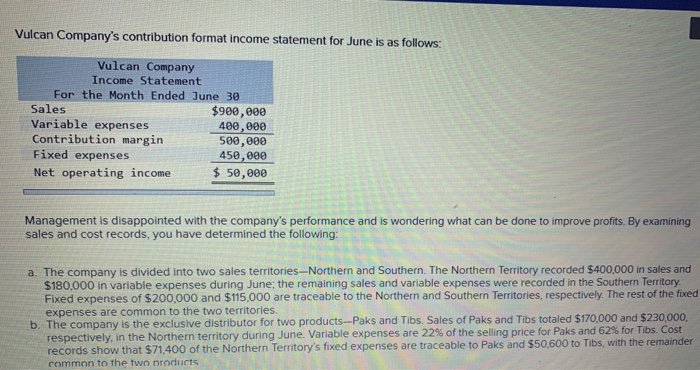

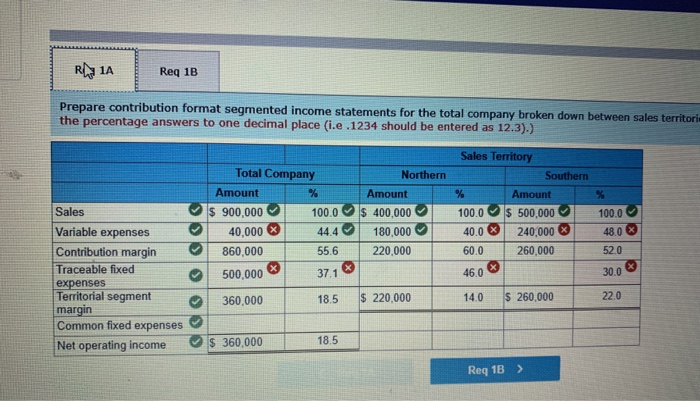

Vulcan Company's contribution format income statement for June is as follows: Vulcan Company Income Statement For the Month Ended June 30 Sales $980,000 Variable expenses 400,000 Contribution margin 500,000 Fixed expenses 450,000 Net operating income $ 50,000 Management is disappointed with the company's performance and is wondering what can be done to improve profits. By examining sales and cost records, you have determined the following: a. The company is divided into two sales territories-Northern and Southern The Northern Territory recorded $400,000 in sales and $180,000 in variable expenses during June; the remaining sales and variable expenses were recorded in the Southern Territory Fixed expenses of $200,000 and $115,000 are traceable to the Northern and Southern Territories, respectively. The rest of the fixed expenses are common to the two territories. b. The company is the exclusive distributor for two products-Paks and Tibs. Sales of Paks and Tibs totaled $170.000 and $230,000. respectively, in the Northern territory during June. Variable expenses are 22% of the selling price for Paks and 62% for Tibs. Cost records show that $71.400 of the Northern Territory's fixed expenses are traceable to Paks and $50.600 to Tibs, with the remainder common to the two products untuyua uisupURILLU W ILLUM PLURIUILLE ales and cost records, you have determined the following: wy LAUT 1. The company is divided into two sales territories-Northern and Southern. The Northern Territory recorded $400,000 in sales and $180,000 in variable expenses during June; the remaining sales and variable expenses were recorded in the Southern Territory. Fixed expenses of $200,000 and $115,000 are traceable to the Northern and Southern Territories, respectively. The rest of the forced expenses are common to the two territories. b. The company is the exclusive distributor for two products-Paks and Tibs. Sales of Paks and Tibs totaled $170,000 and $230,000. respectively, in the Northern Territory during June. Variable expenses are 22% of the selling price for Paks and 62% for Tibs. Cost records show that $71,400 of the Northern Territory's fixed expenses are traceable to Paks and $50,600 to Tibs, with the remainder common to the two products. Required: 1-a. Prepare contribution format segmented income statements for the total company broken down between sales territories 1-b. Prepare contribution format segmented income statements for the Northern Territory broken down by product line Answer is not complete. Complete this question by entering your answers in the tabs below. untuyua uisupURILLU W ILLUM PLURIUILLE ales and cost records, you have determined the following: wy LAUT 1. The company is divided into two sales territories-Northern and Southern. The Northern Territory recorded $400,000 in sales and $180,000 in variable expenses during June; the remaining sales and variable expenses were recorded in the Southern Territory. Fixed expenses of $200,000 and $115,000 are traceable to the Northern and Southern Territories, respectively. The rest of the forced expenses are common to the two territories. b. The company is the exclusive distributor for two products-Paks and Tibs. Sales of Paks and Tibs totaled $170,000 and $230,000. respectively, in the Northern Territory during June. Variable expenses are 22% of the selling price for Paks and 62% for Tibs. Cost records show that $71,400 of the Northern Territory's fixed expenses are traceable to Paks and $50,600 to Tibs, with the remainder common to the two products. Required: 1-a. Prepare contribution format segmented income statements for the total company broken down between sales territories 1-b. Prepare contribution format segmented income statements for the Northern Territory broken down by product line Answer is not complete. Complete this question by entering your answers in the tabs below. R1A Req 1B Prepare contribution format segmented income statements for the total company broken down between sales territori the percentage answers to one decimal place (i.e.1234 should be entered as 12.3).) Total Company Amount % $ 900,000 100,0 40,000 X 44.4 860,000 55. 6 500,000 37.1 360,000 18.5 Northern Amount $ 400,000 180,000 220,000 Sales Territory Southern % Amount 100.0 $ 500,000 40.0 240,000 60.0 260,000 100.0 48.0 52.0 46.0 % Sales Variable expenses Contribution margin Traceable fixed expenses Territorial segment margin Common fixed expenses Net operating income 30.0 % $ 220,000 14.0 $ 260,000 22.0 $ 360,000 Req 18 > Req 1B Req 1A Reg 1B Prepare contribution format segmented income statements for the Northern Territory broken down by product line. (Round the per answers to one decimal place (i.e .1234 should be entered as 12.3).) Product Line Amount $ 400,000 Northern Territory Amount $ 900,000 100,0 180 000 26 0 720,000 74.0 Amount $ 230,000 1000 1000 Sales 220 78.0 | 230,000 380 400,000 50.600 $ 349.400 78,0 Variable expenses Contribution margin Traceable fixed expenses Product line segment margin Common fixed expenses Sales territory segment margin 380 $ 230,000 74,0 720,000 $ 720,000 740