Answered step by step

Verified Expert Solution

Question

1 Approved Answer

We form a portfolio using Johnson & Johnson (NYSE:JNJ), Pfizer (NYSE:PFE), and the risk-free asset. The weights are 0.5,0.4, and 0.1 respectively. Expected returns are

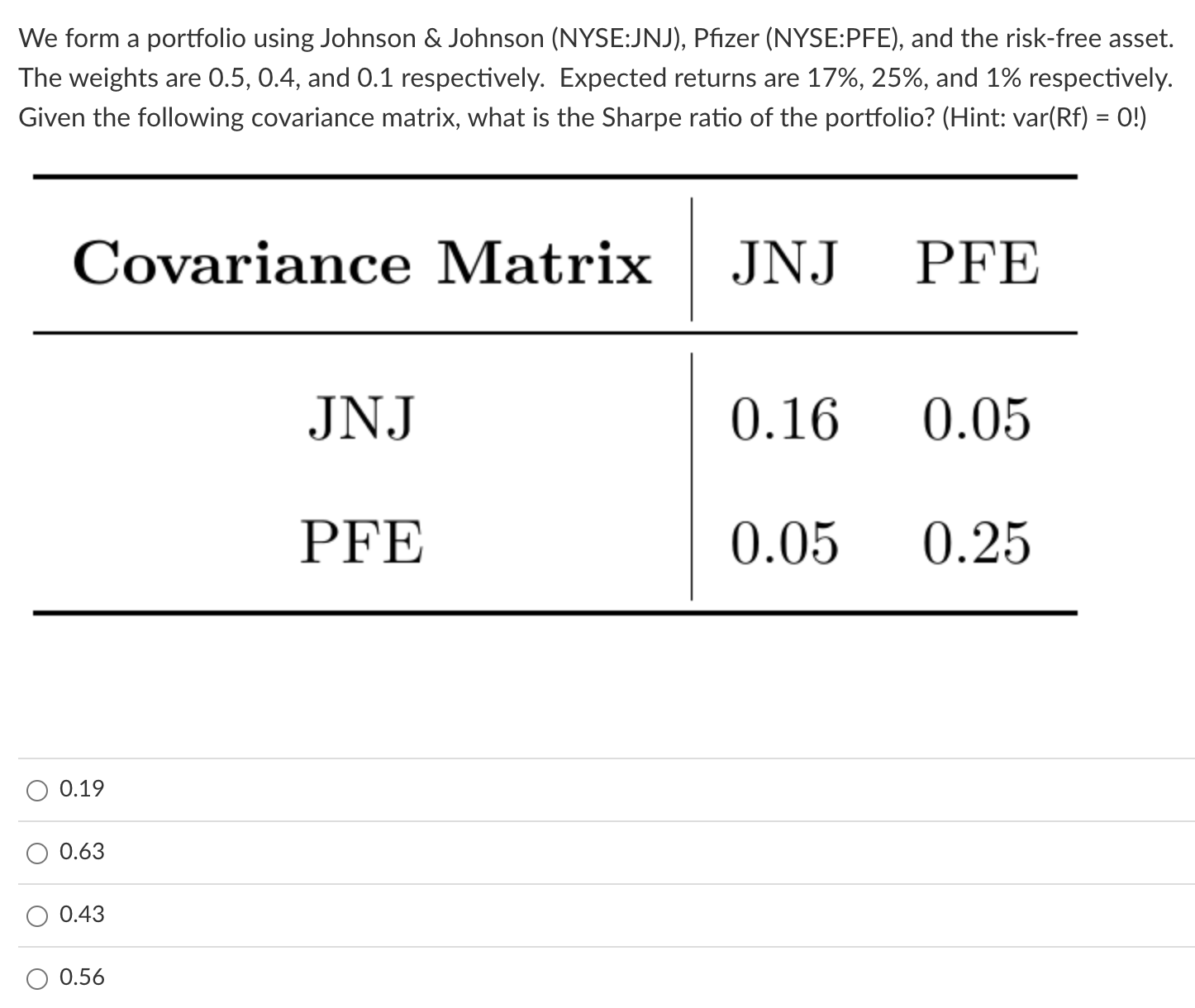

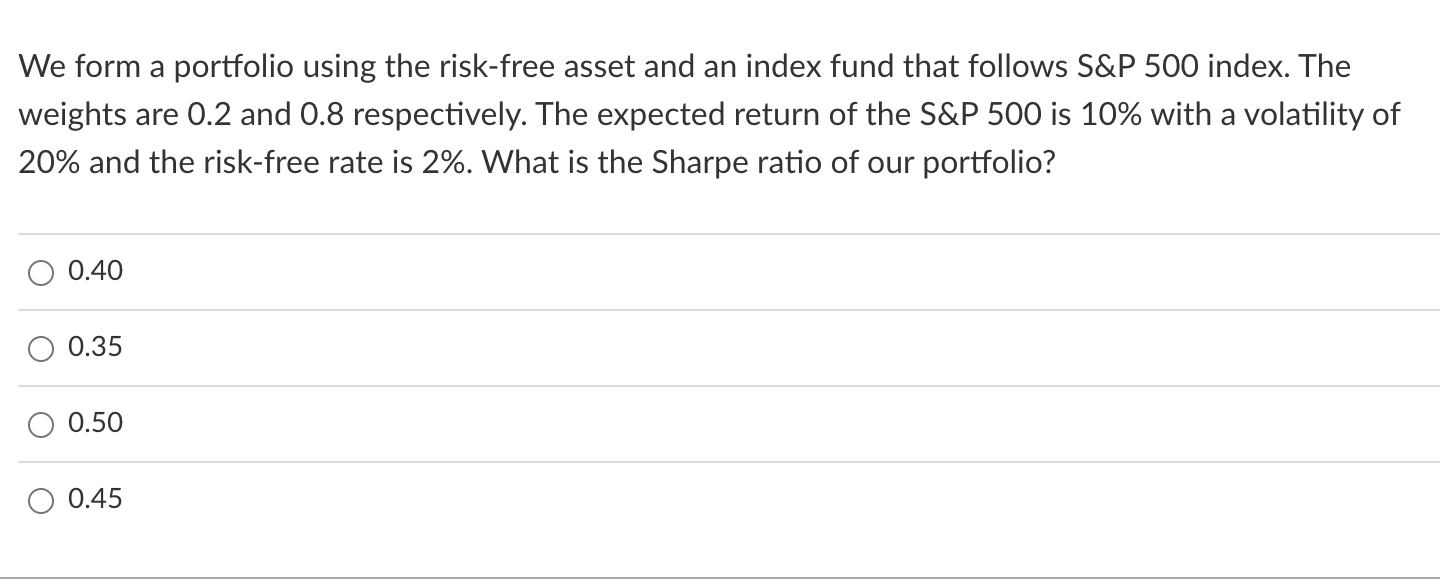

We form a portfolio using Johnson \& Johnson (NYSE:JNJ), Pfizer (NYSE:PFE), and the risk-free asset. The weights are 0.5,0.4, and 0.1 respectively. Expected returns are 17%,25%, and 1% respectively. Given the following covariance matrix, what is the Sharpe ratio of the portfolio? (Hint: var(Rf)=0 !) 0.19 0.63 0.43 0.56 We form a portfolio using the risk-free asset and an index fund that follows S\&P 500 index. The weights are 0.2 and 0.8 respectively. The expected return of the S\&P 500 is 10% with a volatility of 20% and the risk-free rate is 2%. What is the Sharpe ratio of our portfolio? \begin{tabular}{l} 0.40 \\ 0.35 \\ \hline 0.50 \\ 0.45 \end{tabular}

We form a portfolio using Johnson \& Johnson (NYSE:JNJ), Pfizer (NYSE:PFE), and the risk-free asset. The weights are 0.5,0.4, and 0.1 respectively. Expected returns are 17%,25%, and 1% respectively. Given the following covariance matrix, what is the Sharpe ratio of the portfolio? (Hint: var(Rf)=0 !) 0.19 0.63 0.43 0.56 We form a portfolio using the risk-free asset and an index fund that follows S\&P 500 index. The weights are 0.2 and 0.8 respectively. The expected return of the S\&P 500 is 10% with a volatility of 20% and the risk-free rate is 2%. What is the Sharpe ratio of our portfolio? \begin{tabular}{l} 0.40 \\ 0.35 \\ \hline 0.50 \\ 0.45 \end{tabular} Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Problems In Portfolio Theory And The Fundamentals Of Financial Decision Making

Authors: Leonard C Maclean, William T Ziemba

1st Edition

9814749931, 978-9814749930