Answered step by step

Verified Expert Solution

Question

1 Approved Answer

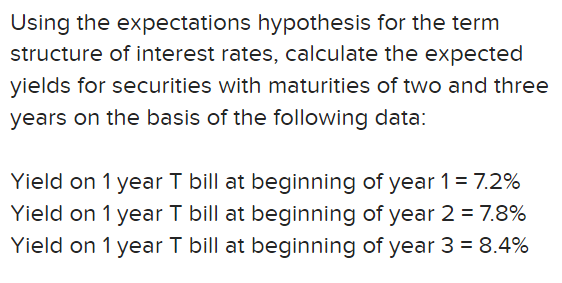

Using the expectations hypothesis for the term structure of interest rates, calculate the expected yields for securities with maturities of two and three years on

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Private Capital Markets Valuation Capitalization And Transfer Of Private Business Interests

Authors: Robert T. Slee

2nd Edition

0470928328, 978-0470928325