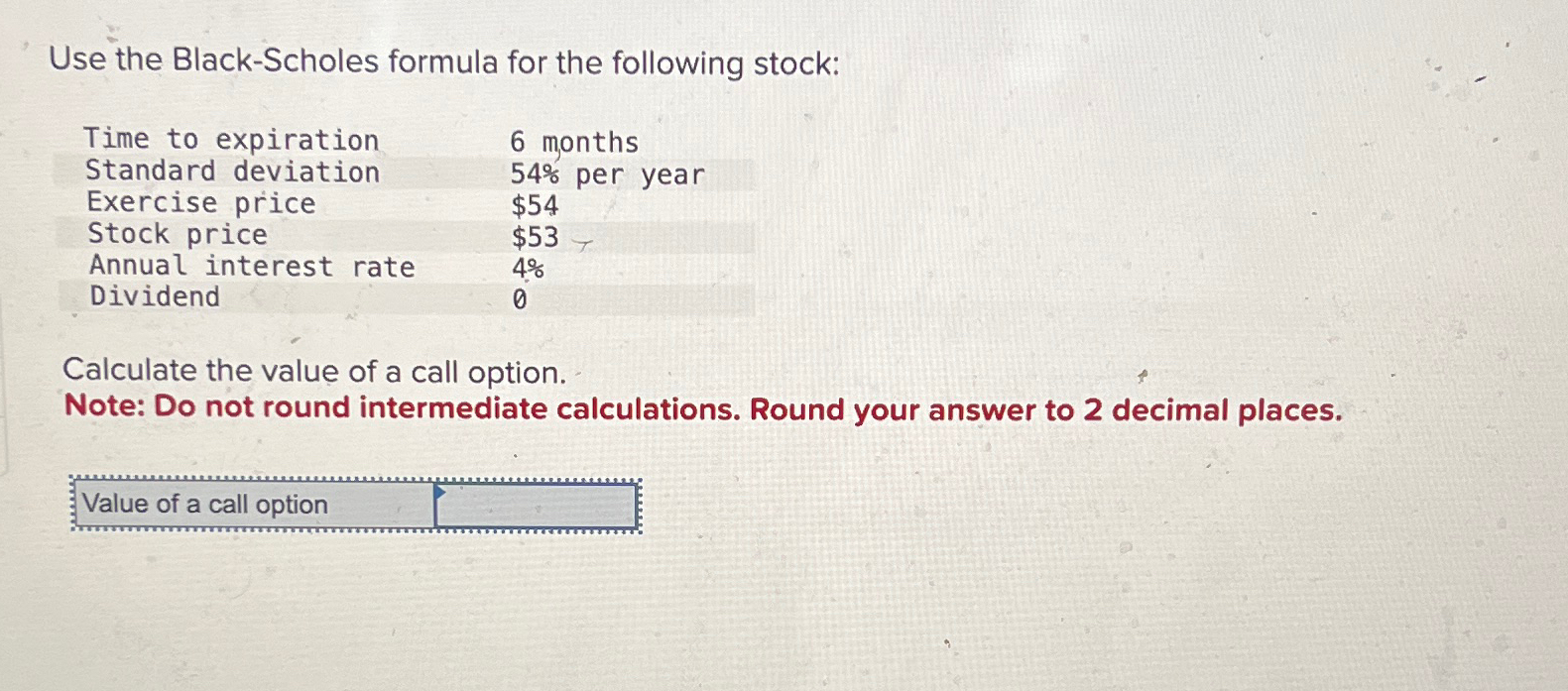

Use the Black-Scholes formula for the following stock: Time to expiration 6 months Standard deviation 54% per year Exercise price $54 Stock price $53

Use the Black-Scholes formula for the following stock: Time to expiration 6 months Standard deviation 54% per year Exercise price $54 Stock price $53 Annual interest rate 4% Dividend 0 Calculate the value of a call option. Note: Do not round intermediate calculations. Round your answer to 2 decimal places. Value of a call option

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Introduction to Investment Banks, Hedge Funds, and Private Equity

Authors: David P. Stowell

1st edition

978-0123745033, 0123745039, 978-9380931074