Answered step by step

Verified Expert Solution

Question

1 Approved Answer

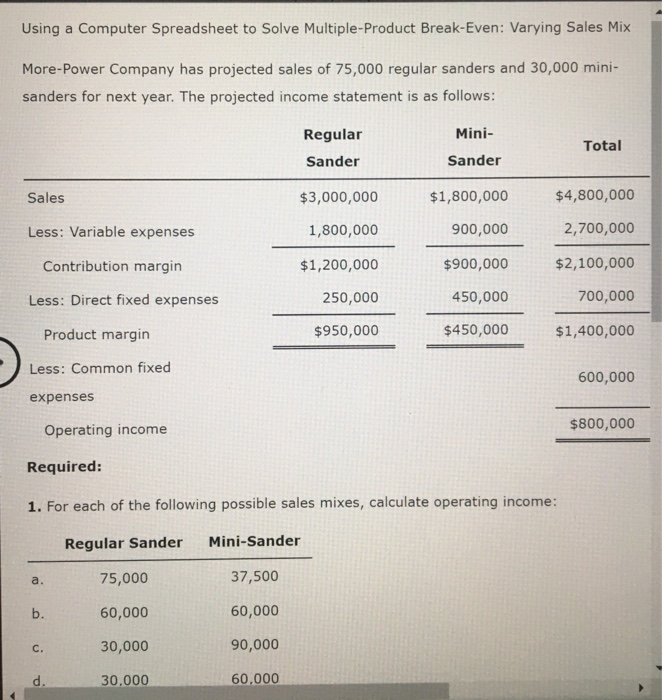

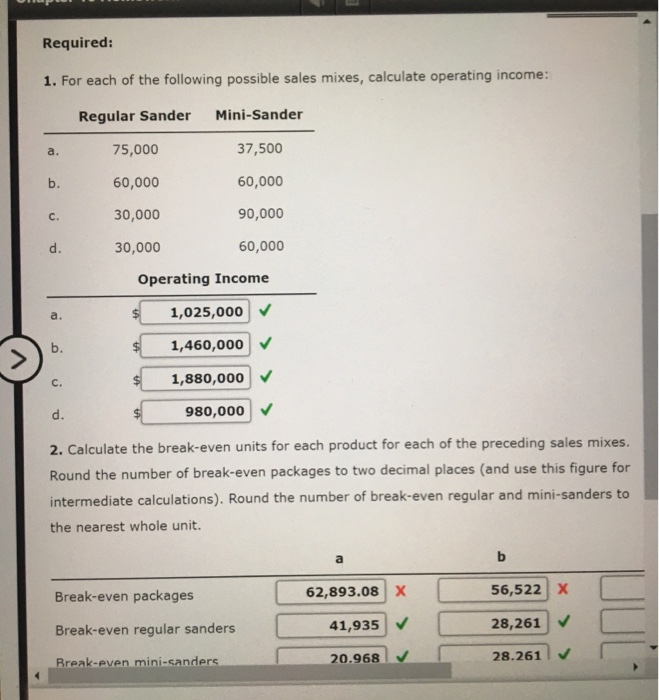

Using a Computer Spreadsheet to Solve Multiple-Product Break-Even: Varying Sales Mix More-Power Company has projected sales of 75,000 regular sanders and 30,000 mini- sanders for

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Cost Accounting

Authors: Edward J. Vanderbeck

16th edition

9781133712701, 1133187862, 1133712703, 978-1133187868