Question

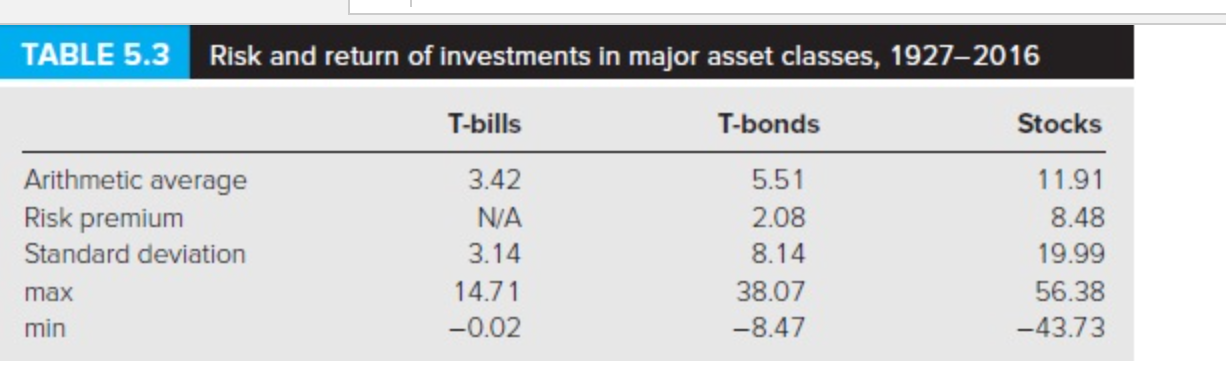

Using Table 5.3 as your guide. (All returns in this problem are in annual term.) Estimate the Sharpe Ratio of the stock market portfolio and

Using Table 5.3 as your guide. (All returns in this problem are in annual term.) Estimate the Sharpe Ratio of the stock market portfolio and the Sharpe Ratio of the T-Bonds. Hints: Assume that market risk premium and market volatility are constant over time. The same for T-Bonds.

Market Sharpe Ratio =

T-Bond Sharpe Ratio =

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of Alternative Assets

Authors: Peter Temple

1st Edition

161477076X, 978-1906659219