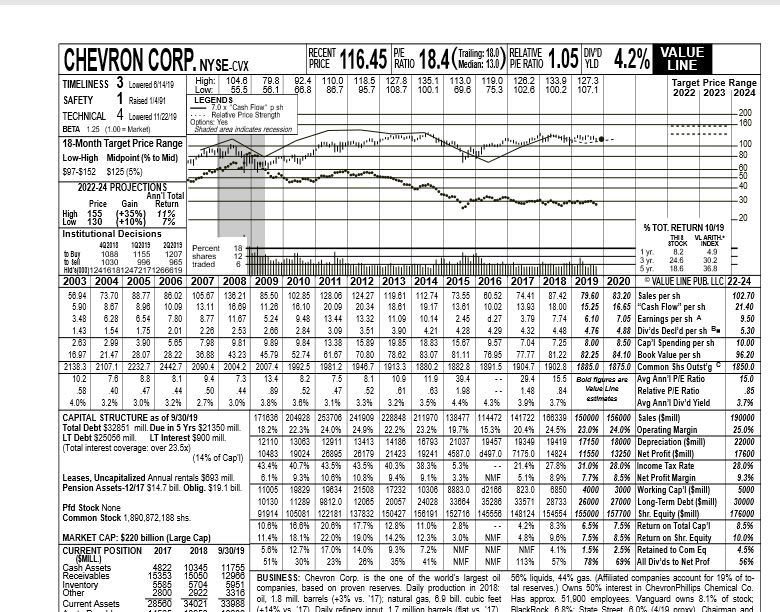

- Using the data in the VLIS, what is Chevrons Cost of Equity?

- For Chevrons Cost of Debt, consider the following bond quotation(settlement date Jan 31, 2020):

| Maturity | Coupon | Price | YTM |

| 3/16/2026 | 2.954 | $106.10 | |

- Using VLIS data, what is Chevrons LT Debt, and market capitalization? please see below - attached. Many Thanks!!!

-

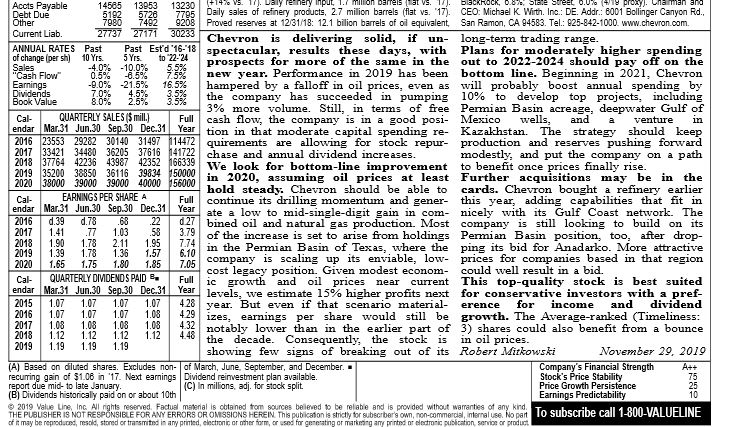

CHEVRON CORP. NYSE CVX TIMELINESS 3. Lowered B4419 tetor 1978 TECHNICAL 4 Lowered 112219 116.45 Km 18.4(edig 190BLATNE1.05 M 4.2% VALVE 110.9 98.9 12.19103. 8 79.9 12.3 1932.2 1871 A Target Price Range 2022 2023 2024 . . . ht SAFETY 1 Raised 1421 LEGENDS 70% Cash Flowsh ... Relative Prce Strength BETA 125 (100 - Market Shared area mecates recession 18-Month Target Price Range AZ Low-High Midpoint (% to Mid) $97-5152 $125(5%) 2022-24 PROJECTIONS Ann'l Total Price Gain Return 88 8888 VLAST % TOT. RETURN 10/19 Institutional Decisions 1929 193219 222119 Percent 18 OBN 106.8 1155 1207shares 124 traded 3 yr 246 HI1124161812472171266819 allan 5 yr 18.6 36.8 2003 2004 2005 2006 2007 2008 2009 2012 2013 2014 2015 2016 2017 2018 2019 2020 VALUE LINE PUB. LLC 22-24 58.94 73.70 88.77 88.02 105.67 136 21 85.50 102.85 80A 12427119.81 112.74 73.66 80.62 74.41 87.42 79.60 83.20 Sales per sh 102.70 5.90 8.87 8.98 10.09 13.11 16.89 11 28 18.10 20.09 20.34 18.81 19.17 13.81 10.02 13.93 18.00 15.25 16.65 Cash Flower Sh 2 1.40 3.48 6.28 6.54 7.80 8.77 11.67 524 9.48 13.44 13.32 11.09 10.14 2.45 d.27 3.79 7.74 6.10 7.05 Earnings per sh A 9.50 1.43 1.54 1.75 2.01 228 253 263 284 3.09 3.51 3.90 4.21 4.28 4.29 4.32 4.48 4.76 4.88 Div'ds Decl'd per sh B 5.30 2.63 2.99 3.90 5.65 7.98 981 9.89 9.84 13.33 15.89 19.85 18.83 15.67 9.57 7.04 7.25 8.00 8.50 Cap' Spending per sh 10.00 18.97 21.47 28.07 28 22 38.88 4323 45.79 52.74 81.67 70.80 78.62 83.07 81.11 78.95 77.77 81.22 82.25 84.10 Book Value per sh 96.20 2138. 3 2107.1 2252. 72442.7 2090.4 2004 2 2007.4 19925 1981.2 1946.7 1913. 3 1880218828 1891.5 1904.7 1902.8 1885.0 1875.0 Common Shs Outstg 1 850.0 10.2 78 8.8 8.1 9.4 73 13. 4 8 2 75 81 10.9 11. 9 39.4 .. 29.4 15.5 Bold Moures are Avg Ann' P/E Ratio 15.0 58 40 47 44 50 44 89 52 47 52 61 63 1.98 - 1.48 84 Value Line Relative PE Ratio 85 4.0% 3.2% 3.0% 32% 2.7% 3.09 3.89 3.8% 3.1% 3.3% 32% 35% 4.4% 4.3% 39% 3.79 estimates Avg Ann'l Div'd Yield 3.7% CAPITAL STRUCTURE as of 9/30/9 171638 204028 253708 241909 228848 211970 138477 114472 141722 168339 150000 156000 Sales (Smill) 190000 Total Debt 332851 mill. Due in 5 Yrs 321350 mill 18 2 34 24.09% 2499 22 2023 24 10.7% 153% 20.4% 24.59 23.0% 24.0% Operatina Margin 25.04 LT Debt $25068 mill. LT Interest $900 mill. 1211013063 1291113413 14186 18793 21037194571834919419 17150 18000 Depreciation (Smill) 22000 (Total interest coverage: over 23.5x) 1987 1 0483 19024 24895 28179 21423 19241 4587.0 d497.0 7175.0 14924 11550 13250 Net Profit milli 17600 43.4% 40.7% 43.5% 43.5% 40.39 38.3% 5.3% .. 21.4% 27.89 31.0% 28.0% Income Tax Rate 28.0% Leases, Uncapitalized Annual rentals $693 mill 8.1% 9,3% 10.6% 10.8% 9.4% 9.1% 3.3% NMF 5.1% 8.9% 7.7% 8.5% Net Profit Margin 9.34 Pension Assets-1277 $14.7 bil. Oblig. $19.1 bill 1125 19929 1934 216091729210308 8883002788 820 860 400 3000 Working Cap'lismilll 5000 10130 11289 98120 12065 20057 24028 33884 35288 33571 28733 26000 27000 Long-Term Debt ($mill) 30000 Pid Stock None 01914 106081 122181 137932 150427 158191 152718 146688 148124 154554 155000 157700 Shr. Equity Smill) 17600 Common Stock 1,890,872.188 shs. 10.6% 18.8% 20.6% 17.79 12.89 11.0% 2.8% 42% 8.39 6.5% 7.5% Return on Total Cap' 8.5% MARKET CAP: $220 billion (Large Cap) 11. 4 1 8.1 22.09 1909 14 29 12.24 3.04 NMF 48% 9.89 7.5% 8,5% Return on Shr. Equity 10.0% CURRENT POSITION 2017 2018 9/30/19 5,8% 12.7% 17.0% 14.09 9.3% 7.2% NMF NMF NMF 4.1% 1.5% 2.5% Retained to Com Eg 45% SMILL. 51% 30% 23% 20% 35% 41% NMF NMF 113% 57% 78% 69% All Div'ds to Net Prof 56% Cash Assets Receivables BUSINESS: Chevron Corp. is the one of the world's largest oil 56% liquids, 44% gas. Afiliated companies account for 19% of to- Inventory Other tal reserves.) Owns 50% interest in Chevron Phillips Chemical Co. 3316 companies, based on proven reserves. Daily production in 2018: Current Assets 28580 33988 oi, 1.8 mil. barrels (+3% vs. 17), natural gas, 6.2 bill. cubic feet Has approx. 51.800 employees. Vanguard owns 8.1% of stock: 1+14% vs 177 Daily renery input 17 million harrels at va "171 BlackRock 6 89 - State Street R 0% (4/19 i Chaman and 16665 12388 5951 assumnjevaon should bende gener Accts Payable 14585 13953 13230 (+14% VS. 1/1. Daly reenery Input, 1./ w on barrels Hat VS. 11. blackHOCK, 0.87 Side Sueel 0.0% 4/19 proxyl. Ulaman and Debt Due 5102 5720 Daily sales of refinery products, 2.7 milion barrels (flat vs. 17). CEO: Michael K Wirth. Inc.: DE. Addr: 8001 Bollinger Canyon Rd, Other 7980 7483 9208 Proved reserves at 12/31/18: 12.1 bilion barrels of oi equivalent San Ramon, CA 94583. Tel.: 025-842-1000. www.chevron.com Current Liab. 27737 27171 30233 Chevron is delivering solid, if un- long-term trading range. ANNUAL RATES Past Past Est'd '16-'18 spectacular, results these days, with Plans for moderately higher spending of change per sh] 10 Yrs 5 Yrs to 22-24 prospects for more of the same in the out to 2022-2024 should pay off on the Sales "Cash Flow new year. Performance in 2019 has been bottom line. Beginning in 2021. Chevron Earnings -9.0% 21.5% 16.5% hampered by a falloff in oil prices, even as will probably boost annual spending by Dividends Book Value 2.5% 3.5% the company has succeeded in pumping 10% to develop top projects, including 3% more volume. Still, in terms of free Permian Basin acreage, deepwater Gulf of Cal QUARTERLY SALES$ mill.) Full cash flow, the company is in a good posi- Mexico Full wells, and a venture in endar Mar 31 Jun.30 Sep.30 Dec.31 Year tion in that moderate capital spending re- Kazakhstan. The strategy should keep 2016 23553 29282 30140 31497 14472 quirements are allowing for stock repur- production and reserves pushing forward 2017 33421 34480 36205 37616 141722 chase and annual dividend increases. modestly, and put the company on a path 2018 37764 42236 43987 42352 166339 We look for bottom-line improvement to benefit once prices finally rise. 2019 35200 38850 36116 39834 50000 in 2020, assuming oil prices at least Further acquisitions may be in the 2020 38000 39000 39000 40000 56000 hold steady. Chevron should be able to cards. Chevron bought a refinery earlier Cal- EARNINGS PER SHARE A Full continue its drilling momentum and gener- this year, adding capabilities that fit in endar Mar 31 Jun 30 Sep.30 Dec.31 Year ate a low to mid-single-digit gain in com- nicely with its Gulf Coast network. The 2016 d.39 0.78 .68 22 d.27 bined oil and natural gas production. Most company is still looking to build on its 2017 1.41 .77 1.03 58 3.79 of the increase is set to arise from holdings Permian Basin position, too, after drop- 2018 1.90 1.78 2.11 1.95 7.74 2019 1.39 1.78 1.36 1.57 in the Permian Basin of Texas, where the ping its bid for Anadarko. More attractive 6.10 2020 1.65 1.75 1.80 1.85 7.05 company is scaling up its enviable, low- prices for companies based in that region cost legacy position. Given modest econom- could well result in a bid. Cal QUARTERLY DIVIDENDS PAID S. Full ic growth and oil prices near current This top-quality stock is best suited endar Mar 31 Jun 30 Sep 30 Dec.31 Year levels, we estimate 15% higher profits next for conservative investors with a pref- 2015 1,07 1,07 1,07 1,07 428 year. But even if that scenario material- erence for income and dividend 2016 1,07 1,07 1,07 1,08 429 izes, earnings per share would still be growth. The Average-ranked (Timeliness: 2017 1,08 1,08 1,08 1.08 4.32 notably lower than in the earlier part of 3) shares could also benefit from a bounce 2018 1.12 1.12 1.12 1.12 2019 1.19 1.19 1.19 the decade. Consequently, the stock is in oil prices. showing few signs of breaking out of its Robert Mitkowski November 29, 2019 (A) Based on diluted shares. Excludes non- of March, June. September, and December. Company's Financial Strength recurring gain of $1.06 in '17. Next earnings Dividend reinvestment plan available Stock's Price Stability report due mid- to late January. (C) In millions, adj. for stock split Price Growth Persistence (B) Dividends historically paid on or about 10th Earnings Predictability 2019 Value Line, IncAll rights reserved. Fachal material is obtained from sources believed to be reliable and is provided without warranties of any kind T. THE PUBUSHER IS NOT RESPONSIBLE FOR ANY ERRORS OR OMISSIONS HEREN This publication is strict or subsorberg own, non-comme nternalise a part to subscribe call 1-800-VALUFLINE of it may be reproduced, resold, stored or transmited in any printed, electronic or other form, or used for conting or making any printed of de publication service or product this CHEVRON CORP. NYSE CVX TIMELINESS 3. Lowered B4419 tetor 1978 TECHNICAL 4 Lowered 112219 116.45 Km 18.4(edig 190BLATNE1.05 M 4.2% VALVE 110.9 98.9 12.19103. 8 79.9 12.3 1932.2 1871 A Target Price Range 2022 2023 2024 . . . ht SAFETY 1 Raised 1421 LEGENDS 70% Cash Flowsh ... Relative Prce Strength BETA 125 (100 - Market Shared area mecates recession 18-Month Target Price Range AZ Low-High Midpoint (% to Mid) $97-5152 $125(5%) 2022-24 PROJECTIONS Ann'l Total Price Gain Return 88 8888 VLAST % TOT. RETURN 10/19 Institutional Decisions 1929 193219 222119 Percent 18 OBN 106.8 1155 1207shares 124 traded 3 yr 246 HI1124161812472171266819 allan 5 yr 18.6 36.8 2003 2004 2005 2006 2007 2008 2009 2012 2013 2014 2015 2016 2017 2018 2019 2020 VALUE LINE PUB. LLC 22-24 58.94 73.70 88.77 88.02 105.67 136 21 85.50 102.85 80A 12427119.81 112.74 73.66 80.62 74.41 87.42 79.60 83.20 Sales per sh 102.70 5.90 8.87 8.98 10.09 13.11 16.89 11 28 18.10 20.09 20.34 18.81 19.17 13.81 10.02 13.93 18.00 15.25 16.65 Cash Flower Sh 2 1.40 3.48 6.28 6.54 7.80 8.77 11.67 524 9.48 13.44 13.32 11.09 10.14 2.45 d.27 3.79 7.74 6.10 7.05 Earnings per sh A 9.50 1.43 1.54 1.75 2.01 228 253 263 284 3.09 3.51 3.90 4.21 4.28 4.29 4.32 4.48 4.76 4.88 Div'ds Decl'd per sh B 5.30 2.63 2.99 3.90 5.65 7.98 981 9.89 9.84 13.33 15.89 19.85 18.83 15.67 9.57 7.04 7.25 8.00 8.50 Cap' Spending per sh 10.00 18.97 21.47 28.07 28 22 38.88 4323 45.79 52.74 81.67 70.80 78.62 83.07 81.11 78.95 77.77 81.22 82.25 84.10 Book Value per sh 96.20 2138. 3 2107.1 2252. 72442.7 2090.4 2004 2 2007.4 19925 1981.2 1946.7 1913. 3 1880218828 1891.5 1904.7 1902.8 1885.0 1875.0 Common Shs Outstg 1 850.0 10.2 78 8.8 8.1 9.4 73 13. 4 8 2 75 81 10.9 11. 9 39.4 .. 29.4 15.5 Bold Moures are Avg Ann' P/E Ratio 15.0 58 40 47 44 50 44 89 52 47 52 61 63 1.98 - 1.48 84 Value Line Relative PE Ratio 85 4.0% 3.2% 3.0% 32% 2.7% 3.09 3.89 3.8% 3.1% 3.3% 32% 35% 4.4% 4.3% 39% 3.79 estimates Avg Ann'l Div'd Yield 3.7% CAPITAL STRUCTURE as of 9/30/9 171638 204028 253708 241909 228848 211970 138477 114472 141722 168339 150000 156000 Sales (Smill) 190000 Total Debt 332851 mill. Due in 5 Yrs 321350 mill 18 2 34 24.09% 2499 22 2023 24 10.7% 153% 20.4% 24.59 23.0% 24.0% Operatina Margin 25.04 LT Debt $25068 mill. LT Interest $900 mill. 1211013063 1291113413 14186 18793 21037194571834919419 17150 18000 Depreciation (Smill) 22000 (Total interest coverage: over 23.5x) 1987 1 0483 19024 24895 28179 21423 19241 4587.0 d497.0 7175.0 14924 11550 13250 Net Profit milli 17600 43.4% 40.7% 43.5% 43.5% 40.39 38.3% 5.3% .. 21.4% 27.89 31.0% 28.0% Income Tax Rate 28.0% Leases, Uncapitalized Annual rentals $693 mill 8.1% 9,3% 10.6% 10.8% 9.4% 9.1% 3.3% NMF 5.1% 8.9% 7.7% 8.5% Net Profit Margin 9.34 Pension Assets-1277 $14.7 bil. Oblig. $19.1 bill 1125 19929 1934 216091729210308 8883002788 820 860 400 3000 Working Cap'lismilll 5000 10130 11289 98120 12065 20057 24028 33884 35288 33571 28733 26000 27000 Long-Term Debt ($mill) 30000 Pid Stock None 01914 106081 122181 137932 150427 158191 152718 146688 148124 154554 155000 157700 Shr. Equity Smill) 17600 Common Stock 1,890,872.188 shs. 10.6% 18.8% 20.6% 17.79 12.89 11.0% 2.8% 42% 8.39 6.5% 7.5% Return on Total Cap' 8.5% MARKET CAP: $220 billion (Large Cap) 11. 4 1 8.1 22.09 1909 14 29 12.24 3.04 NMF 48% 9.89 7.5% 8,5% Return on Shr. Equity 10.0% CURRENT POSITION 2017 2018 9/30/19 5,8% 12.7% 17.0% 14.09 9.3% 7.2% NMF NMF NMF 4.1% 1.5% 2.5% Retained to Com Eg 45% SMILL. 51% 30% 23% 20% 35% 41% NMF NMF 113% 57% 78% 69% All Div'ds to Net Prof 56% Cash Assets Receivables BUSINESS: Chevron Corp. is the one of the world's largest oil 56% liquids, 44% gas. Afiliated companies account for 19% of to- Inventory Other tal reserves.) Owns 50% interest in Chevron Phillips Chemical Co. 3316 companies, based on proven reserves. Daily production in 2018: Current Assets 28580 33988 oi, 1.8 mil. barrels (+3% vs. 17), natural gas, 6.2 bill. cubic feet Has approx. 51.800 employees. Vanguard owns 8.1% of stock: 1+14% vs 177 Daily renery input 17 million harrels at va "171 BlackRock 6 89 - State Street R 0% (4/19 i Chaman and 16665 12388 5951 assumnjevaon should bende gener Accts Payable 14585 13953 13230 (+14% VS. 1/1. Daly reenery Input, 1./ w on barrels Hat VS. 11. blackHOCK, 0.87 Side Sueel 0.0% 4/19 proxyl. Ulaman and Debt Due 5102 5720 Daily sales of refinery products, 2.7 milion barrels (flat vs. 17). CEO: Michael K Wirth. Inc.: DE. Addr: 8001 Bollinger Canyon Rd, Other 7980 7483 9208 Proved reserves at 12/31/18: 12.1 bilion barrels of oi equivalent San Ramon, CA 94583. Tel.: 025-842-1000. www.chevron.com Current Liab. 27737 27171 30233 Chevron is delivering solid, if un- long-term trading range. ANNUAL RATES Past Past Est'd '16-'18 spectacular, results these days, with Plans for moderately higher spending of change per sh] 10 Yrs 5 Yrs to 22-24 prospects for more of the same in the out to 2022-2024 should pay off on the Sales "Cash Flow new year. Performance in 2019 has been bottom line. Beginning in 2021. Chevron Earnings -9.0% 21.5% 16.5% hampered by a falloff in oil prices, even as will probably boost annual spending by Dividends Book Value 2.5% 3.5% the company has succeeded in pumping 10% to develop top projects, including 3% more volume. Still, in terms of free Permian Basin acreage, deepwater Gulf of Cal QUARTERLY SALES$ mill.) Full cash flow, the company is in a good posi- Mexico Full wells, and a venture in endar Mar 31 Jun.30 Sep.30 Dec.31 Year tion in that moderate capital spending re- Kazakhstan. The strategy should keep 2016 23553 29282 30140 31497 14472 quirements are allowing for stock repur- production and reserves pushing forward 2017 33421 34480 36205 37616 141722 chase and annual dividend increases. modestly, and put the company on a path 2018 37764 42236 43987 42352 166339 We look for bottom-line improvement to benefit once prices finally rise. 2019 35200 38850 36116 39834 50000 in 2020, assuming oil prices at least Further acquisitions may be in the 2020 38000 39000 39000 40000 56000 hold steady. Chevron should be able to cards. Chevron bought a refinery earlier Cal- EARNINGS PER SHARE A Full continue its drilling momentum and gener- this year, adding capabilities that fit in endar Mar 31 Jun 30 Sep.30 Dec.31 Year ate a low to mid-single-digit gain in com- nicely with its Gulf Coast network. The 2016 d.39 0.78 .68 22 d.27 bined oil and natural gas production. Most company is still looking to build on its 2017 1.41 .77 1.03 58 3.79 of the increase is set to arise from holdings Permian Basin position, too, after drop- 2018 1.90 1.78 2.11 1.95 7.74 2019 1.39 1.78 1.36 1.57 in the Permian Basin of Texas, where the ping its bid for Anadarko. More attractive 6.10 2020 1.65 1.75 1.80 1.85 7.05 company is scaling up its enviable, low- prices for companies based in that region cost legacy position. Given modest econom- could well result in a bid. Cal QUARTERLY DIVIDENDS PAID S. Full ic growth and oil prices near current This top-quality stock is best suited endar Mar 31 Jun 30 Sep 30 Dec.31 Year levels, we estimate 15% higher profits next for conservative investors with a pref- 2015 1,07 1,07 1,07 1,07 428 year. But even if that scenario material- erence for income and dividend 2016 1,07 1,07 1,07 1,08 429 izes, earnings per share would still be growth. The Average-ranked (Timeliness: 2017 1,08 1,08 1,08 1.08 4.32 notably lower than in the earlier part of 3) shares could also benefit from a bounce 2018 1.12 1.12 1.12 1.12 2019 1.19 1.19 1.19 the decade. Consequently, the stock is in oil prices. showing few signs of breaking out of its Robert Mitkowski November 29, 2019 (A) Based on diluted shares. Excludes non- of March, June. September, and December. Company's Financial Strength recurring gain of $1.06 in '17. Next earnings Dividend reinvestment plan available Stock's Price Stability report due mid- to late January. (C) In millions, adj. for stock split Price Growth Persistence (B) Dividends historically paid on or about 10th Earnings Predictability 2019 Value Line, IncAll rights reserved. Fachal material is obtained from sources believed to be reliable and is provided without warranties of any kind T. THE PUBUSHER IS NOT RESPONSIBLE FOR ANY ERRORS OR OMISSIONS HEREN This publication is strict or subsorberg own, non-comme nternalise a part to subscribe call 1-800-VALUFLINE of it may be reproduced, resold, stored or transmited in any printed, electronic or other form, or used for conting or making any printed of de publication service or product this