Answered step by step

Verified Expert Solution

Question

1 Approved Answer

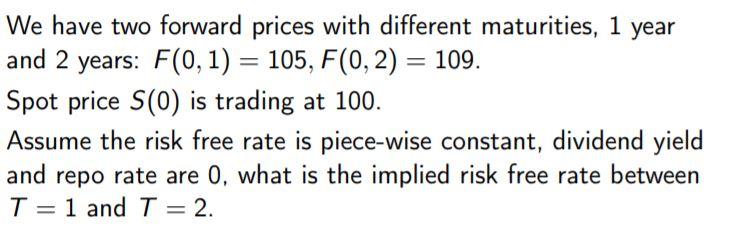

We have two forward prices with different maturities, 1 year and 2 years: F(0, 1) = 105, F(0, 2) = 109. Spot price S(0) is

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance

Authors: Charles Francis Bastable

1st Edition

1375520083, 978-1375520089