Question

Using the data in Table, compare the price on July 24, 2009, of the following options on JetBlue stock to the price predicted by the

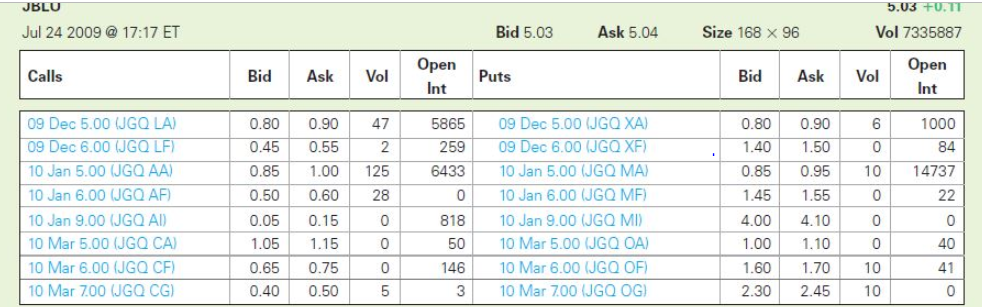

Using the data in Table, compare the price on July 24, 2009, of the following options on JetBlue stock to the price predicted by the Black-Scholes formula. Assume that the standard deviation of JetBlue stock is 64 % per year and that the short-term risk-free rate of interest is 1.1 % per year.  a. December 2009 call option with a $ 5.00 strike price. b. December 2009 put option with a $ 6.00 strike price. c. March 2010 put option with a $ 7.00 strike price

a. December 2009 call option with a $ 5.00 strike price. b. December 2009 put option with a $ 6.00 strike price. c. March 2010 put option with a $ 7.00 strike price

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Risk Management And Simulation

Authors: Aparna Gupta

1st Edition

1439835942,1439835950