Answered step by step

Verified Expert Solution

Question

1 Approved Answer

We assume no arbitrage hypothesis. We assume that the interest rate of the money market account is equal to r. We denote by C(t,St,T,K) (resp.

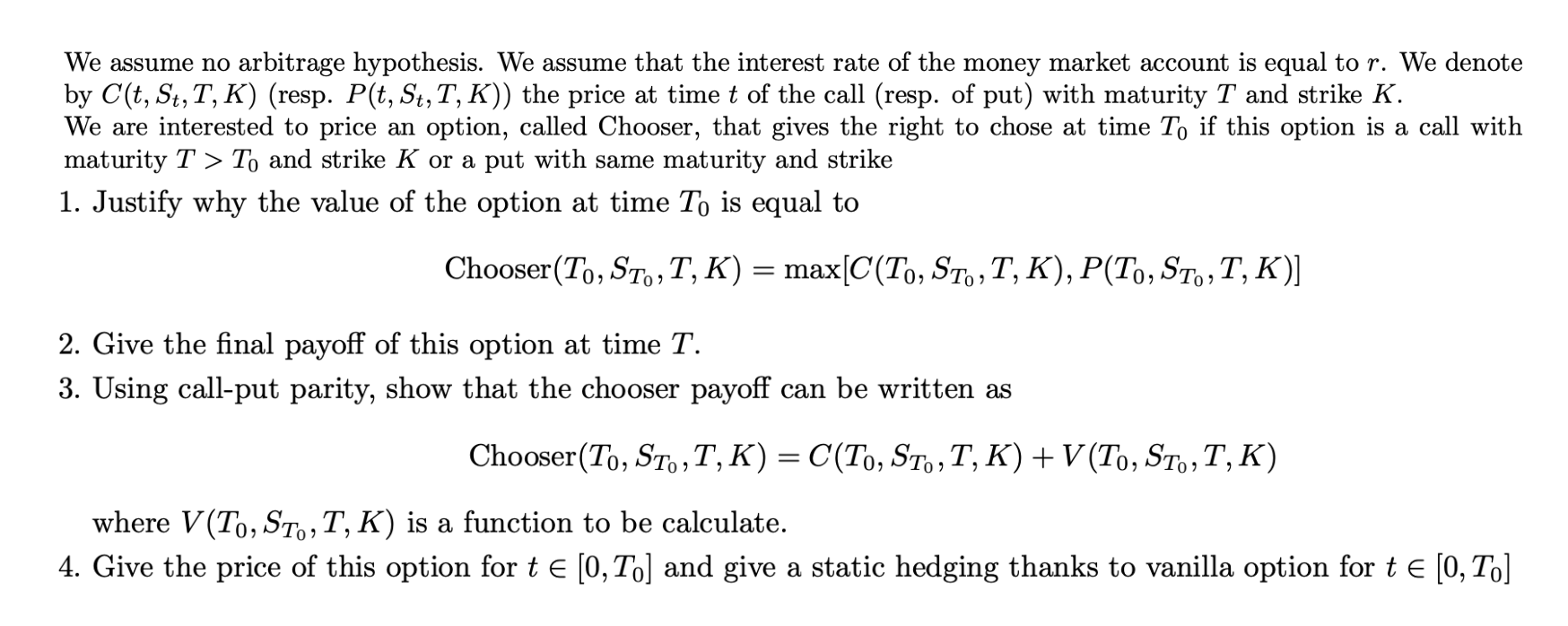

We assume no arbitrage hypothesis. We assume that the interest rate of the money market account is equal to r. We denote by C(t,St,T,K) (resp. P(t,St,T,K)) the price at time t of the call (resp. of put) with maturity T and strike K. We are interested to price an option, called Chooser, that gives the right to chose at time T0 if this option is a call with maturity T>T0 and strike K or a put with same maturity and strike 1. Justify why the value of the option at time T0 is equal to Chooser(T0,ST0,T,K)=max[C(T0,ST0,T,K),P(T0,ST0,T,K)] 2. Give the final payoff of this option at time T. 3. Using call-put parity, show that the chooser payoff can be written as Chooser(T0,ST0,T,K)=C(T0,ST0,T,K)+V(T0,ST0,T,K) where V(T0,ST0,T,K) is a function to be calculate. 4. Give the price of this option for t[0,T0] and give a static hedging thanks to vanilla option for t[0,T0]

We assume no arbitrage hypothesis. We assume that the interest rate of the money market account is equal to r. We denote by C(t,St,T,K) (resp. P(t,St,T,K)) the price at time t of the call (resp. of put) with maturity T and strike K. We are interested to price an option, called Chooser, that gives the right to chose at time T0 if this option is a call with maturity T>T0 and strike K or a put with same maturity and strike 1. Justify why the value of the option at time T0 is equal to Chooser(T0,ST0,T,K)=max[C(T0,ST0,T,K),P(T0,ST0,T,K)] 2. Give the final payoff of this option at time T. 3. Using call-put parity, show that the chooser payoff can be written as Chooser(T0,ST0,T,K)=C(T0,ST0,T,K)+V(T0,ST0,T,K) where V(T0,ST0,T,K) is a function to be calculate. 4. Give the price of this option for t[0,T0] and give a static hedging thanks to vanilla option for t[0,T0] Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started