Answered step by step

Verified Expert Solution

Question

1 Approved Answer

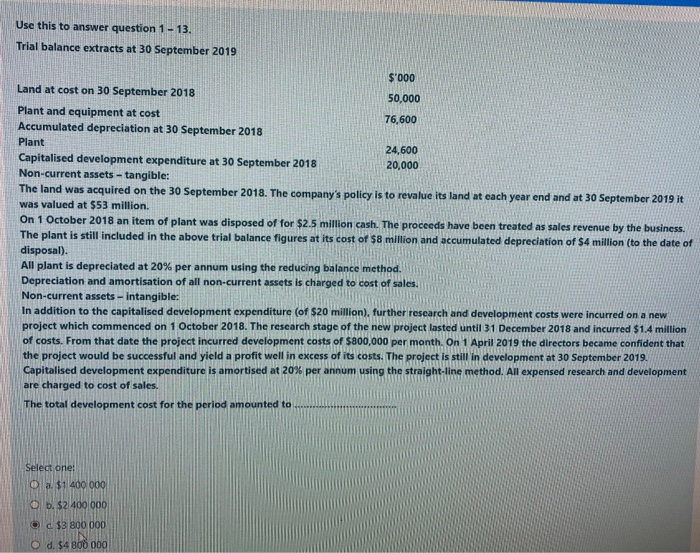

Use this to answer question 1 - 13. Trial balance extracts at 30 September 2019 $'000 Land at cost on 30 September 2018 50,000 Plant

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Practical Guide To UK Accounting And Auditing Standards

Authors: Steve Collings

1st Edition

152650331X, 9781526503312