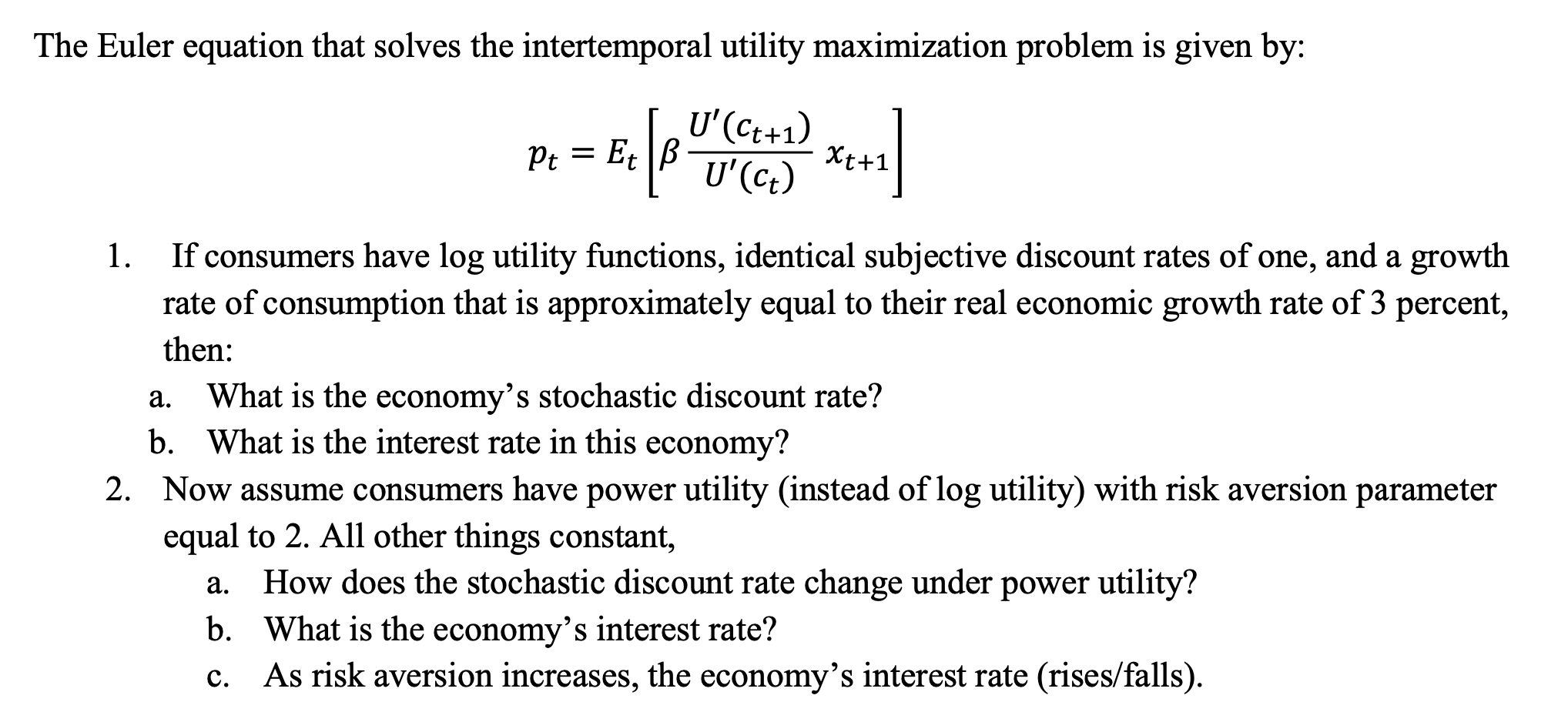

Question

We are given the Euler Equation Pt = Et[ (Beta*((U'(ct+1))/U'(ct))*xt+1]. and told growth rate of consumption is 3%, consumers have a log utility consumption what

We are given the Euler Equation

Pt = Et[ (Beta*((U'(ct+1))/U'(ct))*xt+1]. and told growth rate of consumption is 3%, consumers have a log utility consumption what is the stochastic discount rate? What is the interest rate in this economy?

The Euler equation that solves the intertemporal utility maximization problem is given by: 1. If consumers have log utility functions, identical subjective discount rates of one, and a growth rate of consumption that is approximately equal to their real economic growth rate of 3 percent, then: a. What is the economy's stochastic discount rate? b. What is the interest rate in this economy? 2. Now assume consumers have power utility (instead of log utility) with risk aversion parameter equal to 2. All other things constant, a. How does the stochastic discount rate change under power utility? b. What is the economy's interest rate? C. As risk aversion increases, the economy's interest rate (rises/falls). The Euler equation that solves the intertemporal utility maximization problem is given by: 1. If consumers have log utility functions, identical subjective discount rates of one, and a growth rate of consumption that is approximately equal to their real economic growth rate of 3 percent, then: a. What is the economy's stochastic discount rate? b. What is the interest rate in this economy? 2. Now assume consumers have power utility (instead of log utility) with risk aversion parameter equal to 2. All other things constant, a. How does the stochastic discount rate change under power utility? b. What is the economy's interest rate? C. As risk aversion increases, the economy's interest rate (rises/falls)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Futures And Other Derivatives

Authors: John C. Hull

9th Edition

0133456315, 9780133456318