Answered step by step

Verified Expert Solution

Question

1 Approved Answer

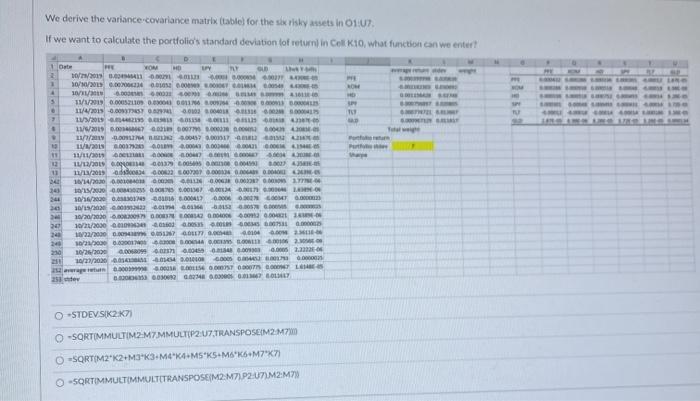

We derive the variance covariance matrix table for the six risky assets in 01:07 If we want to calculate the portfolio's standard deviation for return

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Public Relations Handbook

Authors: Alison Theaker

6th Edition

0367278901,1000208834