Question: Use the case study as shown in the photo and your own research on Peloton to answer the following questions. (500 words each question, total

Use the case study as shown in the photo and your own research on Peloton to answer the following questions. (500 words each question, total of 2000 words)

1) Using the Business Model Canvas to evaluate how Peloton brings together the nine components of the business model. Use each of the nine sections as sub-headings of your answer.

2) Using the Digital Maturity Levels of 0, 1, 2, 3, 4, determine which level Peloton is now. What technological advances and systems should Peloton implement to move up to higher levels of digital maturity? Provide a brief explanation of the various digital levels in your answer.

3) Peloton CEO John Foley used a range of motivations to develop and then launch his business. Applying the internal and external motivations outlined in the topics, how was Foley able to successfully launch and continue to grow Peloton? What role did Intrapreneurship play in this success?

4) Provide an update on Peloton since this case was written in 2020. How did COVID and post COVID impact Peloton. How might Peloton use core technologies and accelerator technologies in the future?

Use the material provided in the case study and references where appropriate, especially for question 4. Use in text referencing with a reference list at the end of the case study, using APA or Harvard style referencing.

![Erin Bass Introduction "Three [.. .] two [.. .] one [.. .]](https://s3.amazonaws.com/si.experts.images/answers/2024/07/668785bc74b19_628668785bc3aa8e.jpg)

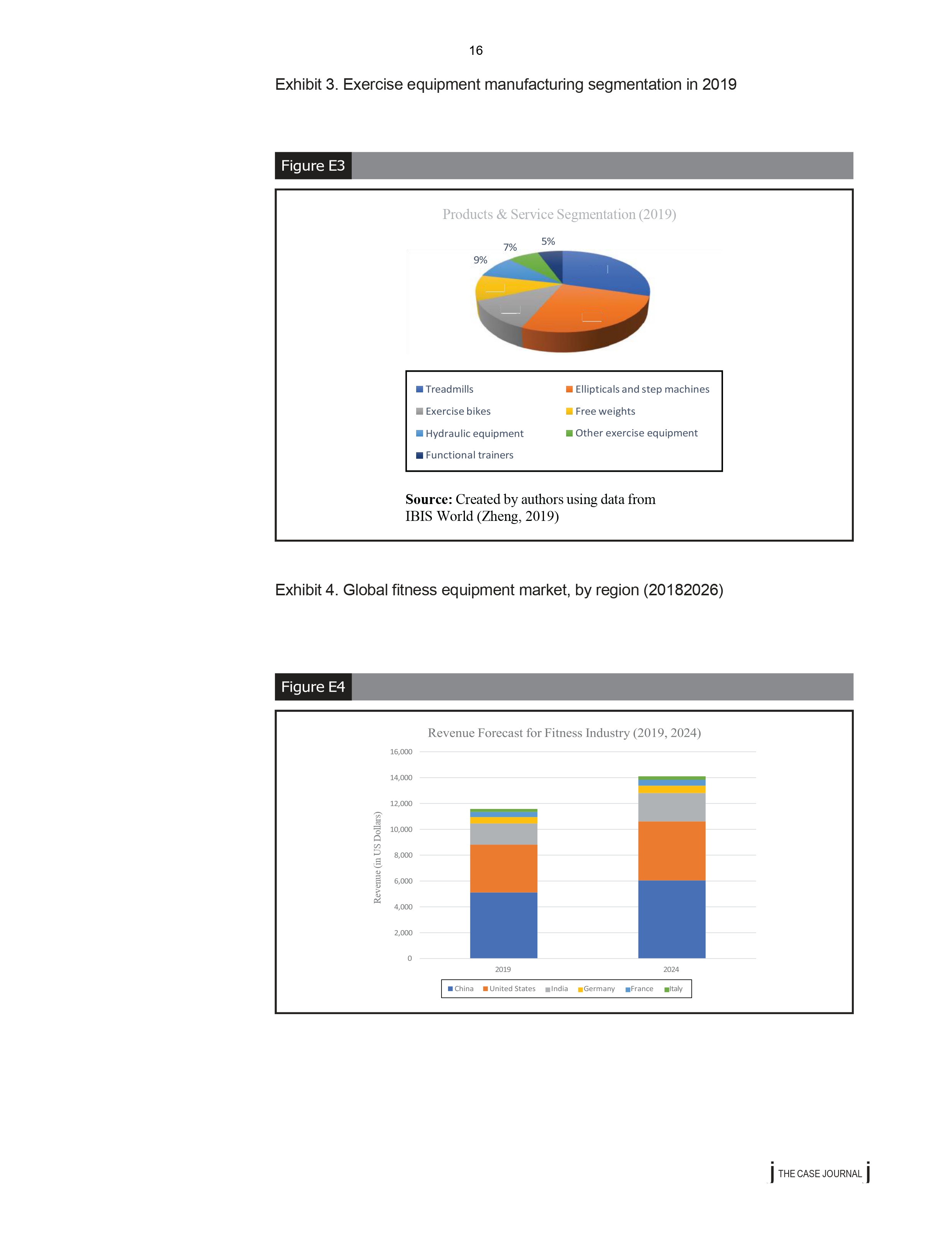

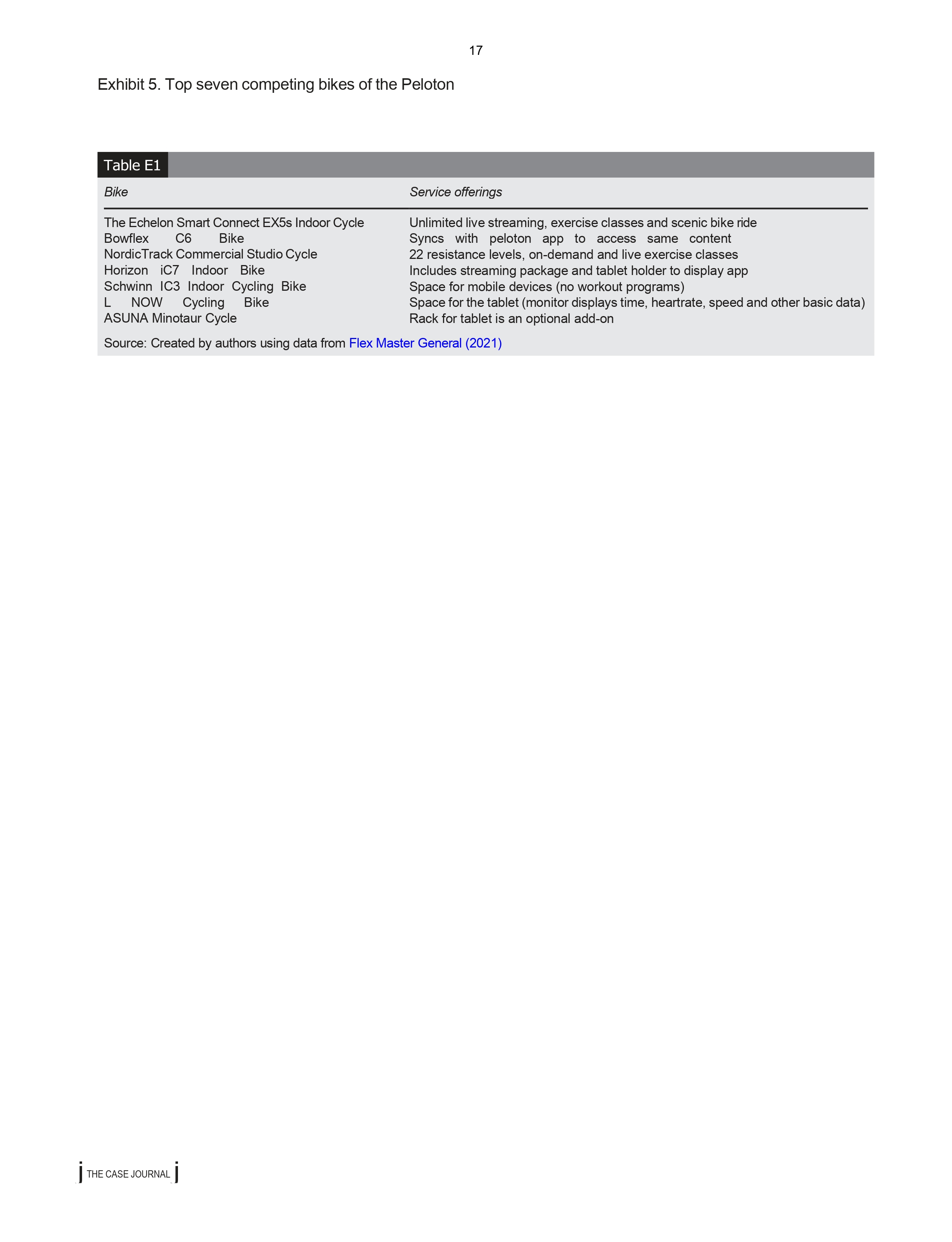

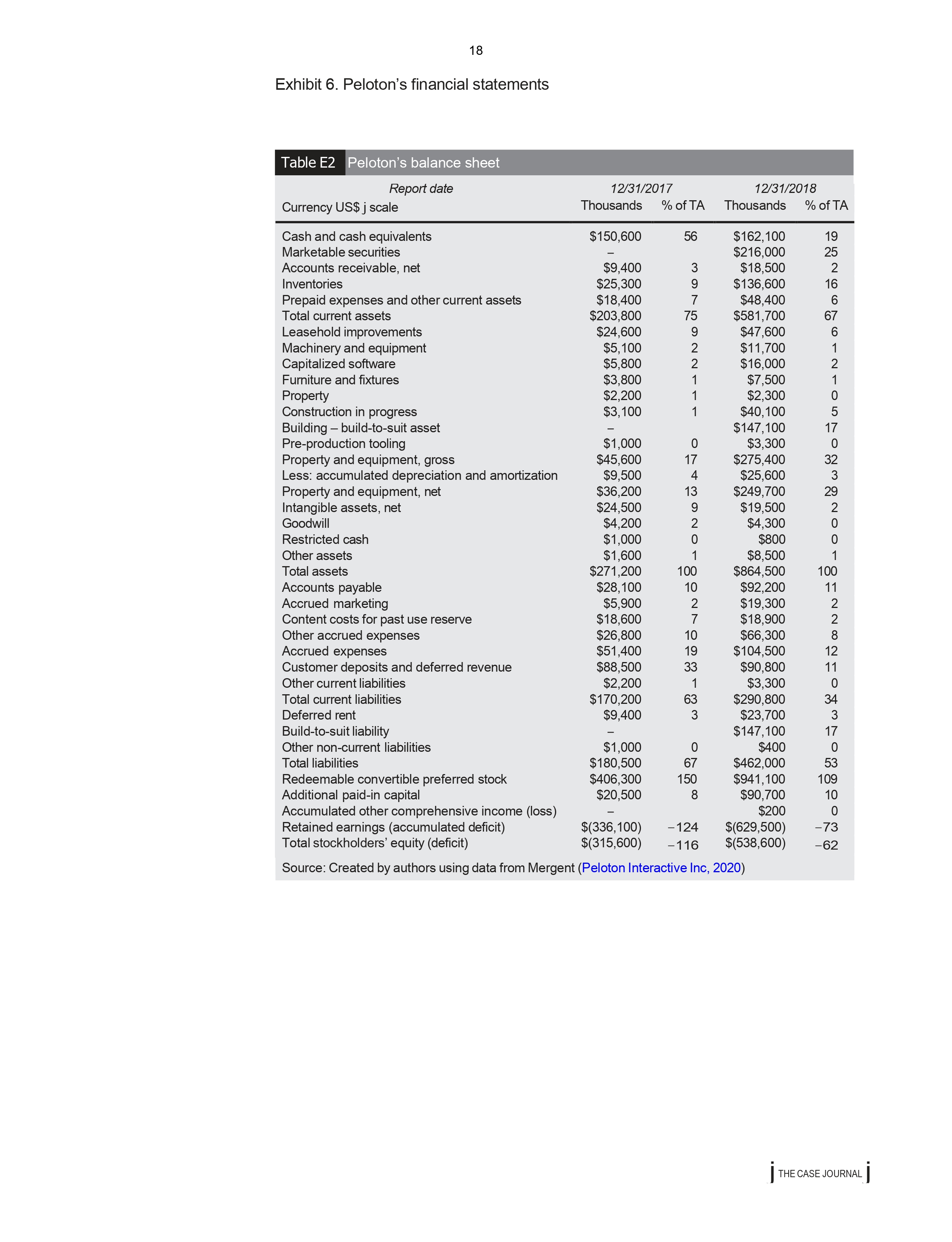

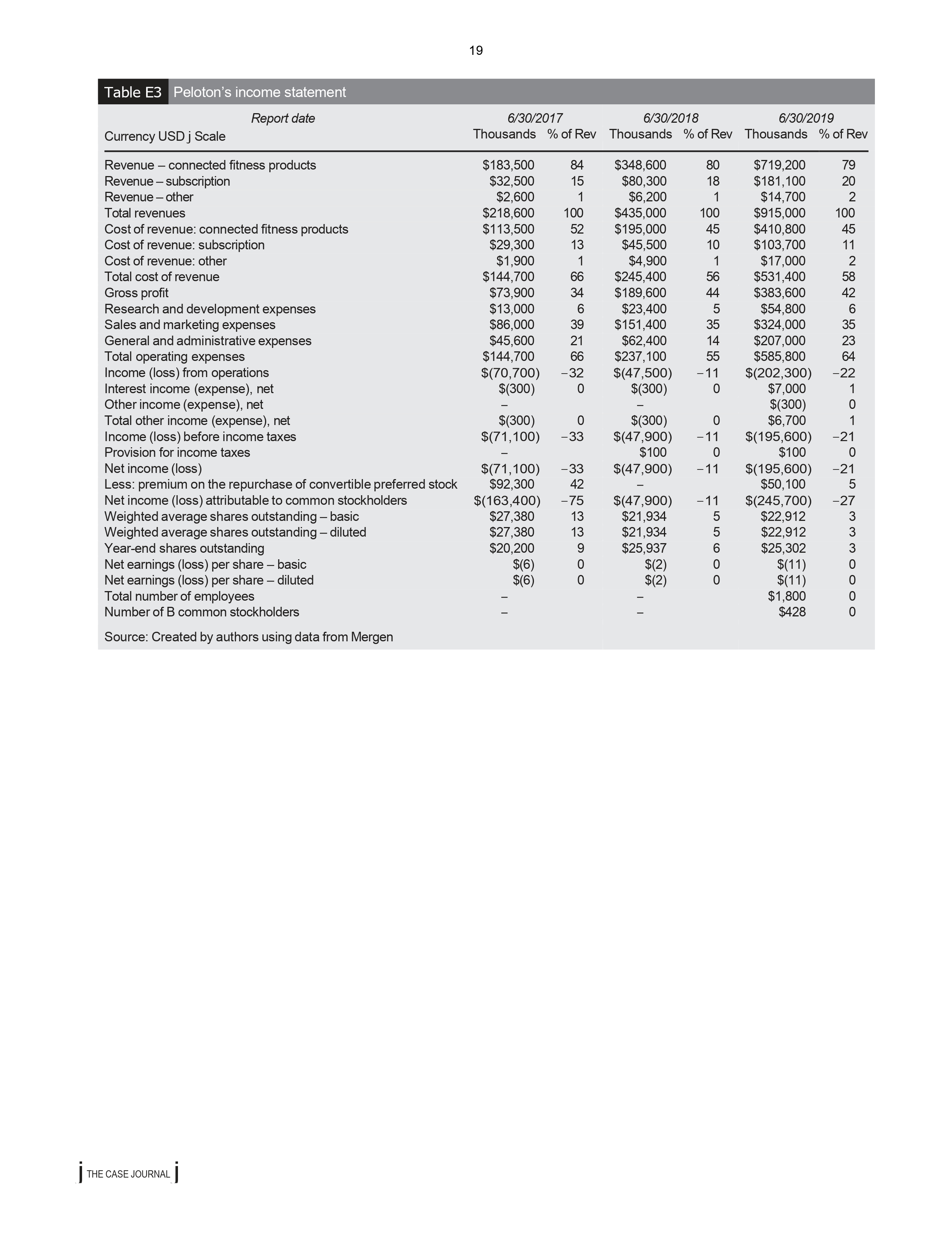

Peloton's ride to growth Christopher Curtis Winchester, Erin Pleggenkuhle-Miles and Andrea Erin Bass Introduction "Three [.. .] two [.. .] one [.. .] let's go!" The energy of Ally Love, a Peloton fitness instructor, was described as "incredibly authentic and motivating" (Dopson, 2020) by those who followed along with some of her classes when using a Peloton bike (Peloton, 2020a; Owusu, CASE 2019). In fall 2020, as consumers looked for the best fitness equipment available, there The CASE Association were many unique attributes about a Peloton bike that made it an enticing buy. However, as Disclaimer. This case is with any start-up that experienced fast growth, problems persisted that needed attention, intended to be used as the particularly as competition heated up. In December 2019, TheStreet's Tony Owusu wrote as basis for class discussion rather than to illustrate either follows: effective or ineffective handling of a management situation. The While Peloton has enjoyed a first-mover advantage, the lack of differentiation of its bike has case was compiled from finally caught up to it as the competition is not only making virtually identical exercise bikes but published sources. ones that are both more affordable and functional (Dopson, 2020). This problem, along with many others, troubled Peloton chief executive officer (CEO) John Foley as he navigated Peloton through an initial public offering (IPO), the COVID-19 pandemic and an uncertain future that had both strengths and weaknesses highlighted among the trends. As of fall 2020, Peloton was experiencing substantial growth due to the global pandemic pushing consumers to work out at home (Peloton's specialty); but as CEO John Foley looked to the future of Peloton, there were many unanswered questions. Describing the situation, thus far, CEO John Foley said as follows: It has been a rollercoaster. It's been emotional for me because we do think we're building something special. We do think we're making people's lives better. [However], we've had to scramble on a number of fronts [due to recent challenges] (Dopson, 2020). Peloton overview Foley described his company as "a media company akin to a Netflix." While this definition was fitting, Peloton Interactive Inc. described itself as follows: A technology company, media company, software company, a product-design company, a retail company, an apparel company, and a social connection company that enables our community to support one another (Owens, 2019) Foley envisioned providing customers with a unique fitness experience made possible through an integrative system of operations (Owens, 2019). Peloton used vertical integration to control the creation of its own software, bikes, exercise classes and even retail outlets. From production to delivery, Peloton took nearly full control of its production, sales and delivery cycles (Owens, 2019). With its integration of streaming workout classes and fitness equipment, Peloton was one of the fitness equipment industry leaders. Its product offerings focused largely on its bike, treadmill and mobile app. While the bike (starting at US$2,245) and treadmill (starting at US DOI 10.1108/TCJ-02-2021-0040 @Emerald Publishing Limited, ISSN 1544-9106 / THE CASE JOURNAL J2 $4,295) (Bary, 2019) had unique attributes such as the positioning of the handles and comparably smaller size (Peloton, 2020b), the app and its classes were what Emily Bary, a market analyst and reporter, believed gave Peloton a distinct advantage over many of its competitors (Bary, 2019). The app offered a US$39/month subscription that provided the consumer with unlimited live and on-demand content including more than 10,000 classes and 14 daily live classes ranging from cycling to yoga to strength (Pyros, 2019). The Peloton began by focusing on the creation of software and hardware for its bikes. However, through these innovations Peloton realized there was an opportunity to create its own electronic tablets and proprietary content. The Peloton continued its vertical integration by entering both the retail space and by integrating key upstream supply chain providers (Gross and Caisman, 2019). In doing so, Peloton was one of the rst companies in the industry to have near full control of the production process (Gross and Caisman, 2019). Its growth came from signicant rounds of funding (History of Peloton below), quickly making it one of the top brands in tness equipment (Turner, 2017). Nevertheless, Peloton's rapid expansion also resulted in a vast array of problems (Warren, 2017) such as legal ghts over music and patents, copycats, faddish decline and nancial losses (Grifth, 2019). In less than eight years from 2012 to early 2020 Peloton grew to more than 1,200 employees (Gross and Caisman, 2019) and 1.6 million subscribers (Peloton, 2020c). This growth created issues of maintaining its startup culture, adjusting its operations to become more decentralized and efciently managing its production process (Gross and Caisman, 2019). Peloton's high level of vertical integration coupled with rapid growth led to an increase of 147% in its operating expenses. Consequently, net income dropped from $47.9m to $195.6m from 2018 to 2019 (Peloton Interactive Inc, 2020) (Exhibit 1). At the beginning of 2020, Peloton's lackluster profitability combined with slowing growth had analysts concerned given the rise in competition. However, the COVID-19 pandemic shifted this perspective when consumers around the world were forced to stay home and consequentially sought out in-home exercise equipment. This presented Peloton with a major opportunity that saw record-breaking subscriptions, orders and stock prices (Smith, 2020). Speaking on the potential size of Peloton's market opportunity, Foley stated as follows: I see a couple hundred million people on the Peloton platform in 15 years [.. .] There's a lot of emails I've been getting about dots being connected on the potential size of our TAM (Total Addressable Market) and our SAM which is our Serviceable Addressable Market. We're selling a lot of bikes in the last 8 weeks [April May 2020] to people that hadn't been considering buying a Peloton product in the past (Shapiro, 2020). One of the key questions Peloton needed to address as it improved its strategy was how to capitalize on the growth experienced during the pandemic to ensure a long-term sustainable strategy. In exploring these future opportunities, there may have been pieces of Peloton's history that could have helped formulate Peloton's new growth strategy. History of peloton 400 no's and a yes (2012) Former Barnes and Noble ecommerce executive John Foley recognized the value of instructor-led workouts compared to self-led workouts (Inspirato, 2015). The problem, as Foley defined it, was to get that experience, you had to go into a gym, which took time. Specically, for cycle classes, you also had to reserve a bike which required advanced planning (Raz, 2019): The company and our concept are direct responses to the person who looks at his or her schedule and thinks, 'lt's going to be tough to squeeze in a really tough and fullling workout' i THE CASE JOURNAL I 3 [.. .] It's possible to get a drippingwet fitness class at any time, from any place. You just have to think about it a little di'erently (Inspirato, 2015). Foley founded Peloton in 2012 (Raz, 2019). Initially, it was going to be a software company providing fitness content; however, after searching for the right equipment, Foley and his partners realized they would need to build a bike. Peloton initially planned to use the iPad to deploy its content but realized that relying on outside hardware to deliver its content was risky. Thus, Peloton decided to design and engineer its own tablet (Raz, 2019). With the idea to design both the hardware and software to bring instructor-led workouts into people's homes, in 2012 Foley closed a $3.5m Series A round of funding and recruited a team of top- level co-founders (Warren, 2017) including Tom Cortese, Hisao Kushi, Yony Feng and Graham Stanton and (Peloton, 2020d) to help him realize the potential of his idea. However, raising initial funds was not easy as follows: I would bet I pitched three times a day for four years, \" Foley said, recalling Peloton's early days on an April 2019 episode of NPR's \"How I Built This with Guy Raz.\" Between thousands of angels, we had a hundred angels to get the rst 10 million. But in order to get a hundred angels at my success rate, I probably pitched 3, 000 people, and then the 400 institutions that all said no (Rogers, 2019). (Pedaling Forwards, 2013 2015) In the next two years, Peloton began its software and hardware development for the prototype of its innovative spinning bike and accompanying monitor. Foley traveled to Taiwan to scope out manufacturers and then went through several iterations of prototyping before the initial bike met the team's approval. Using the prototype bike, Peloton launched a Kickstarter campaign in November 2013 to not only raise money but also increase market awareness. Investors wanted proof of concept, but Foley was intent on creating a blue ocean within the fitness industry and did neither have the sales nor market statistics to showcase the potential of his idea. Forging ahead, Foley put out a call to hire top-of-the-Iine cycle instructors with the belief that people would follow a great instructor from the gym to the gym (Warren, 2017). Peloton's rst recorded content was lmed at the back of its ofce with four bikes, a black backdrop and secondhand equipment. Foley continued to pitch the concept. Though he believed that \"boutique fitness was a blind spot for Silicon Valley investors who did not see what was happening in New York," the prototype did lead to additional funding in 2014 in the form of a $10.5m Series B, which contributed to the rst consumer-ready model (Rogers, 2019). That same year, Peloton's first brickandmortar studio opened in Manhattan, which provided Peloton's newlyhired spin instructors a facility in which to film content for the bikes (Warren, 2017). In 2015, there was a push to improve the company's logistics. After a $30m Series C funding round, Peloton expanded its brick-and-mortar locations and accelerated the production of its bikes to keep up with the increasing demand. Relatedly, Peloton also started its own delivery service after many complaints and issues arose from third-party delivery companies. Peloton hired its own delivery personnel and purchased delivery vehicles to speed up the process and improve the satisfaction of customers (Warren, 2017). Vertical integration (20162018) Peloton's success with its bike continued to grow with the company citing a subscription growth rate of 128% from 2017 to 2018 (Johnston, 2019). Because of its success and increased brand popularity, in 2016 Peloton decided to provide unlimited live and on demand classes so customers could access Peloton classes through their phones and tablets without owning the bike. As Peloton grew, so did its funding. It received an additional $325m in funding in late 2016 (Warren, 2017). By 2016, Peloton had successfully vertically integrated into almost every facet of its production process. It created its own software, hardware, content, retail spaces, apparel, i THE CASE JOURNAL i instructor content and supply chain logistics (Warren, 2017). In June 2018, Peloton further added to its extensive product offerings with its first acquisition of Neurotic Media. This digital music aggregator added to Peloton's capabilities by allowing it to offer top-of-the-line music options for Peloton instructors and users during on-demand and live classes (Gross and Caisman, 2019). Peloton's IPO and holiday ad controversy (2019-early 2020) Throughout the next year, Peloton continued to grow its cult-like following (Siegel, 2019). Its fiscal year-end (June 2019) showed a strong $915m in revenues and a net income of -$195,600 (Peloton Interactive Inc, 2020). In 2019, Peloton received $550m in funding to fuel international expansion (Gross and Caisman, 2019) before its IPO on September 27th. Peloton's IPO offering was 40 million shares at $29 per share. However, its opening price was $27 and fell 11.2% below its initial offering by end of the day (Bary, 2019). After a steady increase in October 2019, partially due to the $47.4m acquisition of one of its bike manufacturing partners, Tonic Fitness Technology (Hanbury, 2019), a controversial "sexist and dystopian" Peloton commercial saw stock prices fall by more than $8 over the course of December 2019 (Ortiz, 2019). The holiday ad sparked a massive debate over social media and news outlets, with many citing that it portrayed negative body images and an unhealthy marriage (Cerullo, 2019) Perhaps, due to this massive backlash, within the one-month period in which the ad was released, Peloton saw its value drop by $1.5bn (Belam and Partridge, 2019). However, because the ad and tangential discussion were rampant within the zeitgeist, brand awareness for Peloton began to increase as people who had never heard of the company were suddenly made aware of Peloton (Riston, 2019). While the relatively short-lived backlash from the ad saw sharp declines in valuation, stock prices and sales, some analysts argue that it ultimately benefitted Peloton in the long run (The Canadian Press Staff, 2019). As shown in Exhibit 2, in January 2020, Peloton's stock hovered steadily between the upper $20s and lower $30s (Google Finance, 2020) with an $8bn valuation (Bary, 2019). Peloton reported more than 1.6 million subscribers who collectively participated in more than 55 million workouts and boasted a 94% 12-month retention rate (Peloton, 2020c). Riding through the COVID-19 pandemic As spring 2020 rolled around, the COVID-19 pandemic brought about unprecedented changes in the USA and across the world as people everywhere adapted to new social distancing norms. With significant economic and social changes, consumers turned to in- home exercise equipment and classes as gyms closed and people were encouraged or mandated to stay home. During that same time, Peloton experienced its largest streamed class in history, a noteworthy 23,000 people and its growth was reflected in its stock price, jumping 16% from January through April (Feuer, 2020). As the pandemic raged on, in April and May 2020, US unemployment rose to 14.7% (Long and Van Dam, 2020), 17.7% of workers were furloughed (Farren, 2020) and 31% of workers worked from home (U.S. Bureau of Labor Statistics, 2020). Collectively, this created an opportunity for Peloton. The following two initiatives were launched in the early spring of 2020 1. Peloton pledged $1m to its Global Bike and Tread Members; and 2. Peloton donated more than 100 bikes for frontline hospital and health-care workers to use (Peloton, 2020e Furthermore, Peloton pledged itself in the fight against racial injustice, pledging $100m promoting well-being and equity for all. This pledge also included expanding Peloton's diversity, equity, and inclusion team, launching new learning programs and incorporating | THE CASE JOURNAL j5 more diversity in its class offerings (Peloton, 2020f). Even as the pandemic persisted, through these diversity- and pandemic-related initiatives indicators of Peloton's growth continued. As of October 2020, Peloton's stock had climbed 459% compared to October 2019. Peloton's stock hit a record close of $130.97 on October 13th and Baird analyst Jonathan Komp indicated these pandemic gains would last (Smith, 2020). As Peloton looked to the future, it was seemingly in a great position, but the industry presented unique opportunities and threats that demanded attention. Ind ustry overview In 2018, the global tness industry including health clubs, studios, gyms, personal trainers and tness equipment was estimated at $94bn (Wellness Creative Co., 2019). The industry's revenue growth was estimated at 8.7%, with memberships and tness options expected to keep pace with growing disposable income trends. In each of the industry categories, several key trends lead to increased growth. For example, one of the biggest contributors to the increase in the tness industry was the sense of community for consumers (Kestenbaum, 2019). Forbes noted this as being the main reason consumers worked out with others (Kestenbaum, 2019). Consumers also drove the rapid uptick in technological developments, specically related to coaching and motivation (Kestenbaum, 2019). One example of this was articial intelligence (Al) being used to coach consumers. Al used sensors to monitor body movement and provide detailed instructions on how to move (Kestenbaum, 2019). Related to Peloton and its tness equipment intended for home use, there was a \"seasonal fad" of working out at home that was particularly attractive during the winter months (Kestenbaum, 2019). Digital trends overall took advantage of streaming capabilities and improved connectivity, a key trend that Foley spoke to (Wellness Creative Co., 2019) as follows: We're not a hardware company [...] Those [legacy exercise-equipment] companies are yesteryear\" within the tness industry (Hartmans, 2018). As noted above, Peloton operated in many different categories of the tness industry. One of these was the personal trainers and classes category that included one-on-one and group session fitness training (Fernandez, 2018). From 2018 to 2023, it was expected to see a 1% annual growth rate added to the $9.1bn annual earnings in the industry (Fernandez, 2018). A few key contributors to this expected growth were the anticipated rise in leisure time available to consumers, paired with the expected growth in disposable income (Fernandez, 2018). Additionally, as the motivation and community facets of classes and personal trainers gained momentum, the number of gyms and self-employed personal trainers offering these services was also expected to grow to meet the rising demand (Fernandez, 2018). Another category Peloton competed heavily in was exercise equipment. Overall, the $2bn exercise equipment manufacturing category had reached maturity and some argued it was in the decline stage. Annual growth from 2014 to 2019 was 0.6% and was expected to only increase to 0.9% from 2019 to 2024. However, the most prominent revenue drivers sports participation and consumer spending were expected (pre-pandemic) to increase in the coming years. A breakdown of the categories of the industry is depicted in Exhibit 3. The five major trends expected to impact the future of the industry were the COVlD-19 pandemic, health consciousness of consumers, offshoring of production, the globalization of the industry and the integration of the internet with tness equipment (Zheng, 2019). COVID-19 pandemic In spring 2020, the COVlD-19 pandemic caused behavioral and economic shifts globally as stay-athome orders were put in place (Reynolds, 2020). During this time, exercise was i THE CASE JOURNAL i 6 promoted as a great source of self-care while quarantined, collectively increasing the number of individuals working out at home (Goldfarb, 2020). As such, this was a positive source of revenue for inhome tness companies as a whole and particularly in the smart equipment segment of the global tness industry as it provided people a way to connect with others and get high-quality workouts from home (Feuer, 2020). As the industry looked beyond the pandemic, the major question became how companies in the industry could capitalize on the increase in users and people who exercised at home. According to Foley as follows: I don't think people are going to rush back to crowded gyms. / just don't see that happening. Especially people who experience Peloton, and why it's a better experience at a better location with a bigger community, with better instructors, for better value [.. .] The gym model was challenged yesterday. And I think it will be even more challenged tomorrow (Shapiro, 2020). Health consciousness The fitness industry as a whole saw a boost as an increasing number of people were concerned with their health and with tness club memberships increasing year after year worldwide (Gough, 2019). Boosting this trend, some employers and insurers began covering the costs of health club membership and classes, as healthy individuals tended to cost less to insure (Midgley, 2018). While the economy saw improved growth over the past ve years, the rise in disposable income did not translate into the sports equipment category. While there was a 37.1% increase in health club memberships between 2008 and 2018; exercise equipment decreased in overall sales volume. A potential opportunity equipment companies were hoping to exploit came in the form of the Personal Health Investment Today Act introduced to the House of Representatives in March 2019, which would give tax incentives to those who enrolled in exercise classes and/0r purchased exercise equipment (Zheng, 2019). Offshoring Because of the decline noted in the exercise equipment industry, many competitors had pursued efforts to cut costs. One of the most prominent avenues for this was Offshoring. Many companies eliminated or consolidated domestic production as they shifted production to China, Taiwan or elsewhere. This led to increased pricebased competition, which resulted in reduced prot margins across the board. As a result, many players in the industry were either acquired or went bankrupt (e.g. Scit, Cybex lntemational Inc., Indoor Cycling Group and Queenax). Additional globalization within the industry also took place due to the rise of Offshoring production (Zheng, 2019). Globalization The globalization of the exercise equipment manufacturing industry was on the rise in 2019 and was expected to continue through the coming five years. One of the biggest drivers was the rising international demand for tness equipment for homes, hotels and gyms. An additional catalyst to the growing lntemational demand was the decreasing value of the US dollar as this presented a growth opportunity for industry manufacturers. In fact, by 2024 exports were expected to account for more than 36% of industry revenue, an annualized increase of 1% (Exhibit 4) (Zheng, 2019). Integration of internet A more recent trend was the integration of the internet with traditional exercise equipment. Many companies noted that in this mature industry a major shift was needed. Therefore, online exercise classes and immersive exercise experiences were incorporated by top i THE CASE JOURNAL I 7 companies in the industry such as Echelon, Peloton and ICON tness through electronic panels on the exercise equipment. This made exercising more motivating for many users who could not nd time to go to the gym (Dopson, 2020). As seen in many of Peloton's competitors, this trend was increasingly incorporated into the equipment, lessening its incorporation as a true differentiator for any one rm (Zheng, 2019). Peloton's competitors Echelon One of Echelon's main advantages was its focused experiences that it provided to its consumers. As a prominent seller of bikes (each equipped with a display for the Echelon Fit App), Echelon (2020a) was also one of the first movers in app development and reects (connected tness mirrors). Coupled with the relative affordability of its bikes in the low $1 ,OOOs (Echelon, 2020b), Echelon had made a name for itself within the tness equipment industry. ICON tness ICON fitness was the umbrella company for a myriad of brands including NordicTrack, iFit and Pro-Form, etc. Collectively, ICON tness focused on innovation by integrating technology with tness equipment. This included on-demand classes that could be connected with its fitness equipment that helped to tailor each workout to the user (ICON Fitness, 2020). While ICON tness offered a wider range of products than Peloton, its average bike was similar to the price of Peloton at around $2,000 (NordicTrack, 2020). Sou/Cycle and equinox The focus of SoulecIe was on the experience of users. Soulecle's main differentiator was that it did not focus on selling bikes and equipment, but rather on providing classes in its studios using its equipment. Soulecle's traditional 45-min classes were in dim, candle-lit studios that were enhanced with the beat of the music. In addition to these classes, Soulecle also sold an extensive line of apparel that paired well with its workouts (Soulecle, 2020). To increase its competitiveness with Peloton, Soulecle's parent company, Equinox, unveiled a bike similar to the Peloton in 2019 that included a screen to bring the Soulecle classes into users' homes (Vennare, 2021 ). Flywheel Flywheel (2020), was a direct competitor for Peloton, offering both on-demand and in- person classes through the builtin tablets on its fitness equipment. Flywheel (2020) also offered in-person classes for the consumers who desired in-person tness experiences. Offering just one athome bike design, Flywheel sold its Flywheel Home Bike (with screen) for $1,999 (not including the $249 delivery and assembly fee) (Fit Rated, 2020). However, Peloton accused Flywheel of infringing on its patents in 2018 and in February 2020, the two companies settled (McGarry, 2020). In March 2020, Flywheel stopped offering its live- streamed and ondemand classes, leaving its studio classes as Flywheel's only product offering (McGarry, 2020). Precor Precor's mission centered on creating personalized health and tness experiences. Its state-ofthe-art equipment was integrated into multiple partnerships including eGym and Amer that helped it focus on its differentiation strategy (Precor, 2020a). Preoor (2020b) provided a wide array of options in exercise equipment, but the average cost of a bike was i THE CASE JOURNAL i 8 a few thousand dollars, making it one of the more premium options in the industry. One of Precor's most prominent advantages was its massive global reach, which included locations and sales all over North America, Europe and Asia. Its focus on both home and commercial tness allowed it to target a wide market all across the world, making it one of the most prominent names in the fitness equipment category (Precor, 2020a). Life tness As the market leader with around $1bn in sales, Life Fitness was the brand to beat. Previously owned by Brunswick Corporation, it was sold in 2019 to a private equity rm for $490m. Connected to its superior exercise equipment were its entertainment-rich consoles that included a wide variety of on-demand, immersive exercise experiences (Life Fitness, 2020a). As one of the leading names and innovators in the exercise equipment industry, Life Fitness (2020b) sold its equipment to many other industries ranging from gyms, to the military, to first responders for between $2,000 to $5,000. Other competition In addition to these primary competitors in the exercise equipment category, Peloton also competed heavily with its service offerings such as the on-demand and live classes it offered (Flex Master General, 2021). According to Flex Master General (2021 ), Peloton's top seven competing bikes when compared with services were the Echelon Smart Connect EX55 Indoor Cycle, Bowex CS Bike, NordicTrack Commercial Studio Cycle, Horizon iC7 Indoor Bike, Schwinn I03 Indoor Cycling Bike, L NOW Cycling Bike and ASUNA Minotaur Cycle (Exhibit 5). In a short time, Peloton's competitors had made strides in relation to one of its key differentiators its on-demand and live-streaming classes. Echelon, NordicTrack and Precor (2020a) each provided very similar offerings to Peloton in that they all used instructors and studios to provide on-demand and live-streaming classes (Flex Master General, 2021). Even technology giants were beginning to break into the industry to compete with Peloton. For example, Apple launched Fitnessb in the fall of 2020, which connected Apple users to trainers from the comfort of their homes. Foley addressed Apple's announcement stating as follows: We're just digesting the announcement like everybody. The biggest thing I will say is it's quite a legitimization of tness content, to the extent the biggest company in the word, a $2 trillion company, is coming in and saying tness content matters. It's meaningful enough for Apple (Thomas, 2020a). Collectively, this presented a serious challenge to Peloton; because as its rst-mover advantages dissipated, what remained was Peloton's legacy of high costs. As such, it wasn't clear whether Foley's strategy for Peloton would sustain long-term. Peloton's strategy In an interview with strategy In business, Foley was asked about Peloton's \"counterintuitive business model" as follows: People might think of us as a stationary bike company or a treadmill company, but we 're absolutely not. Peloton is an innovation company at the nexus of tness, technology, and media that owns the member experience from end to end which is why you could realistically call us hardware, software, content, logistics, and retail company, all at the same time. We believe that being vertically integrated is part of the secret to our success (Gross and Caisman, 2019). As a whole, Peloton strived to differentiate itself as a new concept in tness. Its mission stated that \"Peloton uses technology and design to connect the world through tness, i THE CASE JOURNAL I 9 empowering people to be the best version of themselves anywhere, anytime,\" which was emphasized by its four key values (Peloton, 20209) as follows: - Put members rst. - Operate with a bias for action. - Empower teams of smart creatives. - Together we go far. These values showcased Peloton's emphasis on immersing users during the exercise experience (Peloton, 20209). Its founding strategy was to differentiate within the fitness equipment industry by bringing fitness classes into users' homes and it continued to grow around this strategy. Peloton's positioning had been rmly rooted as a high-end, immersive fitness hardware and software provider. However, it used a unique approach compared to its rivals of being nearly completely vertically integrated. This meant it controlled almost every facet of its production, manufacturing and distribution in-house, which directly impacted its cost structure, as shown in Peloton's nancials (Gross and Caisman, 2019). Overall, Peloton's revenues largely came from its service subscriptions. It initially sold its equipment close to cost as it relied on subscriptions for its key revenue driver (Raz, 2019). However, it changed its pricing model after it learned that customers perceived the bike to be poorly built with a lower price point. Therefore, Peloton decided to raise its price to $2,245 from $1,200 (Mangalindan, 2019). This contributed to Peloton's increased revenues (Mangalindan, 2019). From 2018 to 2019, Peloton's revenues had more than doubled, going from $435m to $915m. In 2019, the vast majority (78.6%) of its revenues came from its connected tness products and 19.8% came from its subscription service (Peloton Interactive Inc, 2020). This exemplied the strong emphasis placed on its tness service offerings. While revenue appeared strong, Peloton's net income told a different story going from $47.9m in 2018 to $195.6m in 2019. To date, Peloton had not yet made a profit. However, Peloton's business model was not like a traditional equipment manufacturer. Peloton's primary sources of revenue are its user memberships, allowing customers access to streaming live and on-demand exercise classes and the premium exercise equipment itself. It has two types of memberships as follows: Peloton membership, for those who own the company's equipment and Digital membership, for those who want to only access the classes on an app (Reiff, 2019). Speaking on its membership increase due to the COVID-19 pandemic, Peloton addressed shareholders by stating: By the end of FY 2020, our Peloton membership base grew to approximately 3.1 million, compared to 1.4 million members in the prior year. Fueled in part by the challenges associated with COVID19, member engagement reached new highs with 164 million Connected Fitness Subscription workouts completed in FY 2020 (Owensc, 2020). Peloton's aggressive expansion strategy through aggressive market penetration in the USA, in combination with its steep operating expenses, made its nancial statements look more similar to a tech company than an equipment manufacturer (Exhibit 6) (Peloton Interactive Inc, 2020). In 2019, Peloton's return on assets (ROA), return on equity (ROE) and return on investment (ROI) were 34.45%, 79.32% and 82%, respectively (Peloton Interactive Inc, 2020). In its ling report, Peloton noted that its previous accounting and reporting structure before ling for an IPO was poorly done and could have been untrustworthy (Owens, 2019). Attention to the cost structure of its overall business model and future growth was a point of interest for analysts in early 2020 (Savitz, 2019), particularly as Peloton continued to place growth ahead of profitability (Thomas, 2019). According to one analyst, Peloton was undervalued given its capabilities, despite its profitability worsening (Fool, 2020). While Peloton's potential profitability was called into question, its Net Promoter Score (N PS), an indicator of the willingness of a customer to recommend its product, was one of the tops i THE CASE JOURNAL i 10 in the industry. It was consistently in the 805 and 905 for each product offering including its equipment, online class offerings and even its delivery, which was previously rated as very poor. Foley placed a heavy emphasis on improving Peloton's NPS to hit nearly 100 for every product, which was one of the key motivators behind his decision to bring its delivery in- house and pursue a vertical integration strategy (Gross and Caisman, 2019). Even as Peloton grew internationally, it remained focused on keeping its NPS scores high. While only 2% of Peloton's sales were intemational as of 2019, Foley expected sales in Canada and the UK to signicantly increase in the coming years (Gross and Caisman, 2019). Aside from these two regions, its global options appeared fairly restricted due to its limited language offerings and US-centric focus (Warner, 2019). If Peloton wanted international success, several operational challenges would need to be addressed. Operations As a relatively young company, Peloton had the advantage of being a start-up in a mature industry, meaning it could react faster than established companies to current and future trends (Gross and Caisman, 2019). However, as it quickly became one of the most prominent brand names, with more than 1.6 million members and nearly $1bn in sales (Peloton, 2020c), its start-up status quickly dissipated (Owens, 2019). As of January 2019, Peloton had more than 1,200 employees and two headquarters, resulting in a new challenge as follows: Peloton was becoming more decentralized as it grew (Gross and Caisman, 2019). While it focused sales primarily within the USA, Peloton also sold its equipment in Canada, the UK and Germany (Peloton, 2020c). This rapid growth resulted in operational challenges for Peloton as its operations shifted from being highly centralized to more decentralized (Gross and Caisman, 2019). This added challenge caused substantial workloads for many of Peloton's work teams and divisions, but Foley praised their work stating: It's hard to put a finger on what team at Peloton is working the hardest because it feels like every team I talk to is redlining [.. .] The supply chain, the manufacturing teams, the eld ops teams where they deliver the bikes and treads globally [are working] all out for sure (Thomas, 2020b). Additionally, Peloton's internal culture faced growing pains as follows: maintaining a start-up culture while rapidly expanding into a large, publiclytraded business was inherently difcult (Gross and Caisman, 2019). In fact, as of December 2020, there were more than 600 posted job openings (Peloton, 2020h). with growth and turnover likely contributing to the difculty of maintaining Peloton's existing culture. Reviews on indeed also suggested some internal turmoil, with many of the criticisms linked to the management and career development (Indeed, 2020). As part of Peloton's culture, the company focused heavily on diversity, another aspect that differentiated it from other tech companies. This included an African-American woman on its board of directors and a female chief nancial officer. While this representation was still disproportional in Foley's eyes, it demonstrated the emphasis and commitment to diversity Peloton had compared to its competition (Gross and Caisman, 2019). However, while these many factors, both positive and negative, continued to persist, the COVlD-19 pandemic created an added challenge for Peloton's operations: We've had to scramble on a number of fronts. It's incredible coordination that needs to take place. There's rocket fuel in your business, and your business has just been displaced and you're no longer together, you're trying to change the engines on the plane when you're in the air, or whatever the metaphor is. It's tricky operational stuff. (John Foley?) (Shapiro, 2020) As Foley indicated, the pandemic created multiple problems that challenged Peloton's persistence for success. Despite Peloton's strong nancials and market opportunity as it i THE CASE JOURNAL I 11 headed into the remainder of 2020, both enduring pre-pandemic and new issues contested Peloton's strategy moving forward. The future of peloton Peloton appeared to be in a great position to continue its rapid growth and beat out its competition. Revenues were climbing, its popularity was increasing and its stock prices had leveled out above its IPO. However, many questions remained as its first-mover advantage dissipated. When speaking of Peloton's future, Foley said as follows: Our team is pretty hungry. We've still got a lot to prove. We are in the first out of the first inning rom our perspective. We're just getting started [.. ] But we are very humble to understand that there's a lot we're learning and there's a long way to go with a lot more left to do (Shapiro, 2020). With all that was happening in the world, how should Peloton position itself for future growth given its vision of using "technology and design to connect the world through fitness, empowering people to be the best version of themselves anywhere, anytime"? This was a crucial point in Peloton's history and the decision made would forever alter the course of Peloton's trajectory. This was a time-sensitive decision, so just as Ally Love, one of Peloton's fitness instructors, said, "three [.. .] two [.. .] one [.. .] let's go!" References Bary, E. (2019), "Peloton stock spins in reverse during trading debut as IPO market cools down", 29 September, available at: www.marketwatch.com/story/peloton-stock-spins-in-reverse-during-trading- debut-as-ipo-market-cools-down-2019-09-26 Belam, M. and Partridge, J. (2019), "Peloton loses $1.5bn in value over 'dystopian, sexist' exercise bike ad", 4 December available at: www.theguardian.com/media/2019/dec/04/peloton-backlash-sexist- dystopian-exercise-bike-christmas-advert Blumtritt, C. (2020), "Revenue forecast for the segment fitness by country 2019", 6 January available at: www- statista-com.leo.lib.unomaha.edu/statistics/891065/eservices-revenue-for-selected-countries-by-segment/ Cerullo, M. (2019), "Peloton holiday ad sparks heated debate on social media over body imagery", 4 December available at: www.cbsnews.comews/peloton-bike-ad-internet-divided-over-peloton- holiday-ad-today-2019-12-03/ Dopson, E. (2020), "Ally love - Peloton [facebook reviews]", 19 January, available at: www.facebook. com/pg/allylovepeloton/reviews/?ref=page_internal Echelon (2020a), "Echelon", available at: https://echelonfit.com/?gclid=CjwkCAiAugvwBRAEEiwAzvjq 3_Fu-ueEdvChLkMWpc17ygGz7Hz5M7atxiqqi1jgbmeiAj9kf97NBoCjGEQAvD_BWE Echelon (2020b), "Compare our models", available at: https://echelonfit.com/pages/compare-bikes Farren, M.D. (2020), "What's the REAL unemployment rate? Introducing the 'pandemic furlough rate" Mercatus Center George Mason University, 8 May available at: www.mercatus.org/bridge/commentary/ what%E2%80%99s-real-unemployment-rate-introducing-pandemic-furlough-rate Fernandez, C. (2018), "Personal trainers. IBISWorld specialized industry report OD4189", IBISWorld database, December Feuer, W. (2020), "Peloton stock pops after reporting largest class ever as coronavirus restrictions keep gyms closed", 24 April, available at: www.cnbc.com/2020/04/24/coronavirus-peloton-stock-pops-after- reporting-largest-class-ever.html Fit Rated (2020), "Flywheel home bike review", available at: www.fitrated.com/exercise-bikes/flywheel- home-bike/ Flex Master General (2021), "The best peloton alternatives", available at: https://flexmastergeneral.com/ peloton-alternatives/ Fool, M. (2020), "Peloton interactive is unprofitable and undervalued", 8 January available at: https://old. nasdaq.com/article/peloton-interactive-is-unprofitable-and-undervalued-cm 1263016 THE CASE JOURNAL |12 Flywheel (2020). "Flywheel sports", available at: www.flywheelsports.com/home-bike Goldfarb, A. (2020), "You can take care of yourself in coronavirus quarantine or isolation, starting right now", 22 March available at: www.nytimes.com/2020/03/20/style/self-care/isolation-exercise-meditation-coronavirus.html Google Finance (2020), "nasdaq: pton", Google Finance, 8 January Gough, C. (2019), "Number of members in health and fitness clubs worldwide from 2009 to 2017 (in millions)", 3 July, available at: www-statista-com.leo.lib.unomaha.edu/statistics/275065/members-of- health-and-fitness-clubs-worldwide/ Griffith, E. (2019), "Peloton is a phenomenon. Can it last?", 28 August, available at: www.nytimes.com/ 2019/08/28/technology/peloton-ipo.html Gross, D. and Caisman, B. (2019), "Peloton's bikes may be stationary. But as CEO john foley tells us, the business is on the move", 9 January, available at: www.strategy-business.com/article/Business-Cycle?gko= c8808& Hanbury, M. (2019), "Peloton spent $47.4 million on a company that makes its bikes, tackling one of its biggest risks", 5 November, available at: www.businessinsider.com/peloton-acquires-bike- manufacturer-addresses-one-of-its-biggest-risks-2019-11 Hartmans, A. (2018), "I tried peloton's new $4,000 treadmill - and now I get why the company has such a cult Following", 10 January, available at: www.businessinsider.com/peloton-ceo-john-foley-on-peloton- tread-cult-following-fitness-domination-2018-1 ICON Fitness (2020). "Our brands", available at: www.iconfitness.com/ Indeed (2020), "Peloton culture reviews [indeed review board]", available at: www.wsj.com/articles/ peloton-interactive-loss-narrows-11572957031 Inspirato (2015), "Pedal pusher: john fuley", January, available at: www.inspirato.com/details/places/ pedal-pusher-john-foley/ Johnston, M. (2019), "Peloton's risky business model", 29 August, available at: www.investopedia.com/ peloton-s-risky-business-model-4768768 Kestenbaum, R. (2019), "The biggest trends in gyms and the fitness industry", 20 November, available at: www.forbes.com/sites/richardkestenbaum/2019/1 1/20/the-biggest-trends-in-gyms-and-the-fitness-industry/ #61 1668a87465 Life Fitness (2020a), "Life fitness", available at: https://lifefitness.com/?_gac=1.86606570.1578593036. CjwKCAiAu9vwBRAEEiwAzvjag172FJ-GeMdplJhtCTvmpWQhqjlWPfCpLhuNtlik11HZvpCjULRoCSE4 QAVD_BWE Life Fitness (2020b), "Lifecycle exercise bikes", available at: https://shop.lifefitness.com/cardio/lifecycle- exercise-bikes Long, H. and Van Dam, A. (2020), "U.S. Unemployment rate soars to 14.7 percent, the worst since the depression era", The Washington Post, 8 May, available at: www.washingtonpost.com/business/2020/ 05/08/april-2020-jobs-report/ McGarry, C. (2020), "Flywheel bikes no longer work, so you get a free peloton instead", 19 February, available at: https://gizmodo.com/flywheel-bikes-no-longer-work-so-you-get-a-free-peloto-1841798213 Mangalindan, J.P. (2019), "Peloton CEO: sales increased after we raised prices to $2,245 per bike", 5 June, available at: https://finance.yahoo.comews/peloton-ceo-says-sales-increased-raised-prices- 2245-exercise-bike-132256225.html. Midgley, B. (2018), "The six reasons the fitness industry is booming", 26 September, available at: www.forbes. com/sites/benmidgley/2018/09/26/the-six-reasons-the-fitness-industry-is-booming/#1f283bd3506d Nordic Track (2020), "Exercise bikes", available at: www.nordictrack.com/exercise-bikes?gclid= CjWKCAiAu9vwBRAEEiwAzvjqueryFCwLLOEilg_voHOXRGlwpsaQdHRoCyX WQAVD_BWE Ortiz, A. (2019), "Peloton ad is criticized as sexist and dystopian", 3 December, available at: www. nytimes.com/2019/12/03/business/peloton-bike-ad-stock.html Owens, J.C. (2019), "Peloton IPO: 5 things to know about the interactive exercise-machine company", 28 September, available at: www.marketwatch.com/story/peloton-ipo-five-things-to-know-about-the- interactive-exercise-machine-company-2019-08-28 | THE CASE JOURNAL ]13 Owensc, J.C. (2020), "Peloton produces profit for the first time amid pandemic-demand spike, stock pushes toward new record", 10 September, available at: www.marketwatch.com/story/peloton-produces-profit-for- the-first-time-amid-pandemic-demand-spike-stock-heads-toward-new-high-11599768987#: ~:text= In%20total%20for%20the%20fiscal,in%20the%20previous %20fiscal%20year Owusu, R. (2019), "Peloton price target cut to $5 at citron on competition concerns", 10 December available at: www.thestreet.com/technology/peloton-valuation-5-a-share-short-seller-left-says Peloton (2020a), "Ally love", available at: www.onepeloton.com/instructors/bike/AllyMissLove Peloton (2020b), "Bike", available at: https://www.onepeloton.com/bike Peloton (2020c), "Investor relations", available at: https://investor.onepeloton.com/ Peloton (2020d), "Meet our team", available at: www.onepeloton.com/company/team Peloton (2020e), "An update from out cofounder and CEO john foley", 6 April available at: https://blog. onepeloton.com/peloton-covid-19-initiatives/ (accessed 22 June 2020). Peloton (2020f), "An update on the peloton pledge", available at: https://blog.onepeloton.com/peloton- pledge-first-steps/ Peloton (2020g), "The peloton story", available at: www.onepeloton.com/company Peloton (2020h), "Work at peloton", available at: www.onepeloton.com/careers Peloton Interactive Inc (2020), "Peloton interactive inc (NMS: PTON)", Mergent Online Financial Report. Mergent Online database, January. Precor (2020a), "Precor", available at: www.precor.com/en-us Precor (2020b), "Stationary bikes", available at: precorathome.com/collections/stationary-bikes Pyros, A. (2019), "Considering investing in a peloton? Here's what owners have to say", 4 December, available at: www.retailmenot.com/blog/is-the-peloton-worth-it.html Raz, G. (2019), "How I built this with guy raz: Peloton: john foley [audio podcast]", 28 April available at: www.stitcher.com/podcastational-public-radio/how-i-built-this/e/60335673 Reiff, N. (2019), "How peloton makes money", 11 September, available at: www.investopedia.com/ insights/how-peloton-makes-money/ Reynolds, E. (2020), "Coronavirus pandemic: updates from around the world", 1 May, available at: www. cnn.com/world/live-news/coronavirus-pandemic-05-01-20-int//index.html Riston, M. (2019), "Peloton's ad is bad, but it will ultimately benefit the brand", 10 December, available at: www.marketingweek.com/ritson-peloton-ad-benefit-brand/ Rogers, T.N. (2019), "Peloton is valued at more than $4 billion, but CEO and cofounder john foley says investors turned his pitches down for 4 years. These are the reasons why he thinks they were rejected so many times", 29 August, available at: www.businessinsider.com/why-peloton-ceo-john-foley-thinks- investors-rejected-him-2019-8 Savitz, E.J. (2019), "Peloton stock skids as analyst questions the size of the market", 11 October, available at:www.barrons.com/articles/peloton-stock-ipo-falls-size-of-market-51570825145 Shapiro, E. (2020), "Peloton CEO john foley talks cheaper bikes and making the most of staying home", 26 May, available at: https://time.com/5839552/peloton-ceo-john-foley/ Siegel, R. (2019), "Peloton pegs IPO hopes on its multifaceted identity and cult-like following", 26 September, available at: www.washingtonpost.com/business/2019/09/26/peloton-pegs-ipo-hopes-its- multi-faceted-identity-cult-like-following/ Smith, C. (2020), "Peloton stock is soaring. Analyst says gains from pandemic will last", 13 October, available at: www.barrons.com/articles/pelotons-gains-from-pandemic-will-last-analyst-says-51602624941 SoulCycle (2020), "SOULCYCLE", available at: www.soul-cycle.com/ The Canadian Press Staff (2019), "Backlash to peloton ad could boost sales, experts say", 10 December, available www.ctvnews.ca/business/backlash-to-peloton-ad-could-boost-sales- experts-say-1.4722466 Thomas, P. (2019), "Peloton shares fall as company puts growth ahead of profit", 5 November, available at: www.wsj.com/articles/peloton-interactive-loss-narrows-11572957031 THE CASE JOURNAL |14 Thomas, L. (2020a), "Peloton CEO on apple launching a workout service: 'it's quite a legitimization of fitness content", 15 September, available at: www.cnbc.com/2020/09/15/peloton-ceo-on-apple- launching-workouts-a-legitimization-of-fitness-content.html Thomas, L. (2020b), "You might be able to rent a peloton bike one day, CEO John Foley says", 11 September, available at: www.cnbc.com/2020/09/11/you-might-be-able-to-rent-a-center-bike-one-day- ceo-john-foley-says.html Turner, M. (2017), "A bunch of cycling enthusiasts just helped peloton cycle raise $325 million - betting it could be the 'apple of fitness", 24 May, available at: www.businessinsider.com/peloton-raises-325- million-2017-5 U.S. Bureau of Labor Statistics (2020), "Ability to work from home: evidence from two surveys and implications for the labor market in the COVID-19 pandemic", US Bureau of Labor Statistics, June, available at: www.bls.gov/opub/mlr/2020/article/ability-to-work-from-home.htm Vennare, A. (2021), "Equinox announced its peloton competitor", available at: https://insider.fitt.co/ equinox-soulcycle-peloton-competitor/ Warner, J. (2019), "Peloton IPO", What you need to know, 18 June, available at: www.ig.com/enews- and-trade-ideas/shares-news/peloton-ipo-what-you-need-to-know-190617 Warren, L. (2017), "A brief history of peloton: a look at the cycling startup's explosive growth", 20 June, available at: www.builtinnyc.com/2017/06/16/history-peloton Wellness Creative Co. (2019), "Fitness industry statistics [growth, trends, and research stats 2019]", 2 September, available at: www.wellnesscreatives.com/fitness-industry-statistics-growth/ Yahoo Finance (2020), "nasdaq: pton", Yahoo Finance, 23 January. Zheng, G. (2019), "Gym & exercise equipment manufacturing in the US. IBISWorld industry report 33992b", IBISWorld database, July. Corresponding author Christopher Curtis Winchester can be contacted at: winch092@umn.edu | THE CASE JOURNAL ]15 Exhibit 1. Peloton's revenue vs net income (20172019) Figure E1 Revenue vs. Net Income (2017 - 2019) $8,00,000 $6,00,000 $4,00,000 Total (in Thousands $2,00,000 (2,00,000) $(4,00,000) 2017 2018 2019 Year Revenue Net Income Source: Created by authors using data from Mergent (Peloton Interactive Inc, 2020) Exhibit 2. Peloton's Stock (Launch to January 2020) Figure E2 Stock Price Launch - February 2020 40 Stock Price (in US Dollars) 15 10 5 0 9-26-19 10-26-19 11-26-19 12-26-19 1-26-20 Date Source: Created by authors using data from Yahoo Finance (2020) THE CASE JOURNAL |16 Exhibit 3. Exercise equipment manufacturing segmentation in 2019 Figure E3 Products & Service Segmentation (2019) 7% 5% 9% Treadmills Ellipticals and step machines Exercise bikes Free weights Hydraulic equipment Other exercise equipment Functional trainers Source: Created by authors using data from IBIS World (Zheng, 2019) Exhibit 4. Global fitness equipment market, by region (20182026) Figure E4 Revenue Forecast for Fitness Industry (2019, 2024) 16,000 14,000 12,000 10,000 8 000 Revenue (in US Dollars 6,000 4,000 2.000 2019 2024 China United States India Germany France Italy | THE CASE JOURNAL j17 Exhibit 5. Top seven competing bikes of the Peloton Table E1 Bike Service offerings The Echelon Smart Connect EX5s Indoor Cycle Unlimited live streaming, exercise classes and scenic bike ride Bowflex C6 Bike Syncs with peloton app to access same content NordicTrack Commercial Studio Cycle 22 resistance levels, on-demand and live exercise classes Horizon iC7 Indoor Bike Includes streaming package and tablet holder to display app Schwinn IC3 Indoor Cycling Bike Space for mobile devices (no workout programs) L NOW Cycling Bike Space for the tablet (monitor displays time, heartrate, speed and other basic data) ASUNA Minotaur Cycle Rack for tablet is an optional add-on Source: Created by authors using data from Flex Master General (2021) i THE CASE JOURNALj 18 Exhibit 6. Peloton's financial statements Table E2 Peloton's balance sheet Report date 12/31/201 7 12/31/2018 Currency US$J' scale Thousands % of TA Thousands % of TA Cash and cash equivalents $150,600 56 $162,100 19 Marketa ble securities $216,000 25 Accounts receivable, net $9,400 3 $18,500 2 Inventories $25,300 9 $136,600 16 Prepaid expenses and other current assets $18,400 7 $48,400 6 Total current assets $203,800 75 $581,700 67 Leasehold improvements $24,600 9 $47,600 6 Machinery and equipment $5,100 2 $11,700 1 Capitalized software $5,800 2 $16,000 2 Furniture and xtures $3,800 1 $7,500 1 Property $2,200 1 $2,300 0 Construction in progress $3,100 1 $40,100 5 Building build-to-suit asset $147,100 17 Pre-production tooling $1,000 0 $3,300 0 Property and equipment, gross $45,600 17 $275,400 32 Less: accumulated depreciation and amortization $9,500 4 $25,600 3 Property and equipment, net $36,200 13 $249,700 29 Intangible assets, net $24,500 9 $19,500 2 Goodwill $4,200 2 $4,300 0 Restricted cash $1,000 0 $800 0 Other assets $1 ,600 1 $8,500 1 Total assets $271 ,200 100 $864,500 100 Accounts payable $28,100 10 $92,200 '1 Accrued marketing $5,900 2 $19,300 2 Content costs for past use reserve $18,600 7 $18,900 2 Other accrued expenses $26,800 10 $66,300 8 Accrued expenses $51,400 19 $104,500 '2 Customer deposits and deferred revenue $88,500 33 $90,800 '1 Other current liabilities $2,200 1 $3,300 0 Total current liabilities $170,200 63 $290,800 34 Deferred rent $9,400 3 $23,700 3 Build-tosuit liability $147,100 '7 Other non-current liabilities $1,000 0 $400 0 Total liabilities $180,500 67 $462,000 53 Redeemable convertible preferred stock $406,300 150 $941,100 109 Additional paid-in capital $20,500 8 $90,700 '0 Accumulated other comprehensive income (loss) $200 0 Retained earnings (accumulated decit) $(336,100) 124 $(629,500) 73 Total stockholders' equity (decit) $(315,600) _1 1e $(538,600) 62 Source: Created by authors using data from Mergent (Peloton Interactive Inc, 2020) i THE CASE JOURNAL I 19 Table E3 Peloton's income statement Report date 6/30/201 7 6/30/2018 6/30/2019 Currency USD j Scale Thousands % of Rev Thousands \"/0 of Rev Thousands % of Rev Revenue connected tness products $183,500 84 $348,600 80 $719,200 79 Revenue subscription $32,500 15 $80,300 18 $181 ,100 20 Revenue other $2,600 1 $6,200 1 $14,700 2 Total revenues $218,600 100 $435,000 100 $915,000 100 Cost of revenue: connected tness products $113,500 52 $195,000 45 $410,800 45 Cost of revenue: subscription $29,300 13 $45,500 10 $103,700 11 Cost of revenue: other $1,900 1 $4,900 1 $17,000 2 Total cost of revenue $ 144,700 66 $245,400 56 $531 ,400 58 Gross prot $73,900 34 $189,600 44 $383,600 42 Research and development expenses $13,000 6 $23,400 5 $54,800 6 Sales and marketing expenses $86,000 39 $151,400 35 $324,000 35 General and administrative expenses $45,600 21 $62,400 14 $207,000 23 Total operating expenses $144,700 66 $237,100 55 $585,800 64 Income (loss) from operations $(70,700) ,32 $(47,500) ,1 1 $(202,300) 722 Interest income (expense), net $(300) 0 $(300) 0 $7,000 1 Other income (expense), net $(300) 0 Total other income (expense), net $(300) 0 $(300) 0 $6,700 1 Income (loss) before income taxes $(71,100) 33 $(47,900) 11 $(195,600) 21 Provision for income taxes $100 0 $100 0 Net income (loss) $(71,100) 733 $(47,900) ,11 $(195,600) 721 Less: premium on the repurchase of convertible preferred stock $92,300 42 $50,100 5 Net income (loss) attributable to common stockholders $(163,400) 75 $(47,900) 11 $(245,700) 27 Weighted average shares outstanding basic $27,380 13 $21,934 5 $22,912 3 Weighted average shares outstanding diluted $27,380 13 $21,934 5 $22,912 3 Yearend shares outstanding $20,200 9 $25,937 6 $25,302 3 Net earnings (loss) per share basic $(6) 0 $(2) 0 $(11) 0 Net earnings (loss) per share diluted $(6) 0 $(2) 0 $(11) 0 Total number of employees $1 ,800 0 Number of B common stockholders $428 0 Source: Created by authors using data from Mergen i THE CASE JOURNAL i 20 Exhibit 7. Technology-market evolution matrix for Global Fitness Industry Figure E5 Pace of Market Evolution Slow Fast The Market Leads The Technology Leads Pace of Technological Evolution Exhibit 8. Sample strategic group map for the fitness industry smart bike provider segment Figure E6 Cost of Bikes Level of Amenities in Bike) Source: Created by authors using Peloton, Echelon, ICON, Equinox, Flywheel, Precot and Life Fitness Sites i THE CASE JOURNAL] i THE CASE JOURNALj 21 Exhibit 9. Sample as-is strategy canvas Figure E7 Strategy Canvas For Fitness Industry -Smart Bike Provider Segment (As -Is) 0 Pelmon Echelon + ICON Flywheel + Precor l Life Fitness QUALITY OF DIVERSITY OF VARIETY OF QUALITY OF LEVEL OF HOME USE CLASSES EQUIPMENT WORKOUTS APP BIKE AMENITIES Source: Created by authors using Peloton, Echelon, ICON, Flywheel, Precor and Life Fitness Sites Exhibit 10. Sample to-be strategy canvas Figure E8 Strategy Canvas For Fitness Industry -Smart Bike Provider Segment (To - Be) 0 Peloton Echelon + ICON Flywheel Precm' i Life Fitness QUALITY OF DIVERSITY VARIETY OF QUALITY OF LEVEL OF HOME USE ADDITIONAL CLASSES OF WORKOUTS APP BIKE HEALTH EQUIPMENT AMENITIES OFFERINGS Source: Created by authors using Peloton, Echelon, ICON, Flywheel, Precor and Life Fitness Sites 22 References Chen, M. J., & Miller, D. (2015). "Reconceptualizing competitive dynamics: A multidimensional framework". Strategic Management Journal, 36(5), 758-775. MacMillan, I., Mccaffrey, M. L., & Van Wijk, G. (1985). "Competitors' responses to easily mitated new products - exploring commercial banking product introductions", Strategic Management Journal, 6, 75-86. Mauborgne, R., & Kim, W. C. (2007). Blue ocean strategy. Gildan Media. Suarez, F. & Lanzolla, G. (2005). "The half-truth of first-mover advantage", Available at: https://hbr.org/2005/04/the-half-truth-of-first-mover-advantage Williamson, O. E. (1979). "Transaction-cost economics: the governance of contractual relations", The Journal of Law and Economics, 22, 233-261. Case Study Questions Use the case study and your own research on Peloton to answer the following questions. 1) Using the Business Model Canvas to evaluate how Peloton brings together the nine components of the business model. Use each of the nine sections as sub-headings of your answer. 2) Using the Digital Maturity Levels of 0, 1, 2, 3, 4, determine which level Peloton is now. What technological advances and systems should Peloton implement to move up to higher levels of digital maturity? Provide a brief explanation of the various digital levels in your answer. 3) Peloton CEO John Foley used a range of motivations to develop and then launch his business. Applying the internal and external motivations outlined in the topics, how was Foley able to successfully launch and continue to grow Peloton? What role did Intrapreneurship play in this success? 4) Provide an update on Peloton since this case was written in 2020. How did COVID and post COVID impact Peloton. How might Peloton use core technologies and accelerator technologies in the future? | THE CASE JOURNAL ]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts