Question

Using the information provided by the case, particularly in the Spotifys section Valuation, will carry out a valuation of the company and its shares using

Using the information provided by the case, particularly in the Spotifys section Valuation, will carry out a valuation of the company and its shares using the method Discounted Cash Flow (DFC). They will use the 2017 figures as the base year (Revenues: 4,090) and will estimate the flow of Cash (Free Cash Flow) for the years 2018 to 2027. Below, the source of the data they will use for the DCF:

Account / Item Section and / or Spotify case page Revenue (2017) Page 5

| Account | Item Section or Page |

| Revenue (2017) | Page 5 |

| Revenue Growth EBIT Margin Tax Rate CAPEX- DEP+ WC Shares Outstanding | Page 5 and 6 Exhibit 10: Page 17 Page 6 Exhibit 10: Page 17 Page 6 |

| Cost F Capital | |

| Risk Free Rate | 2.85% |

| Beta | 1.15 |

| Market Risk Premium (MRP) | 5.% |

| Ke (Cost of Equity) | Rf + Beta x MRP |

| We (proportion of equity) | 1. |

| Weighted average cost of capital (WACC) | |

| Growth Rate | 3.% |

PLEASE EXCEL TEMPLATE TO SEE I will give thumbs up HELP!!!!!

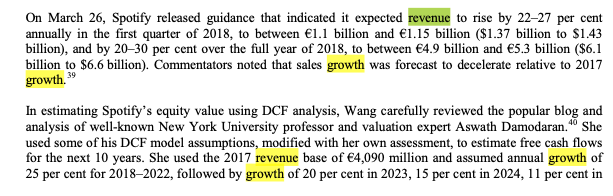

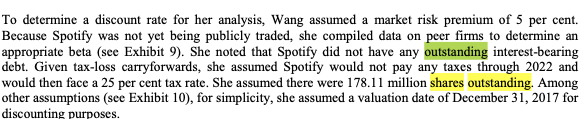

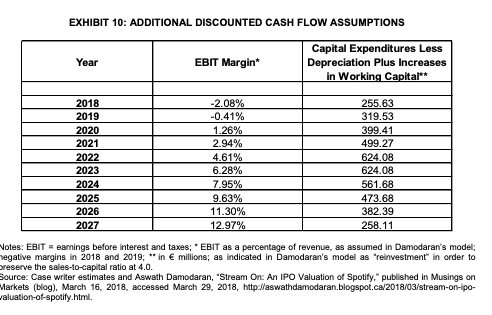

To determine a discount rate for her analysis, Wang assumed a market risk premium of 5 per cent. Because Spotify was not yet being publicly traded, she compiled data on peer firms to determine an appropriate beta (see Exhibit 9). She noted that Spotify did not have any outstanding interest-bearing debt. Given tax-loss carryforwards, she assumed Spotify would not pay any taxes through 2022 and would then face a 25 per cent tax rate. She assumed there were 178.11 million shares outstanding. Among other assumptions (see Exhibit 10), for simplicity, she assumed a valuation date of December 31, 2017 for discounting purposes. On March 26, Spotify released guidance that indicated it expected revenue to rise by 22-27 per cent annually in the first quarter of 2018, to between 1.1 billion and 1.15 billion ($1.37 billion to $1.43 billion), and by 20-30 per cent over the full year of 2018, to between 4.9 billion and 5.3 billion ($6.1 billion to $6.6 billion). Commentators noted that sales growth was forecast to decelerate relative to 2017 growth. 39 In estimating Spotify's equity value using DCF analysis, Wang carefully reviewed the popular blog and analysis of well-known New York University professor and valuation expert Aswath Damodaran." She used some of his DCF model assumptions, modified with her own assessment, to estimate free cash flows for the next 10 years. She used the 2017 revenue base of 4,090 million and assumed annual growth of 25 per cent for 20182022, followed by growth of 20 per cent in 2023, 15 per cent in 2024, 11 per cent in To determine a discount rate for her analysis, Wang assumed a market risk premium of 5 per cent. Because Spotify was not yet being publicly traded, she compiled data on peer firms to determine an appropriate beta (see Exhibit 9). She noted that Spotify did not have any outstanding interest-bearing debt. Given tax-loss carryforwards, she assumed Spotify would not pay any taxes through 2022 and would then face a 25 per cent tax rate. She assumed there were 178.11 million shares outstanding. Among other assumptions (sce Exhibit 10), for simplicity, she assumed a valuation date of December 31, 2017 for discounting purposes. EXHIBIT 10: ADDITIONAL DISCOUNTED CASH FLOW ASSUMPTIONS Year EBIT Margin* Capital Expenditures Less Depreciation Plus Increases in Working Capital** 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 -2.08% -0.41% 1.26% 2.94% 4.61% 6.28% 7.95% 9.63% 11.30% 12.97% 255.63 319.53 399.41 499.27 624.08 624.08 561.68 473.68 382.39 258.11 Notes: EBIT = earnings before interest and taxes: EBIT as a percentage of revenue, as assumed in Damodaran's model: negative margins in 2018 and 2019in millions; as indicated in Damodaran's model as "reinvestment in order to reserve the sales-to-capital ratio at 4.0. Source: Case writer estimates and Aswath Damodaran, "Stream On: An IPO Valuation of Spotify," published in Musings on Markets (blog), March 16, 2018. accessed March 29, 2018, http://aswathdamodaran.blogspot.ca/2018/03/stream-on-ipo- Jaluation-of-spotify.html To determine a discount rate for her analysis, Wang assumed a market risk premium of 5 per cent. Because Spotify was not yet being publicly traded, she compiled data on peer firms to determine an appropriate beta (see Exhibit 9). She noted that Spotify did not have any outstanding interest-bearing debt. Given tax-loss carryforwards, she assumed Spotify would not pay any taxes through 2022 and would then face a 25 per cent tax rate. She assumed there were 178.11 million shares outstanding. Among other assumptions (see Exhibit 10), for simplicity, she assumed a valuation date of December 31, 2017 for discounting purposes. On March 26, Spotify released guidance that indicated it expected revenue to rise by 22-27 per cent annually in the first quarter of 2018, to between 1.1 billion and 1.15 billion ($1.37 billion to $1.43 billion), and by 20-30 per cent over the full year of 2018, to between 4.9 billion and 5.3 billion ($6.1 billion to $6.6 billion). Commentators noted that sales growth was forecast to decelerate relative to 2017 growth. 39 In estimating Spotify's equity value using DCF analysis, Wang carefully reviewed the popular blog and analysis of well-known New York University professor and valuation expert Aswath Damodaran." She used some of his DCF model assumptions, modified with her own assessment, to estimate free cash flows for the next 10 years. She used the 2017 revenue base of 4,090 million and assumed annual growth of 25 per cent for 20182022, followed by growth of 20 per cent in 2023, 15 per cent in 2024, 11 per cent in To determine a discount rate for her analysis, Wang assumed a market risk premium of 5 per cent. Because Spotify was not yet being publicly traded, she compiled data on peer firms to determine an appropriate beta (see Exhibit 9). She noted that Spotify did not have any outstanding interest-bearing debt. Given tax-loss carryforwards, she assumed Spotify would not pay any taxes through 2022 and would then face a 25 per cent tax rate. She assumed there were 178.11 million shares outstanding. Among other assumptions (sce Exhibit 10), for simplicity, she assumed a valuation date of December 31, 2017 for discounting purposes. EXHIBIT 10: ADDITIONAL DISCOUNTED CASH FLOW ASSUMPTIONS Year EBIT Margin* Capital Expenditures Less Depreciation Plus Increases in Working Capital** 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 -2.08% -0.41% 1.26% 2.94% 4.61% 6.28% 7.95% 9.63% 11.30% 12.97% 255.63 319.53 399.41 499.27 624.08 624.08 561.68 473.68 382.39 258.11 Notes: EBIT = earnings before interest and taxes: EBIT as a percentage of revenue, as assumed in Damodaran's model: negative margins in 2018 and 2019in millions; as indicated in Damodaran's model as "reinvestment in order to reserve the sales-to-capital ratio at 4.0. Source: Case writer estimates and Aswath Damodaran, "Stream On: An IPO Valuation of Spotify," published in Musings on Markets (blog), March 16, 2018. accessed March 29, 2018, http://aswathdamodaran.blogspot.ca/2018/03/stream-on-ipo- Jaluation-of-spotify.htmlStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

College Accounting A Practical Approach Chapters 1-25

Authors: Jeffrey Slater, Mike Deschamps

15th Edition

0137504284, 9780137504282