very urgent Thanks!Question 1

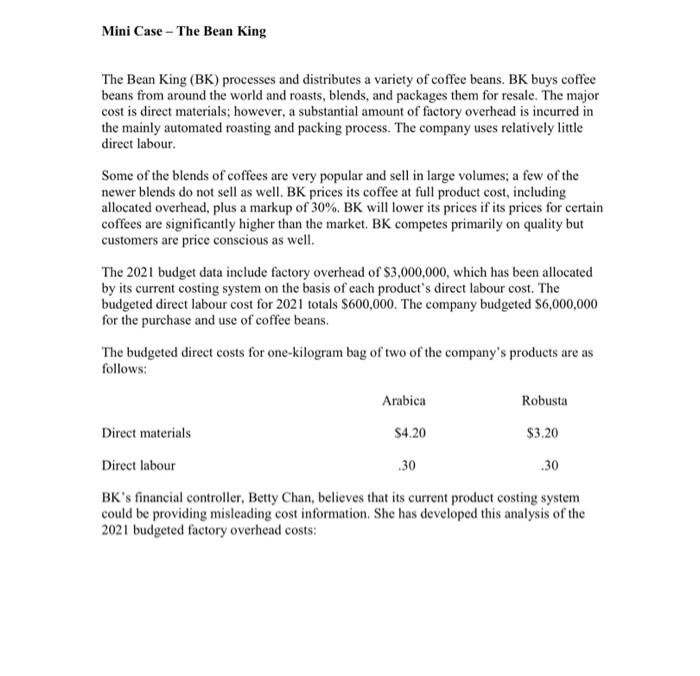

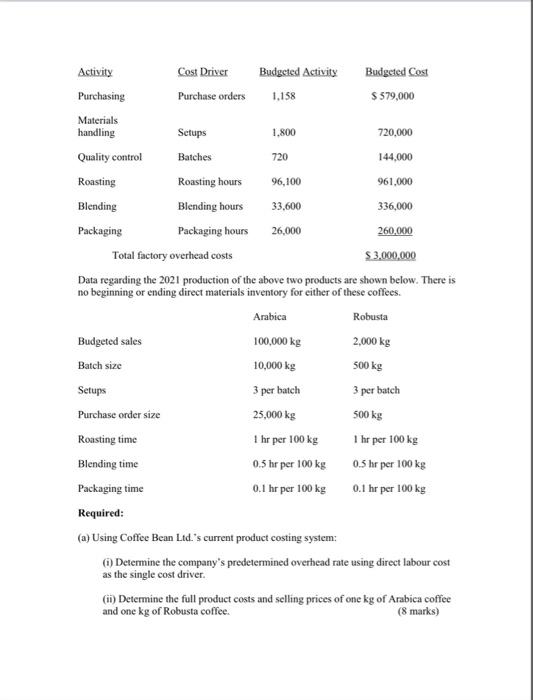

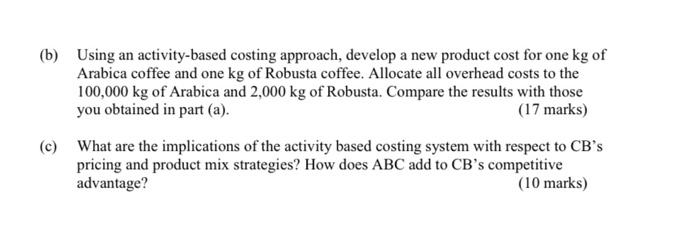

Mini Case - The Bean King The Bean King (BK) processes and distributes a variety of coffee beans. BK buys coffee beans from around the world and roasts, blends, and packages them for resale. The major cost is direct materials; however, a substantial amount of factory overhead is incurred in the mainly automated roasting and packing process. The company uses relatively little direct labour. Some of the blends of coffees are very popular and sell in large volumes; a few of the newer blends do not sell as well. BK prices its coffee at full product cost, including allocated overhead, plus a markup of 30%. BK will lower its prices if its prices for certain coffees are significantly higher than the market. BK competes primarily on quality but customers are price conscious as well. The 2021 budget data include factory overhead of $3,000,000, which has been allocated by its current costing system on the basis of each product's direct labour cost. The budgeted direct labour cost for 2021 totals $600,000. The company budgeted $6,000,000 for the purchase and use of coffee beans. The budgeted direct costs for one-kilogram bag of two of the company's products are as follows: Arabica Robusta Direct materials $4.20 $3.20 Direct labour .30 BK's financial controller, Betty Chan, believes that its current product costing system could be providing misleading cost information. She has developed this analysis of the 2021 budgeted factory overhead costs: .30 Activity Cost Driver Budgeted Activity Budgeted Cost Purchasing Purchase orders 1.158 $ 579,000 Materials handling Setups 1.800 720,000 Quality control Batches 720 144,000 Roasting Roasting hours 96,100 961.000 Blending Blending hours 33.600 336,000 Packaging Packaging hours 26,000 260,000 Total factory overhead costs $3,000,000 Data regarding the 2021 production of the above two products are shown below. There is no beginning or ending direct materials inventory for either of these coffees. Arabica Robusta Budgeted sales 100,000 kg 2,000 kg Batch size 10,000 kg 500 kg Setups 3 per batch 3 per batch Purchase order size 25,000 kg 500 kg Roasting time 1 hr per 100 kg 1 hr per 100 kg Blending time 0.5 hr per 100 kg 0.5 hr per 100 kg Packaging time 0.1 hr per 100 kg 0.1 hr per 100 kg Required: (a) Using Coffee Bean Ltd.'s current product costing system: Determine the company's predetermined overhead rate using direct labour cost as the single cost driver. (1) Determine the full product costs and selling prices of one kg of Arabica coffee and one kg of Robusta coffee. (8 marks) (b) Using an activity-based costing approach, develop a new product cost for one kg of Arabica coffee and one kg of Robusta coffee. Allocate all overhead costs to the 100,000 kg of Arabica and 2,000 kg of Robusta. Compare the results with those you obtained in part (a). (17 marks) (c) What are the implications of the activity based costing system with respect to CB's pricing and product mix strategies? How does ABC add to CB's competitive advantage? (10 marks)