Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Use the following spot and forward bid-ask rates for the U.S. dollar/euro (USS/) exchange rate from December 10, 2010, to answer the following questions:

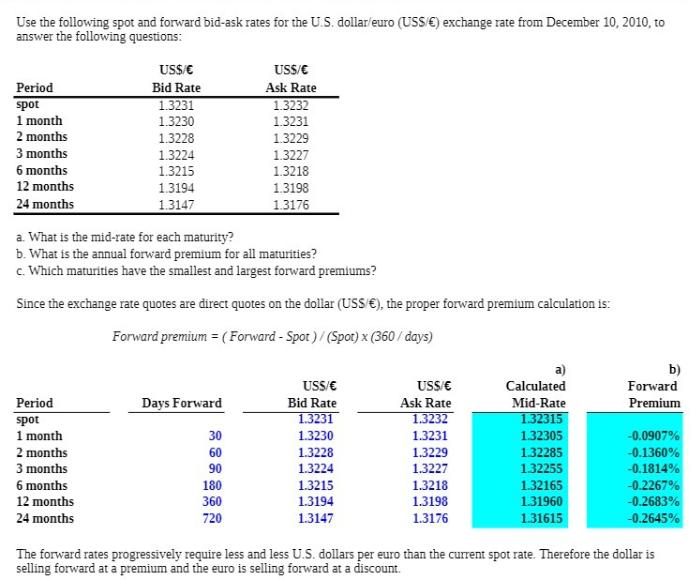

Use the following spot and forward bid-ask rates for the U.S. dollar/euro (USS/) exchange rate from December 10, 2010, to answer the following questions: US$/ US$/ Period spot Bid Rate Ask Rate 1.3231 1.3232 1 month 1.3230 1.3231 2 months 1.3228 1.3229 3 months 1.3224 1.3227 6 months 1.3215 1.3218 12 months 1.3194 1.3198 24 months 1.3147 1.3176 a. What is the mid-rate for each maturity? b. What is the annual forward premium for all maturities? c. Which maturities have the smallest and largest forward premiums? Since the exchange rate quotes are direct quotes on the dollar (USS ), the proper forward premium calculation is: Forward premium = (Forward - Spot) / (Spot) x (360/days) USS/ Period spot Days Forward Bid Rate USS/ Ask Rate a) Calculated b) Forward Mid-Rate Premium 1.3231 1.3232 1.32315 1 month 2 months 3 months 6 months 30 1.3230 1.3231 1.32305 -0.0907% 60 1.3228 1.3229 1.32285 -0.1360% 90 1.3224 1.3227 1.32255 -0.1814% 180 1.3215 1.3218 1.32165 -0.2267% 12 months 24 months 360 1.3194 1.3198 1.31960 -0.2683% 720 1.3147 1.3176 1.31615 -0.2645% The forward rates progressively require less and less U.S. dollars per euro than the current spot rate. Therefore the dollar is selling forward at a premium and the euro is selling forward at a discount.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Here are the calculations with deep workings a Midrate for each maturity Spot Bid 13231 Ask 13232 Mi...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Multinational Business Finance

Authors: David K. Eiteman, Arthur I. Stonehill, Michael H. Moffett

13th edition

132743469, 978-0132743464