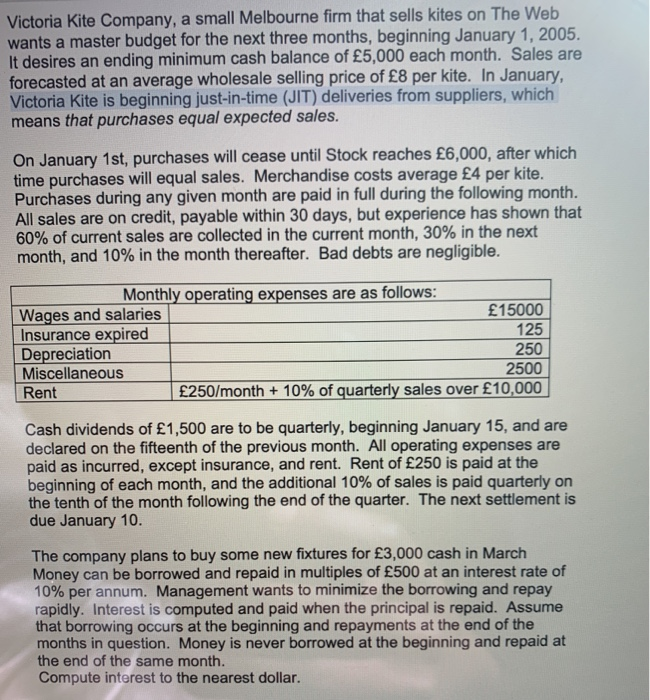

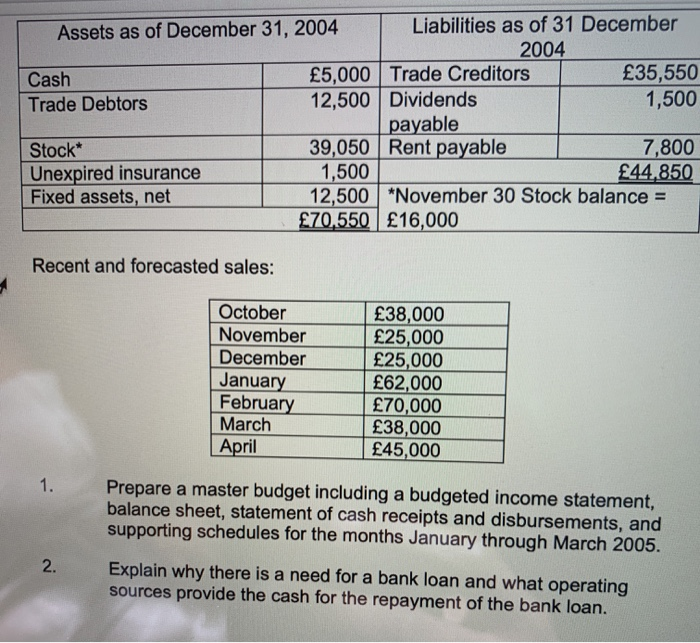

Victoria Kite Company, a small Melbourne firm that sells kites on the Web wants a master budget for the next three months, beginning January 1, 2005. It desires an ending minimum cash balance of 5,000 each month. Sales are forecasted at an average wholesale selling price of 8 per kite. In January, Victoria Kite is beginning just-in-time (JIT) deliveries from suppliers, which means that purchases equal expected sales. On January 1st, purchases will cease until Stock reaches 6,000, after which time purchases will equal sales. Merchandise costs average 4 per kite. Purchases during any given month are paid in full during the following month. All sales are on credit, payable within 30 days, but experience has shown that 60% of current sales are collected in the current month, 30% in the next month, and 10% in the month thereafter. Bad debts are negligible. Monthly operating expenses are as follows: Wages and salaries 15000 Insurance expired 125 Depreciation 250 Miscellaneous 2500 Rent 250/month + 10% of quarterly sales over 10,000 Cash dividends of 1,500 are to be quarterly, beginning January 15, and are declared on the fifteenth of the previous month. All operating expenses are paid as incurred, except insurance, and rent. Rent of 250 is paid at the beginning of each month, and the additional 10% of sales is paid quarterly on the tenth of the month following the end of the quarter. The next settlement is due January 10. The company plans to buy some new fixtures for 3,000 cash in March Money can be borrowed and repaid in multiples of 500 at an interest rate of 10% per annum. Management wants to minimize the borrowing and repay rapidly. Interest is computed and paid when the principal is repaid. Assume that borrowing occurs at the beginning and repayments at the end of the months in question. Money is never borrowed at the beginning and repaid at the end of the same month. Compute interest to the nearest dollar. Assets as of December 31, 2004 Liabilities as of 31 December 2004 Cash 5,000 Trade Creditors 35,550 Trade Debtors 12,500 Dividends 1,500 payable Stock* 39,050 Rent payable 7,800 Unexpired insurance 1,500 44.850 Fixed assets, net 12,500 *November 30 Stock balance = 70,550 16,000 Recent and forecasted sales: October November December January February March April 38,000 25,000 25,000 62,000 70,000 38,000 45,000 1. Prepare a master budget including a budgeted income statement, balance sheet, statement of cash receipts and disbursements, and supporting schedules for the months January through March 2005. 2. Explain why there is a need for a bank loan and what operating sources provide the cash for the repayment of the bank loan. Victoria Kite Company, a small Melbourne firm that sells kites on the Web wants a master budget for the next three months, beginning January 1, 2005. It desires an ending minimum cash balance of 5,000 each month. Sales are forecasted at an average wholesale selling price of 8 per kite. In January, Victoria Kite is beginning just-in-time (JIT) deliveries from suppliers, which means that purchases equal expected sales. On January 1st, purchases will cease until Stock reaches 6,000, after which time purchases will equal sales. Merchandise costs average 4 per kite. Purchases during any given month are paid in full during the following month. All sales are on credit, payable within 30 days, but experience has shown that 60% of current sales are collected in the current month, 30% in the next month, and 10% in the month thereafter. Bad debts are negligible. Monthly operating expenses are as follows: Wages and salaries 15000 Insurance expired 125 Depreciation 250 Miscellaneous 2500 Rent 250/month + 10% of quarterly sales over 10,000 Cash dividends of 1,500 are to be quarterly, beginning January 15, and are declared on the fifteenth of the previous month. All operating expenses are paid as incurred, except insurance, and rent. Rent of 250 is paid at the beginning of each month, and the additional 10% of sales is paid quarterly on the tenth of the month following the end of the quarter. The next settlement is due January 10. The company plans to buy some new fixtures for 3,000 cash in March Money can be borrowed and repaid in multiples of 500 at an interest rate of 10% per annum. Management wants to minimize the borrowing and repay rapidly. Interest is computed and paid when the principal is repaid. Assume that borrowing occurs at the beginning and repayments at the end of the months in question. Money is never borrowed at the beginning and repaid at the end of the same month. Compute interest to the nearest dollar. Assets as of December 31, 2004 Liabilities as of 31 December 2004 Cash 5,000 Trade Creditors 35,550 Trade Debtors 12,500 Dividends 1,500 payable Stock* 39,050 Rent payable 7,800 Unexpired insurance 1,500 44.850 Fixed assets, net 12,500 *November 30 Stock balance = 70,550 16,000 Recent and forecasted sales: October November December January February March April 38,000 25,000 25,000 62,000 70,000 38,000 45,000 1. Prepare a master budget including a budgeted income statement, balance sheet, statement of cash receipts and disbursements, and supporting schedules for the months January through March 2005. 2. Explain why there is a need for a bank loan and what operating sources provide the cash for the repayment of the bank loan