Answered step by step

Verified Expert Solution

Question

1 Approved Answer

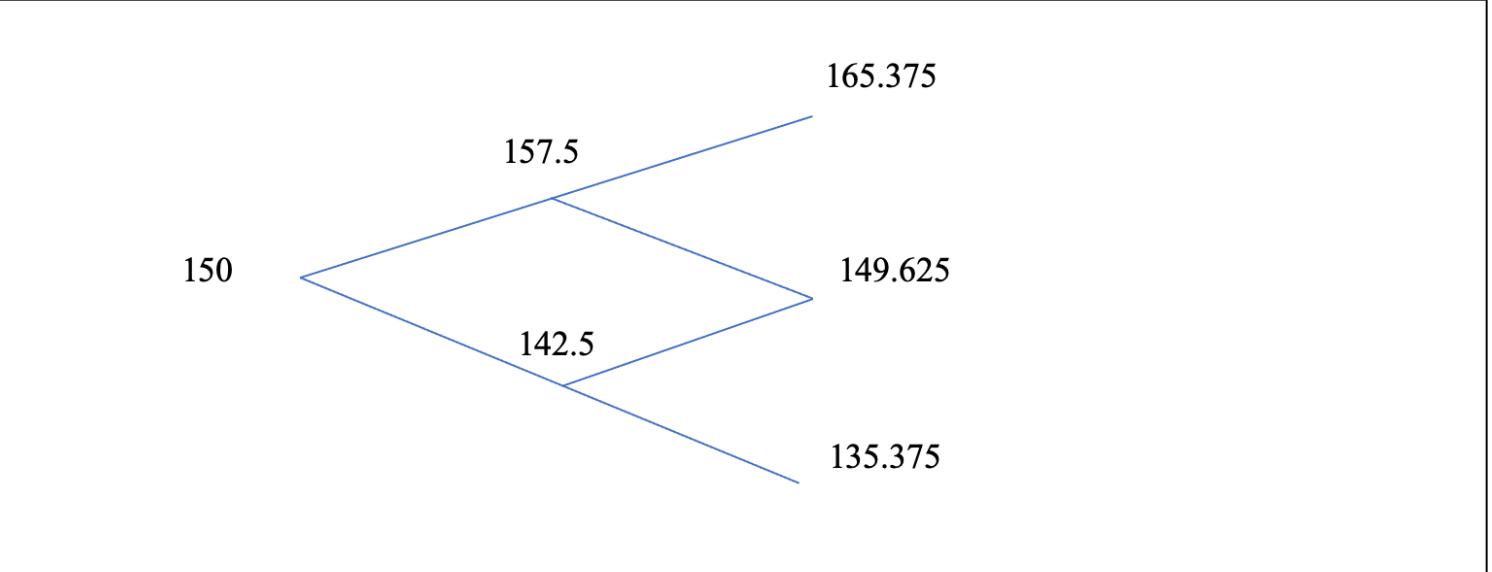

Use the two-step binomial tree from the image to calculate the value of a six-month European call option using the no-arbitrage approach. 150 157.5 142.5

Use the two-step binomial tree from the image to calculate the value of a six-month European call option using the no-arbitrage approach.

150 157.5 142.5 165.375 149.625 135.375

Step by Step Solution

★★★★★

3.35 Rating (164 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the value of a sixmonth European call option using the noarbitrage approach and the giv...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduces Quantitative Finance

Authors: Paul Wilmott

2nd edition

470319585, 470319581, 978-0470319581