Answered step by step

Verified Expert Solution

Question

1 Approved Answer

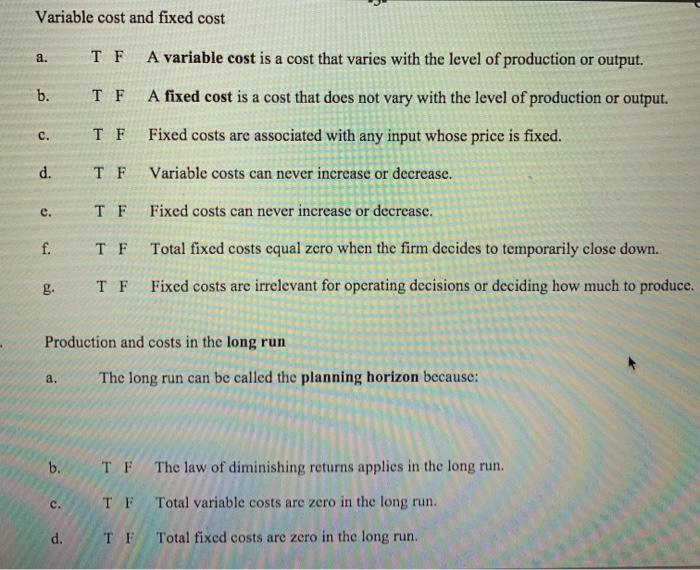

Variable cost and fixed cost a. b. C. d. S f. g. a. b. C. T F A variable cost is a cost that

Variable cost and fixed cost a. b. C. d. S f. g. a. b. C. T F A variable cost is a cost that varies with the level of production or output. A fixed cost is a cost that does not vary with the level of production or output. Fixed costs are associated with any input whose price is fixed. Variable costs can never increase or decrease. Fixed costs can never increase or decrease. Total fixed costs equal zero when the firm decides to temporarily close down. Fixed costs are irrelevant for operating decisions or deciding how much to produce. d. T F T F T F Production and costs in the long run T F T F TF The long run can be called the planning horizon because: TF The law of diminishing returns applies in the long run. Total variable costs are zero in the long run. TF Total fixed costs are zero in the long run.

Step by Step Solution

★★★★★

3.44 Rating (157 Votes )

There are 3 Steps involved in it

Step: 1

a Answer True Explanation Variable cost are cost that change with the level of production When more of a commodity is produced variable cost increase ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516