Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Using the same data as for Problem 2 3 , calculate the expected return and the volatility ( standard deviation ) of a portfolio consisting

Using the same data as for Problem calculate the expected return and the volatility standard deviation of a portfolio consisting of Johnson & Johnsons and Walgreens stocks using a wide range of portfolio weights. Plot the expected return as a function of the portfolio volatility.

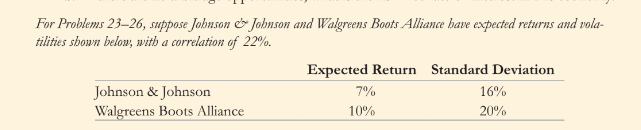

Using your graph, identify the range of Johnson & Johnsons portfolio weights that yield eficient combinations of the two stocks, rounded to the nearest percentage point.For Problems suppose Jobnson & Johnson and Walgreens Boots. Alliance have expected returns and volatilities shown below, with a correlation of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ISE Real Estate Finance And Investments

Authors: Jeffrey Fisher William B. Brueggeman

17th International Edition

1264892888, 9781264892884