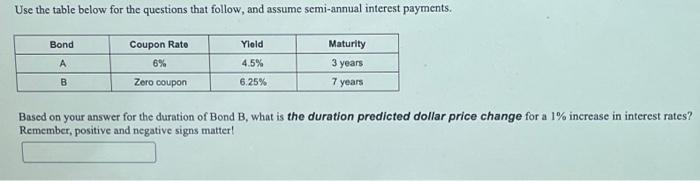

Question: Use the table below for the questions that follow, and assume semi-annual interest payments. Bond A B Coupon Rate 6% Zero coupon Yield 4.5% 6.25%

Use the table below for the questions that follow, and assume semi-annual interest payments. Bond A B Coupon Rate 6% Zero coupon Yield 4.5% 6.25% Maturity 3 years 7 years Based on your answer for the duration of Bond B, what is the duration predicted dollar price change for a 1% increase in interest rates? Remember, positive and negative signs matter!

Use the table below for the questions that follow, and assume semi-annual interest payments. Based on your answer for the duration of Bond B, what is the duration predicted dollar price change for a 1% increase in interest rates? Remember, positive and negative signs matter

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock