using the common sizing method

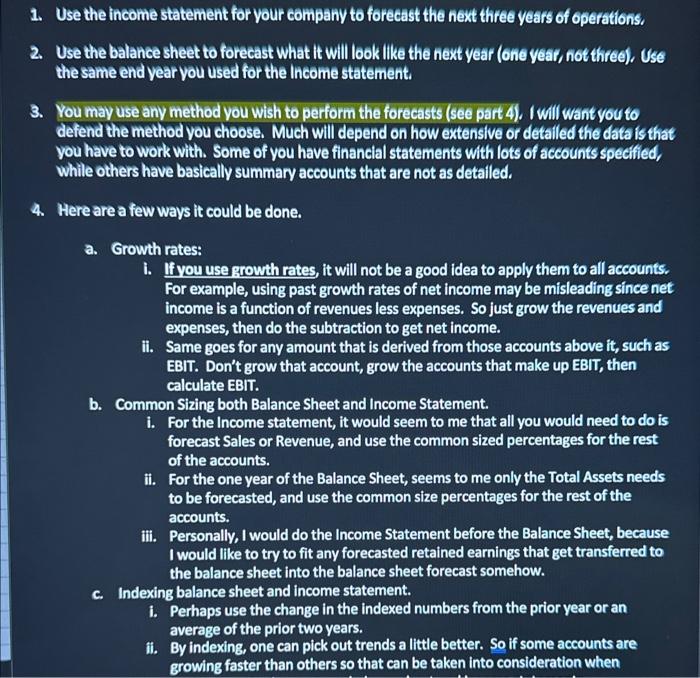

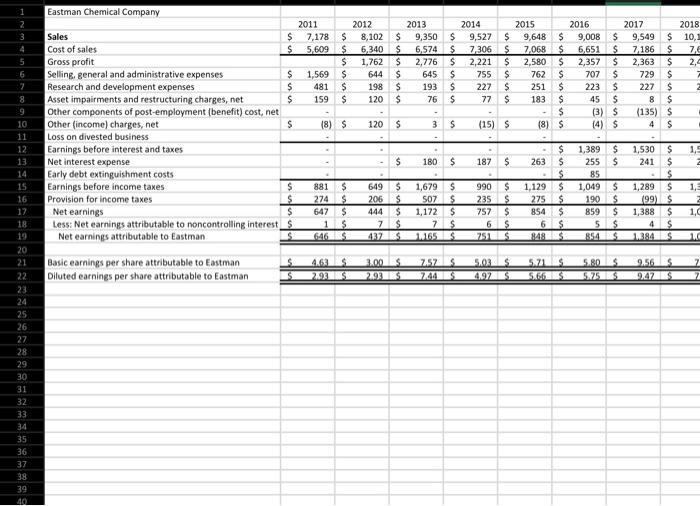

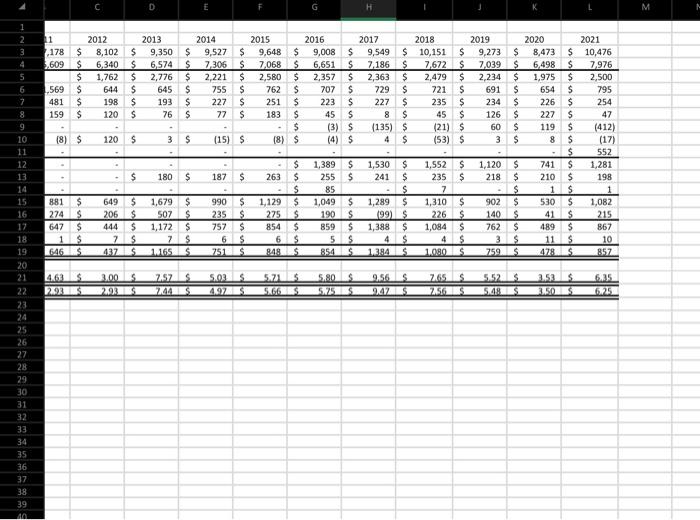

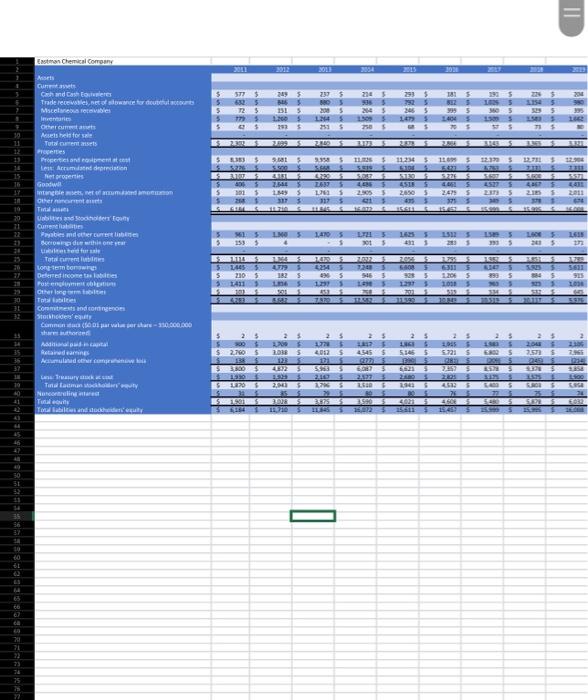

1. Use the income statement for your company to forecast the next three years of operations. 2. Use the balance sheet to forecast what it will look like the next year (one year, not three), Use the same end year you used for the income statement. 3. You may use any method you wish to perform the forecasts (see part 4). I will want you to defend the method you choose. Much will depend on how extensive or detailed the data is that you have to work with. Some of you have financial statements with lots of accounts specified, While others have basically summary accounts that are not as detailed. 4. Herearea few ways it could be done. a. Growth rates: i. If you use growth rates, it will not be a good idea to apply them to all accounts. For example, using past growth rates of net income may be misleading since net income is a function of revenues less expenses. So just grow the revenues and expenses, then do the subtraction to get net income. ii. Same goes for any amount that is derived from those accounts above it, such as EBIT. Don't grow that account, grow the accounts that make up EBIT, then calculate EBIT. b. Common Sizing both Balance Sheet and Income Statement. i. For the Income statement, it would seem to me that all you would need to do is forecast Sales or Revenue, and use the common sized percentages for the rest of the accounts. ii. For the one year of the Balance Sheet, seems to me only the Total Assets needs to be forecasted, and use the common size percentages for the rest of the accounts. iii. Personally, I would do the Income Statement before the Balance Sheet, because I would like to try to fit any forecasted retained earnings that get transferred to the balance sheet into the balance sheet forecast somehow. c. Indexing balance sheet and income statement. i. Perhaps use the change in the indexed numbers from the prior year or an average of the prior two years. ii. By indexing, one can pick out trends a little better. So if some accounts are growing faster than others so that can be taken into consideration when ] Eastman Chemical Company Sales Gross profit Selling, general and administrative expenses Research and development expenses Asset impairments and restructuring charges, net Other components of post-employment (benefit) cost, net Other (income) charges, net Loss on divested business Earnings before interest and taxes Net interest expense Early debt extinguishment costs Earnings before income taxes Provision for income taxes Net earnings Less: Net earnings attributable to noncontrolling interest Net earnings attributable to Eastman Basic earnings per share attributable to Eastman Diluted earnings per share attributable to Eastman \begin{tabular}{llllllllllllllll} 5 & 4.63 & 5 & 3.00 & 5 & 2.57 & 5 & 5.03 & 5 & 5.71 & 5 & 5.80 & 5 & 9.56 & 5 & 7 \\ \hline \hline 5 & 2.93 & 5 & 2.93 & 5 & 744 & 5 & 4.97 & 5 & 5.64 & 5 & 5.75 & 5 & 947 & 5 & 7 \\ \hline \hline \end{tabular} 1. Use the income statement for your company to forecast the next three years of operations. 2. Use the balance sheet to forecast what it will look like the next year (one year, not three). Use the same end year you used for the lncome statement. 3. You may use any method you wish to perform the forecasts (see part 4). I will want you to defend the method you choose. Much will depend on how extensive or detailed the data is that you have to work with. Some of you have financial statements with lots of accounts specified, while others have basically summary accounts that are not as detailed. 4. Here are a few ways it could be done. a. Growth rates: i. If you use growth rates, it will not be a good idea to apply them to all accounts. For cxample. using past growth rates of net income may be misleading since net income is a function of revenues less expenses. So just grow the revenues and expenses, then do the subtraction to get net income. ii. Same goes for any amount that is derived from those accounts above it, such as EBIT. Don't grow that account, grow the accounts that make up EBIT, then calculate EBIT. b. Common Sizing both Balance Shect and Income Statement. i. For the Income statement, it would seem to me that all you would need to do is forecast Sales or Revenue, and use the common sized percentages for the rest of the accounts. ii. For the one year of the Balance Sheet, seems to me only the Total Assets needs to be forecasted, and use the common size percentages for the rest of the accounts. iii. Personally, I would do the Income Statement before the Balance Sheet, because I would like to try to fit any forecasted retained earnings that get transferred to the balance sheet into the balance sheet forecast somehow. c. Indexing balance sheet and income statement. i. Perhaps use the change in the indexed numbers from the prior year or an average of the prior two years. ii. By indexing, one can pick out trends a little better. So if some accounts are growing faster than others so that can be taken into consideration when performing the forecasts on balance sheet and income statements. d. Using ratios from the prior year 1. Use the income statement for your company to forecast the next three years of operations. 2. Use the balance sheet to forecast what it will look like the next year (one year, not three), Use the same end year you used for the income statement. 3. You may use any method you wish to perform the forecasts (see part 4). I will want you to defend the method you choose. Much will depend on how extensive or detailed the data is that you have to work with. Some of you have financial statements with lots of accounts specified, While others have basically summary accounts that are not as detailed. 4. Herearea few ways it could be done. a. Growth rates: i. If you use growth rates, it will not be a good idea to apply them to all accounts. For example, using past growth rates of net income may be misleading since net income is a function of revenues less expenses. So just grow the revenues and expenses, then do the subtraction to get net income. ii. Same goes for any amount that is derived from those accounts above it, such as EBIT. Don't grow that account, grow the accounts that make up EBIT, then calculate EBIT. b. Common Sizing both Balance Sheet and Income Statement. i. For the Income statement, it would seem to me that all you would need to do is forecast Sales or Revenue, and use the common sized percentages for the rest of the accounts. ii. For the one year of the Balance Sheet, seems to me only the Total Assets needs to be forecasted, and use the common size percentages for the rest of the accounts. iii. Personally, I would do the Income Statement before the Balance Sheet, because I would like to try to fit any forecasted retained earnings that get transferred to the balance sheet into the balance sheet forecast somehow. c. Indexing balance sheet and income statement. i. Perhaps use the change in the indexed numbers from the prior year or an average of the prior two years. ii. By indexing, one can pick out trends a little better. So if some accounts are growing faster than others so that can be taken into consideration when ] Eastman Chemical Company Sales Gross profit Selling, general and administrative expenses Research and development expenses Asset impairments and restructuring charges, net Other components of post-employment (benefit) cost, net Other (income) charges, net Loss on divested business Earnings before interest and taxes Net interest expense Early debt extinguishment costs Earnings before income taxes Provision for income taxes Net earnings Less: Net earnings attributable to noncontrolling interest Net earnings attributable to Eastman Basic earnings per share attributable to Eastman Diluted earnings per share attributable to Eastman \begin{tabular}{llllllllllllllll} 5 & 4.63 & 5 & 3.00 & 5 & 2.57 & 5 & 5.03 & 5 & 5.71 & 5 & 5.80 & 5 & 9.56 & 5 & 7 \\ \hline \hline 5 & 2.93 & 5 & 2.93 & 5 & 744 & 5 & 4.97 & 5 & 5.64 & 5 & 5.75 & 5 & 947 & 5 & 7 \\ \hline \hline \end{tabular} 1. Use the income statement for your company to forecast the next three years of operations. 2. Use the balance sheet to forecast what it will look like the next year (one year, not three). Use the same end year you used for the lncome statement. 3. You may use any method you wish to perform the forecasts (see part 4). I will want you to defend the method you choose. Much will depend on how extensive or detailed the data is that you have to work with. Some of you have financial statements with lots of accounts specified, while others have basically summary accounts that are not as detailed. 4. Here are a few ways it could be done. a. Growth rates: i. If you use growth rates, it will not be a good idea to apply them to all accounts. For cxample. using past growth rates of net income may be misleading since net income is a function of revenues less expenses. So just grow the revenues and expenses, then do the subtraction to get net income. ii. Same goes for any amount that is derived from those accounts above it, such as EBIT. Don't grow that account, grow the accounts that make up EBIT, then calculate EBIT. b. Common Sizing both Balance Shect and Income Statement. i. For the Income statement, it would seem to me that all you would need to do is forecast Sales or Revenue, and use the common sized percentages for the rest of the accounts. ii. For the one year of the Balance Sheet, seems to me only the Total Assets needs to be forecasted, and use the common size percentages for the rest of the accounts. iii. Personally, I would do the Income Statement before the Balance Sheet, because I would like to try to fit any forecasted retained earnings that get transferred to the balance sheet into the balance sheet forecast somehow. c. Indexing balance sheet and income statement. i. Perhaps use the change in the indexed numbers from the prior year or an average of the prior two years. ii. By indexing, one can pick out trends a little better. So if some accounts are growing faster than others so that can be taken into consideration when performing the forecasts on balance sheet and income statements. d. Using ratios from the prior year