Answered step by step

Verified Expert Solution

Question

1 Approved Answer

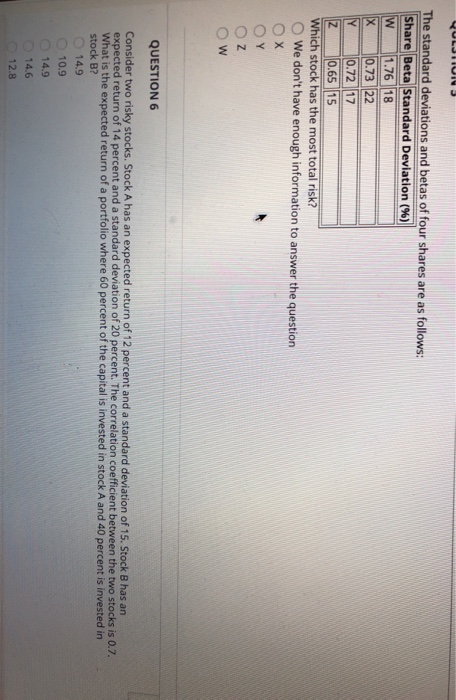

VULJTIUI 3 The standard deviations and betas of four shares are as follows: Share Beta Standard Deviation (%) w 1.76 18 X 0.73 22 Y

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cryptoassets The Innovative Investors Guide To Bitcoin And Beyond

Authors: Chris Burniske ,Jack Tatar

1st Edition

1260026671, 126002668X, 9781260026672, 9781260026689