Answered step by step

Verified Expert Solution

Question

1 Approved Answer

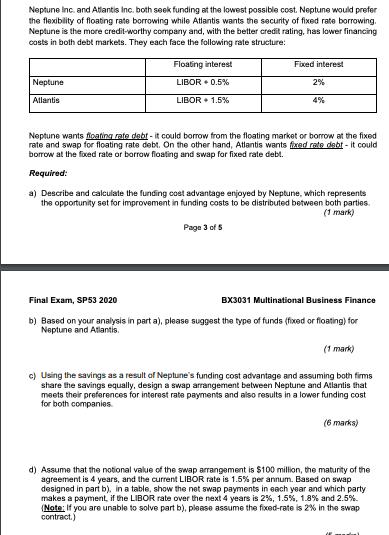

Neptune Inc. and Atlantis Inc. both seek funding at the lowest possible cost. Neptune would prefer the flexibility of floating rate borrowing while Atlantis

Neptune Inc. and Atlantis Inc. both seek funding at the lowest possible cost. Neptune would prefer the flexibility of floating rate borrowing while Atlantis wants the security of fixed rate borrowing. Neptune is the more credit-worthy company and, with the better credit rating, has lower financing costs in both debt markets. They each face the following rate structure: Neptune Atlantis Floating interest LIBOR +0.5% LIBOR + 1.5% Fixed interest 2% 4% Neptune wants floating rate debt - it could borrow from the floating market or borrow at the fixed rate and swap for floating rate debt. On the other hand, Atlantis wants fixed rate debt - it could borrow at the fixed rate or borrow floating and swap for fixed rate debt. Required: a) Describe and calculate the funding cost advantage enjoyed by Neptune, which represents the opportunity set for improvement in funding costs to be distributed between both parties. (1 mark) Page 3 of 5 Final Exam, SP53 2020 BX3031 Multinational Business Finance b) Based on your analysis in part a), please suggest the type of funds (fixed or floating) for Neptune and Atlantis. (1 mark) c) Using the savings as a result of Neptune's funding cost advantage and assuming both firms share the savings equally, design a swap arrangement between Neptune and Atlantis that meets their preferences for interest rate payments and also results in a lower funding cost for both companies. (6 marks) d) Assume that the notional value of the swap arrangement is $100 million, the maturity of the agreement is 4 years, and the current LIBOR rate is 1.5% per annum. Based on swap designed in part b), in a table, show the net swap payments in each year and which party makes a payment, if the LIBOR rate over the next 4 years is 2%, 1.5%, 1.8% and 2.5% (Note: If you are unable to solve part b), please assume the fixed-rate is 2% in the swap contract.)

Step by Step Solution

★★★★★

3.59 Rating (152 Votes )

There are 3 Steps involved in it

Step: 1

a The opportunity set for improvement in funding costs for Neptune would be the difference between t...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Multinational Business Finance

Authors: David K. Eiteman, Arthur I. Stonehill, Michael H. Moffett

14th edition

133879879, 978-0133879872