Question

Using the table attached below, plot the opportunity set of risky assets in Excel. Then vary the correlation between stocks and bonds from + 1

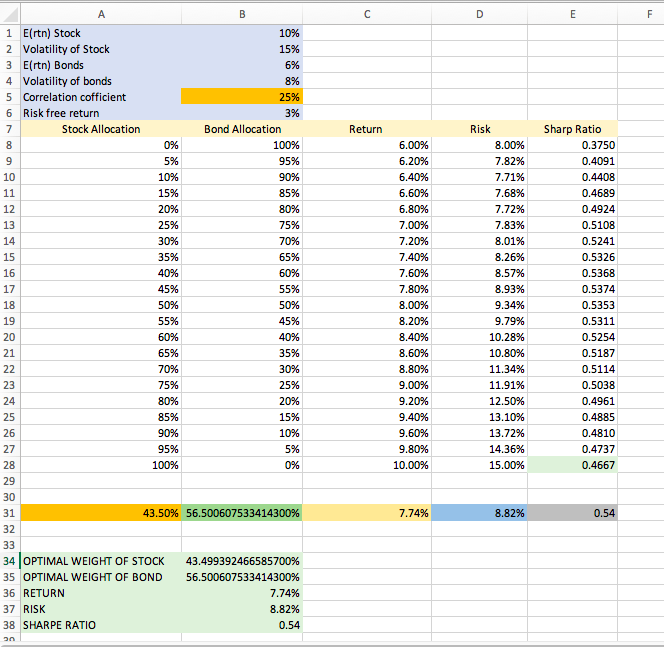

Using the table attached below, plot the opportunity set of risky assets in Excel. Then vary the correlation between stocks and bonds from + 1 to -1 and describe the changes in shape of the efficient frontier as you do so. Upload the Excel file that contains the table & graph. Also include in Excel file a description of the efficient frontier's shape as you vary the correlation.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Concepts And Practice Of Mathematical Finance

Authors: Mark S. Joshi

2nd Edition

0521514088, 9780521514088