Answered step by step

Verified Expert Solution

Question

1 Approved Answer

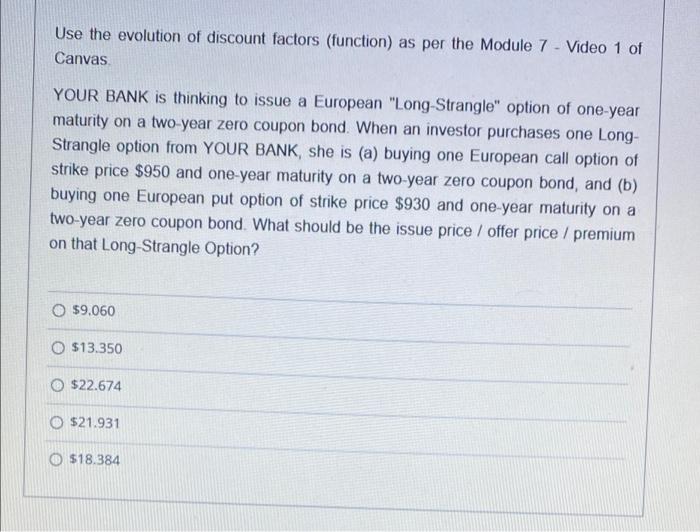

Use the evolution of discount factors (function) as per the Module 7 - Video 1 of Canvas YOUR BANK is thinking to issue a European

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Interpreting Company Reports And Accounts

Authors: Geoffrey Holmes, Alan Sugden, Paul Gee

10th Edition

0273711415, 9780273711414