Question

Video transcript: Modified internal rate of return. Decision-makers tend to like using rates of return when they compare projects, mostly because they're simple and easy

Video transcript: Modified internal rate of return. Decision-makers tend to like using rates of return when they compare projects, mostly because they're simple and easy to understand. So it's no wonder that the internal rate of return gets used a lot in capital budgeting. But unfortunately, it's not that great of a measure of a project's true return. This is mostly due to the fact that, at its heart, the internal rate of return makes a faulty assumption. It assumes that a project's cash flows can be reinvested at the project's internal rate of return, but this simply isn't realistic. Why not? Well, if a company's getting a really high return on a project, chances are that other firms will come along and try and get in on the action. This competition will make it difficult for the company to find similar projects with such high returns to invest in. In the real world, they're probably going to have to settle for a significantly lower reinvestment rate, so the IRR overstates a project's true return. Fortunately, there is a better measure of a project's rate of return that takes this reality into account. The modified internal rate of return improves on the basic internal rate of return by assuming that a project's cash flows are reinvested at the firm's weighted average cost of capital. This is the actual rate the company pays when it goes out and raises money in the market to invest in their projects, so it's a much more realistic reinvestment rate. So by correcting the faulty assumption inherent in the internal rate of return, the modified internal rate of return provides a return measure that's more useful for managers who have to do business in the real world. That's the value of the modified internal rate of return.

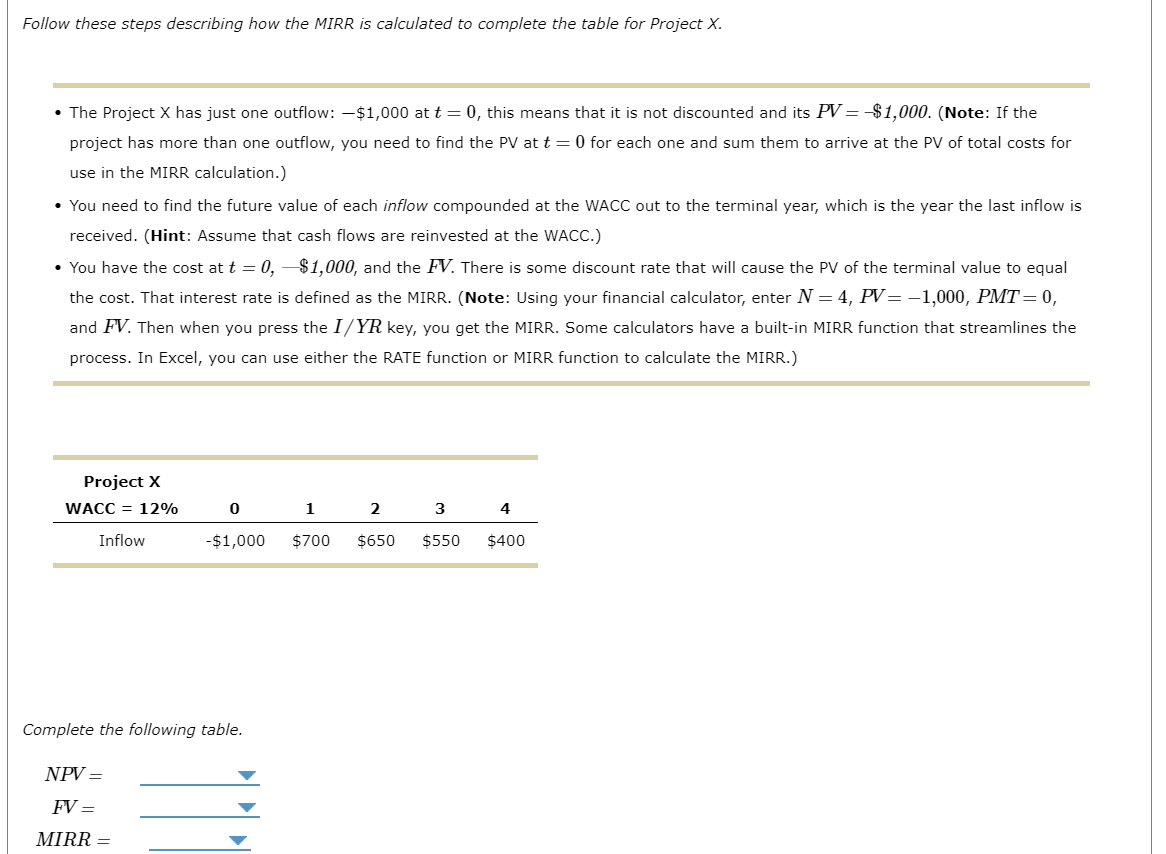

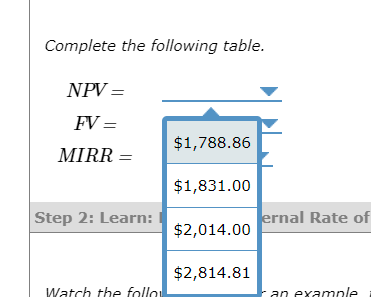

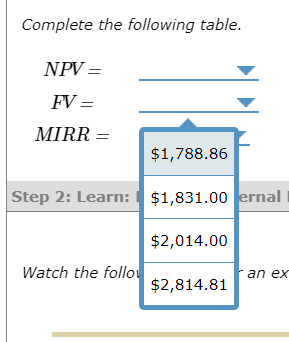

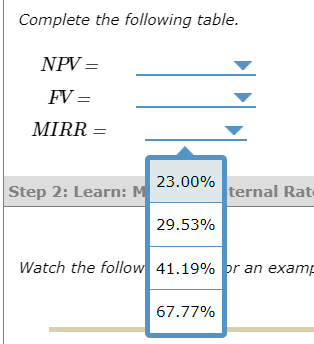

Complete the following table. Follow these steps describing how the MIRR is calculated to complete the table for Project X. - The Project X has just one outflow: $1,000 at t=0, this means that it is not discounted and its PV=$1,000. (Note: If the project has more than one outflow, you need to find the PV at t=0 for each one and sum them to arrive at the PV of total costs for use in the MIRR calculation.) - You need to find the future value of each inflow compounded at the WACC out to the terminal year, which is the year the last inflow is received. (Hint: Assume that cash flows are reinvested at the WACC.) - You have the cost at t=0,$1,000, and the FV. There is some discount rate that will cause the PV of the terminal value to equal the cost. That interest rate is defined as the MIRR. (Note: Using your financial calculator, enter N=4,PV=1,000,PMT=0, and FV. Then when you press the I/YR key, you get the MIRR. Some calculators have a built-in MIRR function that streamlines the process. In Excel, you can use either the RATE function or MIRR function to calculate the MIRR.) Complete the following table. NPV=FV=MIRR= According to the video, the calculations of the IRR is based on the assumption that cash flows can be reinvested at: the IRR. the MIRR. the NPV. the WACC. Complete the following table. Complete the following table

Complete the following table. Follow these steps describing how the MIRR is calculated to complete the table for Project X. - The Project X has just one outflow: $1,000 at t=0, this means that it is not discounted and its PV=$1,000. (Note: If the project has more than one outflow, you need to find the PV at t=0 for each one and sum them to arrive at the PV of total costs for use in the MIRR calculation.) - You need to find the future value of each inflow compounded at the WACC out to the terminal year, which is the year the last inflow is received. (Hint: Assume that cash flows are reinvested at the WACC.) - You have the cost at t=0,$1,000, and the FV. There is some discount rate that will cause the PV of the terminal value to equal the cost. That interest rate is defined as the MIRR. (Note: Using your financial calculator, enter N=4,PV=1,000,PMT=0, and FV. Then when you press the I/YR key, you get the MIRR. Some calculators have a built-in MIRR function that streamlines the process. In Excel, you can use either the RATE function or MIRR function to calculate the MIRR.) Complete the following table. NPV=FV=MIRR= According to the video, the calculations of the IRR is based on the assumption that cash flows can be reinvested at: the IRR. the MIRR. the NPV. the WACC. Complete the following table. Complete the following table Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Budgets And Financial Management In Higher Education

Authors: Margaret J. Barr, George S. McClellan

3rd Edition

1119287731, 9781119287735