Answered step by step

Verified Expert Solution

Question

1 Approved Answer

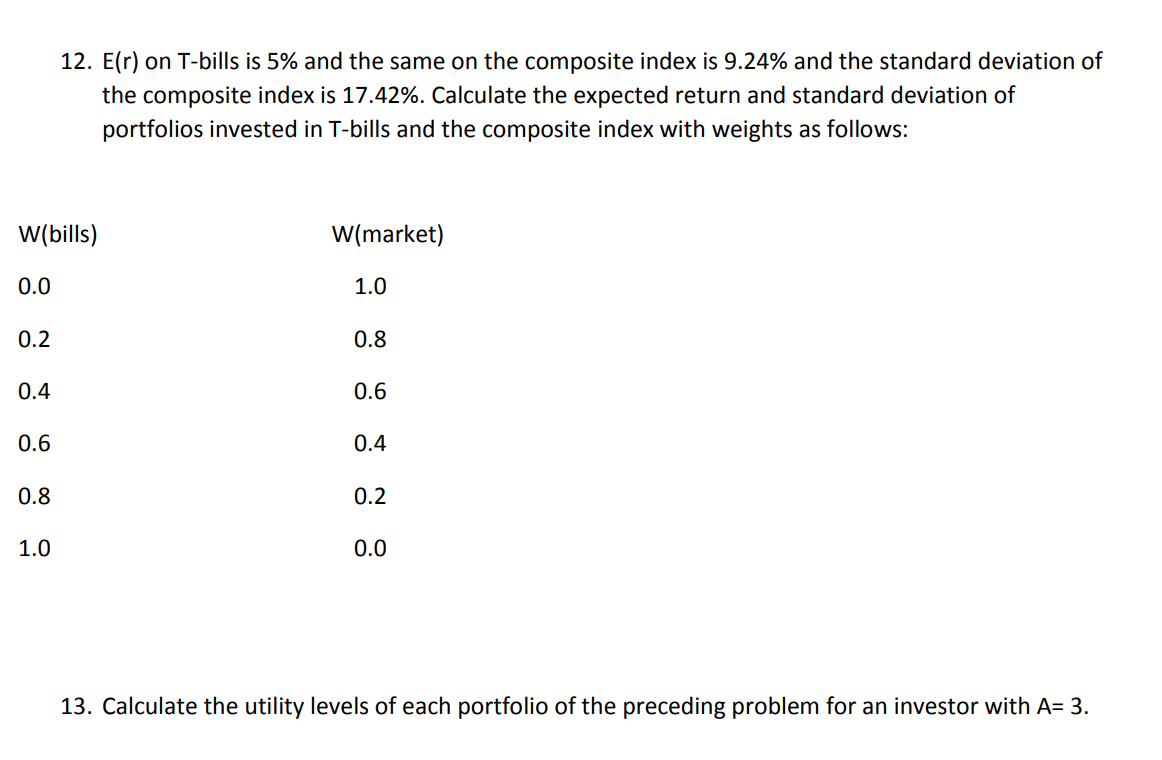

W(bills) 0.0 0.2 0.4 0.6 0.8 12. E(r) on T-bills is 5% and the same on the composite index is 9.24% and the standard

W(bills) 0.0 0.2 0.4 0.6 0.8 12. E(r) on T-bills is 5% and the same on the composite index is 9.24% and the standard deviation of the composite index is 17.42%. Calculate the expected return and standard deviation of portfolios invested in T-bills and the composite index with weights as follows: 1.0 W(market) 1.0 0.8 0.6 0.4 0.2 0.0 13. Calculate the utility levels of each portfolio of the preceding problem for an investor with A= 3.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To calculate the expected return and standard deviation of portfolios invested in Tbills and the composite index with different weights we can use the ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistics For Business And Financial Economics

Authors: Cheng Few Lee , John C Lee , Alice C Lee

3rd Edition

1461458978, 9781461458975