Answered step by step

Verified Expert Solution

Question

1 Approved Answer

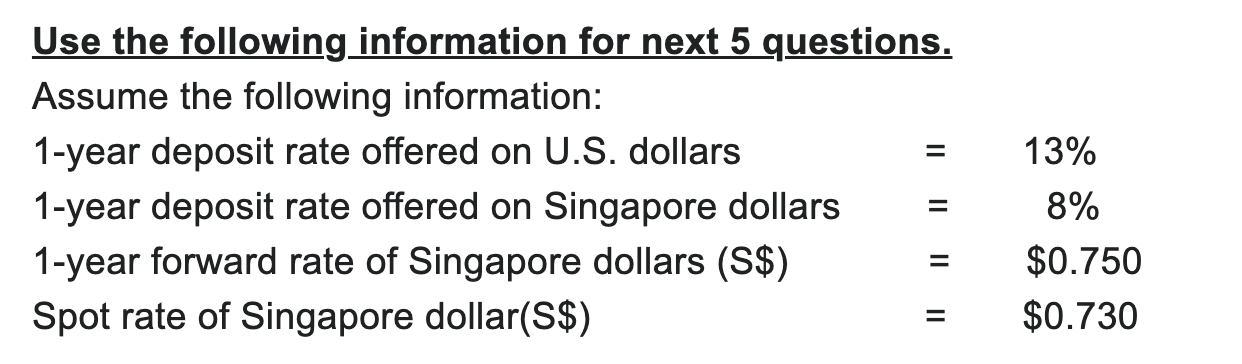

Use the following information for next 5 questions. Assume the following information: 1-yeardepositrateofferedonU.S.dollars1-yeardepositrateofferedonSingaporedollars1-yearforwardrateofSingaporedollars(S$)SpotrateofSingaporedollar(S$)====13%8%$0.750$0.730 Based on the calculation and the conclusion you obtained for the previous

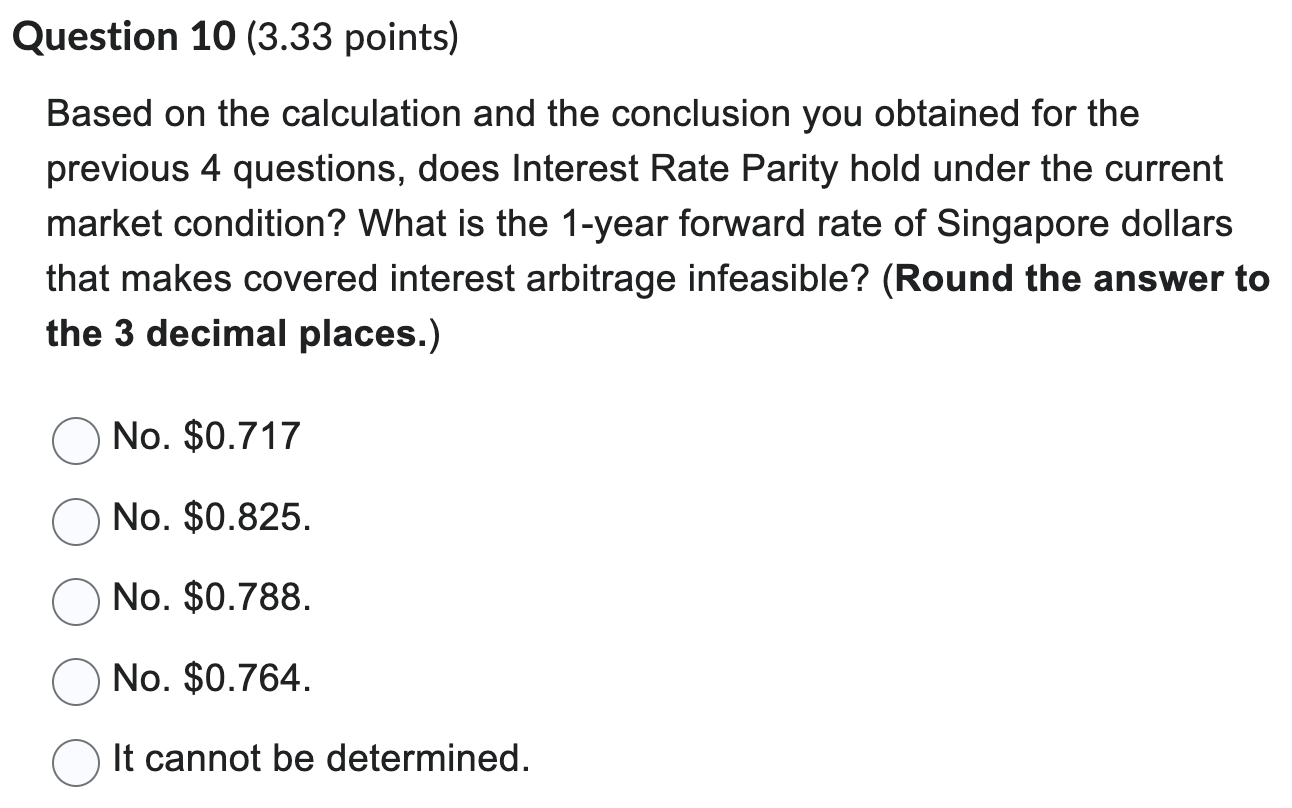

Use the following information for next 5 questions. Assume the following information: 1-yeardepositrateofferedonU.S.dollars1-yeardepositrateofferedonSingaporedollars1-yearforwardrateofSingaporedollars(S$)SpotrateofSingaporedollar(S$)====13%8%$0.750$0.730 Based on the calculation and the conclusion you obtained for the previous 4 questions, does Interest Rate Parity hold under the current market condition? What is the 1-year forward rate of Singapore dollars that makes covered interest arbitrage infeasible? (Round the answer to the 3 decimal places.) No. $0.717 No. $0.825. No. $0.788. No. $0.764. It cannot be determined

Use the following information for next 5 questions. Assume the following information: 1-yeardepositrateofferedonU.S.dollars1-yeardepositrateofferedonSingaporedollars1-yearforwardrateofSingaporedollars(S$)SpotrateofSingaporedollar(S$)====13%8%$0.750$0.730 Based on the calculation and the conclusion you obtained for the previous 4 questions, does Interest Rate Parity hold under the current market condition? What is the 1-year forward rate of Singapore dollars that makes covered interest arbitrage infeasible? (Round the answer to the 3 decimal places.) No. $0.717 No. $0.825. No. $0.788. No. $0.764. It cannot be determined Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Catechism Of Money

Authors: Joseph P. Root

1st Edition

1377114929, 978-1377114927