Answered step by step

Verified Expert Solution

Question

1 Approved Answer

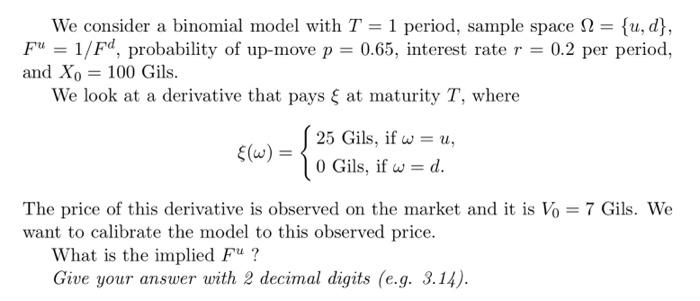

We consider a binomial model with T = 1 period, sample space = {u, d}, Fu = 1/Fd, probability of up-move p = 0.65, interest

We consider a binomial model with T = 1 period, sample space = {u, d}, Fu = 1/Fd, probability of up-move p = 0.65, interest rate r = 0.2 per period, and Xo = 100 Gils. We look at a derivative that pays at maturity T, where 25 Gils, if wu, = {(w) = 0 Gils, if w= d. The price of this derivative is observed on the market and it is Vo = 7 Gils. We want to calibrate the model to this observed price. What is the implied F" ? Give your answer with 2 decimal digits (e.g. 3.14). We consider a binomial model with T = 1 period, sample space = {u, d}, Fu = 1/Fd, probability of up-move p = 0.65, interest rate r = 0.2 per period, and Xo = 100 Gils. We look at a derivative that pays at maturity T, where 25 Gils, if wu, = {(w) = 0 Gils, if w= d. The price of this derivative is observed on the market and it is Vo = 7 Gils. We want to calibrate the model to this observed price. What is the implied F" ? Give your answer with 2 decimal digits (e.g. 3.14)

We consider a binomial model with T = 1 period, sample space = {u, d}, Fu = 1/Fd, probability of up-move p = 0.65, interest rate r = 0.2 per period, and Xo = 100 Gils. We look at a derivative that pays at maturity T, where 25 Gils, if wu, = {(w) = 0 Gils, if w= d. The price of this derivative is observed on the market and it is Vo = 7 Gils. We want to calibrate the model to this observed price. What is the implied F" ? Give your answer with 2 decimal digits (e.g. 3.14). We consider a binomial model with T = 1 period, sample space = {u, d}, Fu = 1/Fd, probability of up-move p = 0.65, interest rate r = 0.2 per period, and Xo = 100 Gils. We look at a derivative that pays at maturity T, where 25 Gils, if wu, = {(w) = 0 Gils, if w= d. The price of this derivative is observed on the market and it is Vo = 7 Gils. We want to calibrate the model to this observed price. What is the implied F" ? Give your answer with 2 decimal digits (e.g. 3.14)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Performance Measurement In Finance

Authors: John Knight, Stephen Satchell, Nathalie Farah

1st Edition

0750650265, 978-0750650267