Question: We need to Evaluate pension accounting (defined benefit plans) and add and correct the incorrect treatment of it with the adjustments, calculations and the specific

We need to Evaluate pension accounting (defined benefit plans) and add and correct the incorrect treatment of it with the adjustments, calculations and the specific FASB rules that apply.

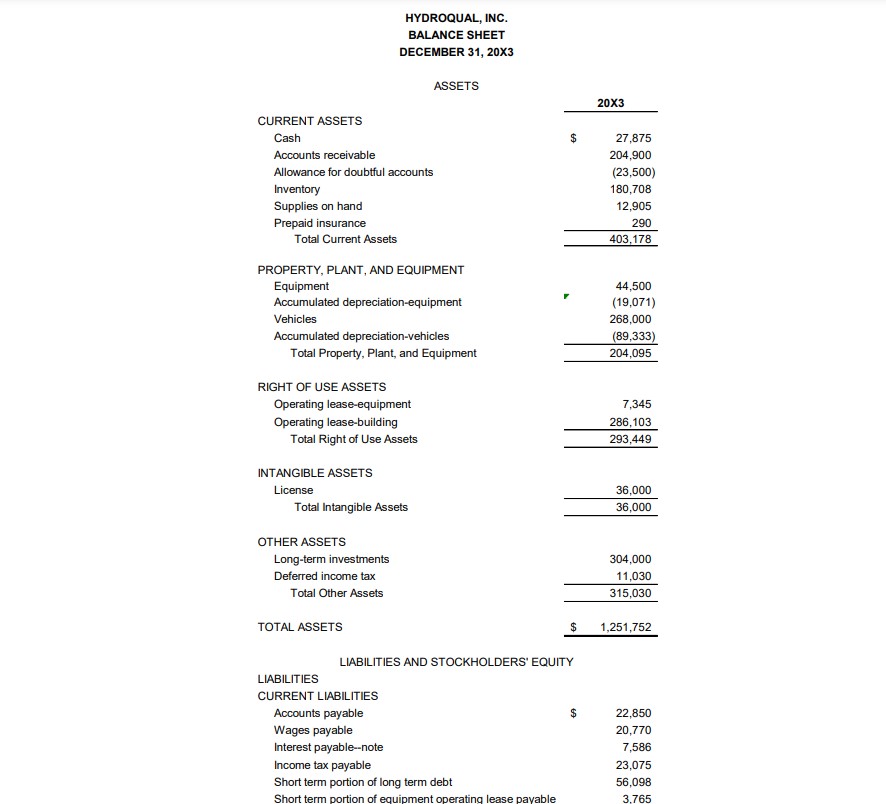

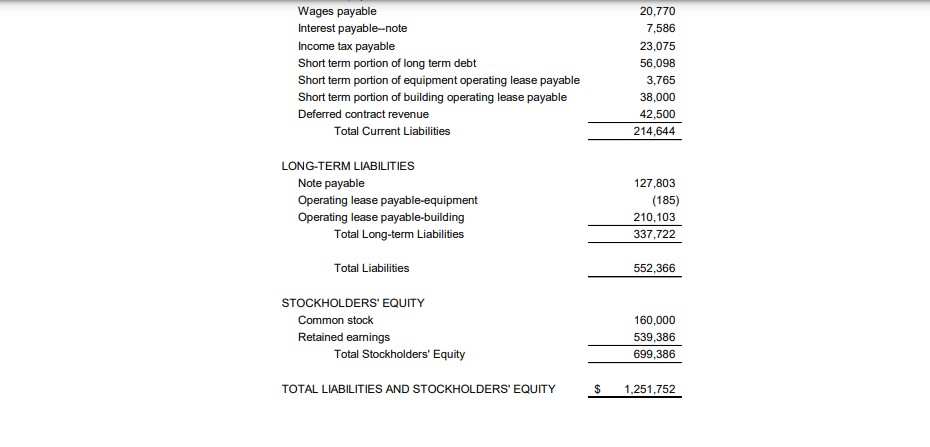

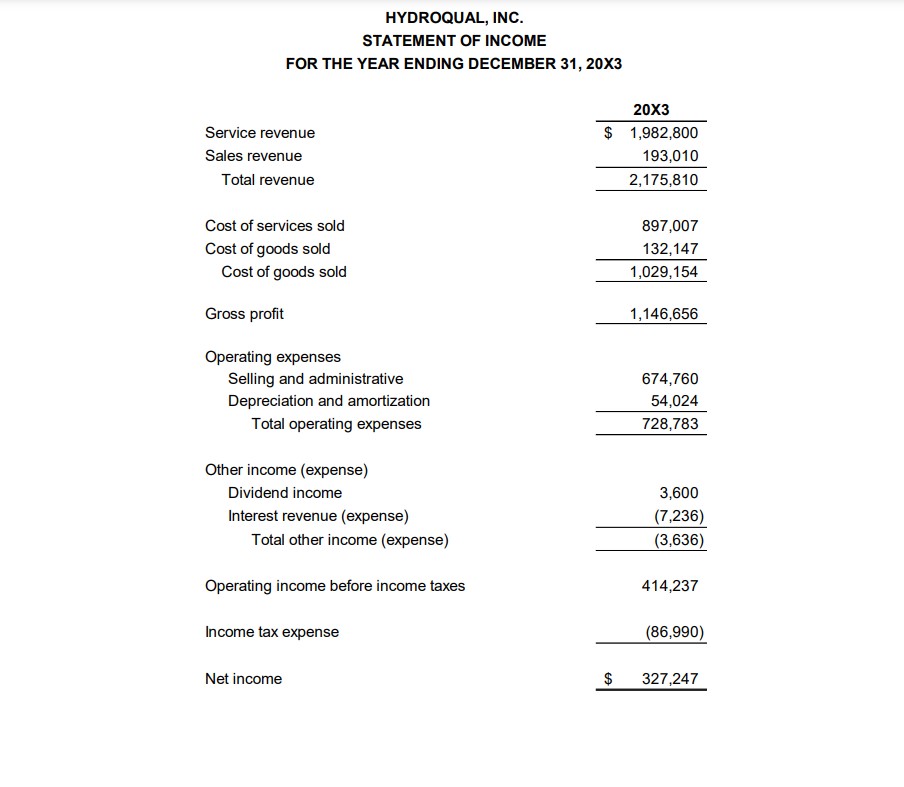

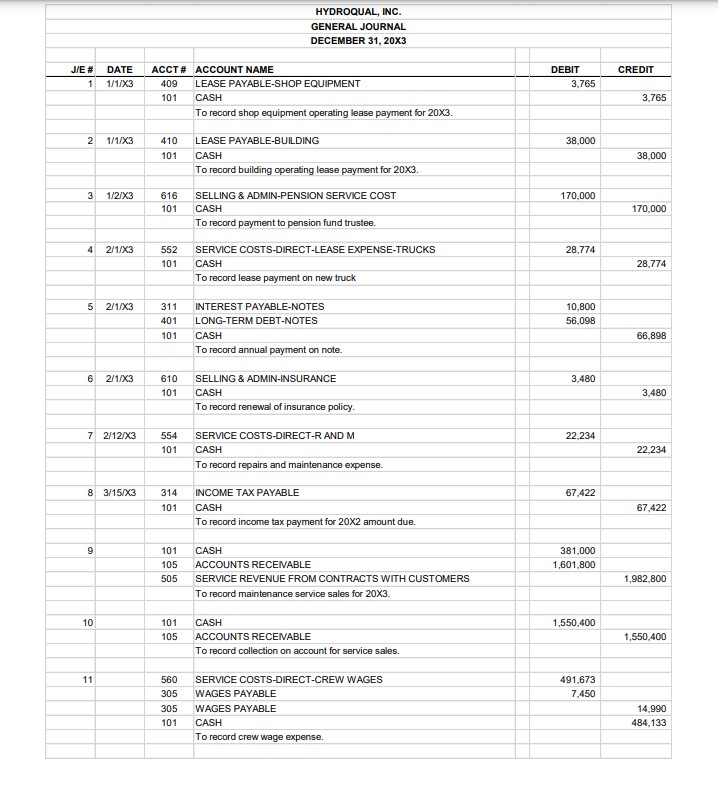

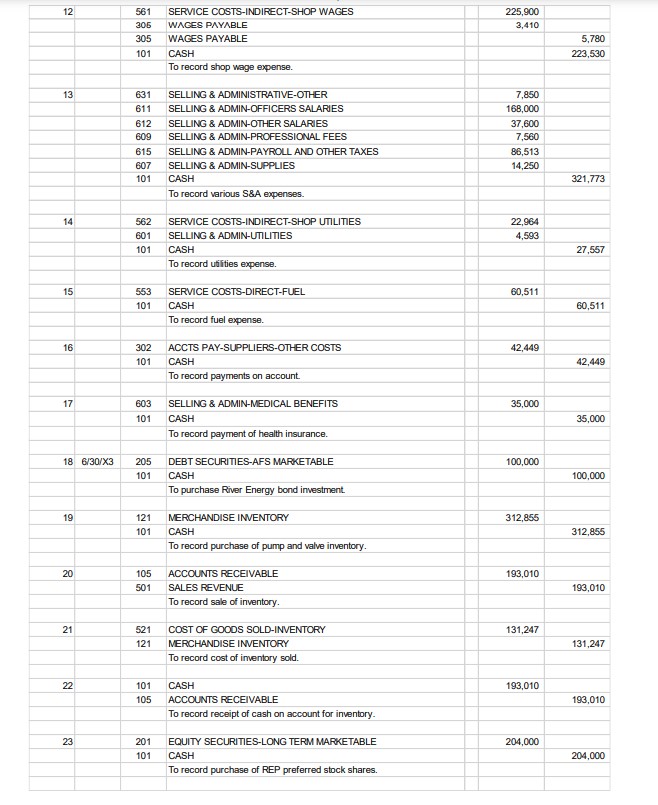

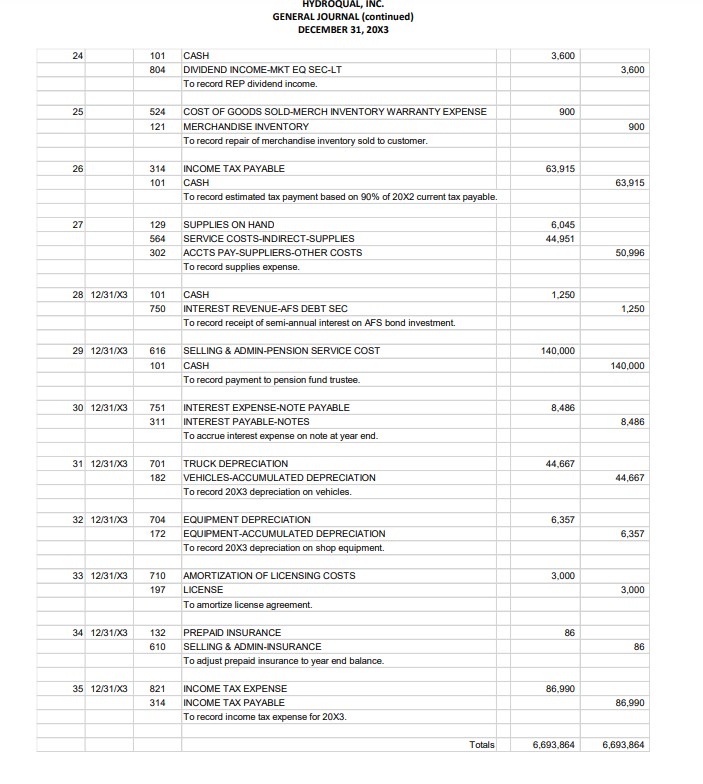

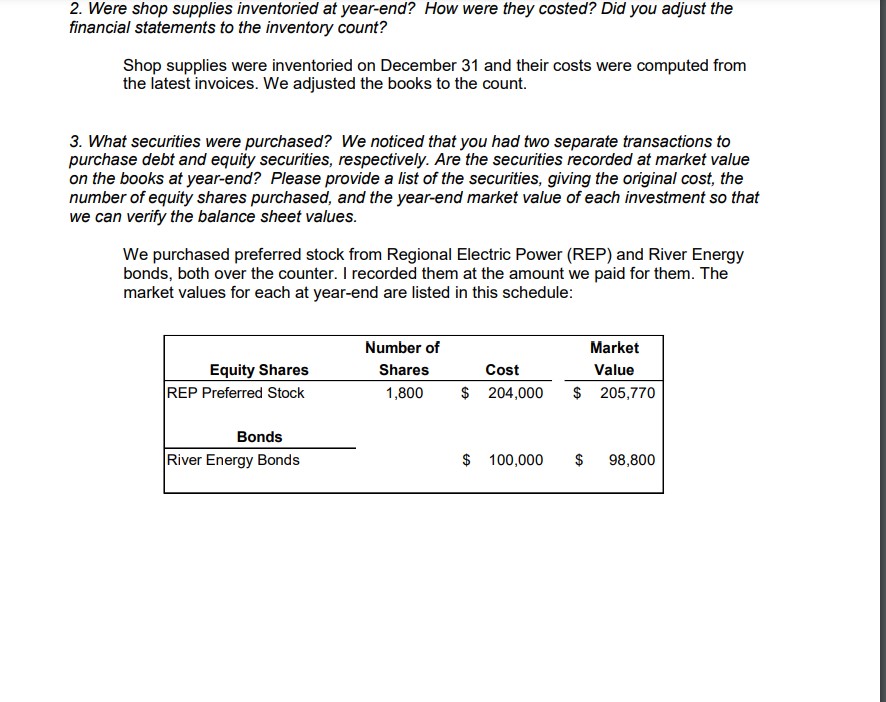

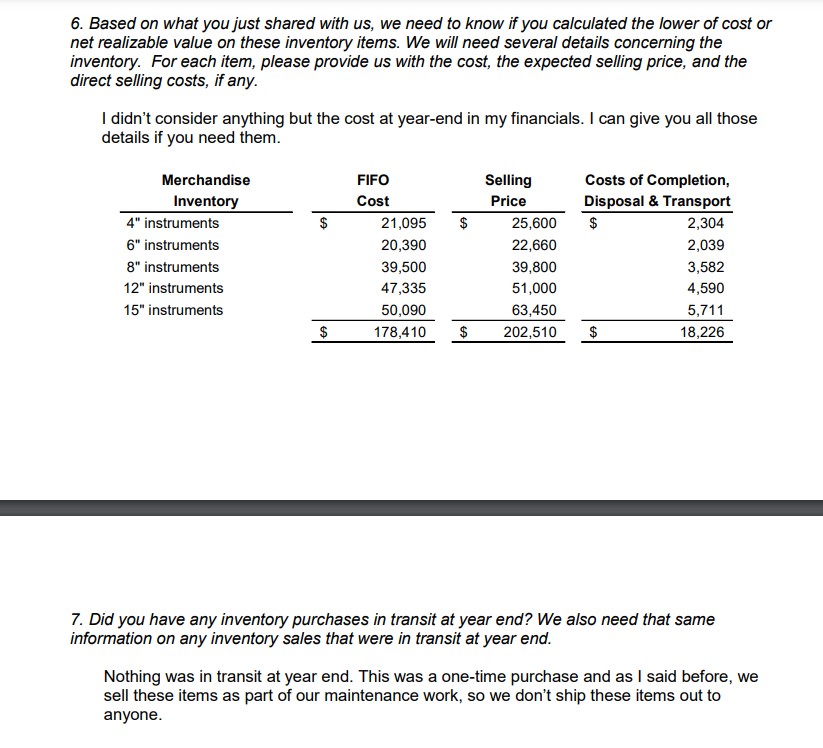

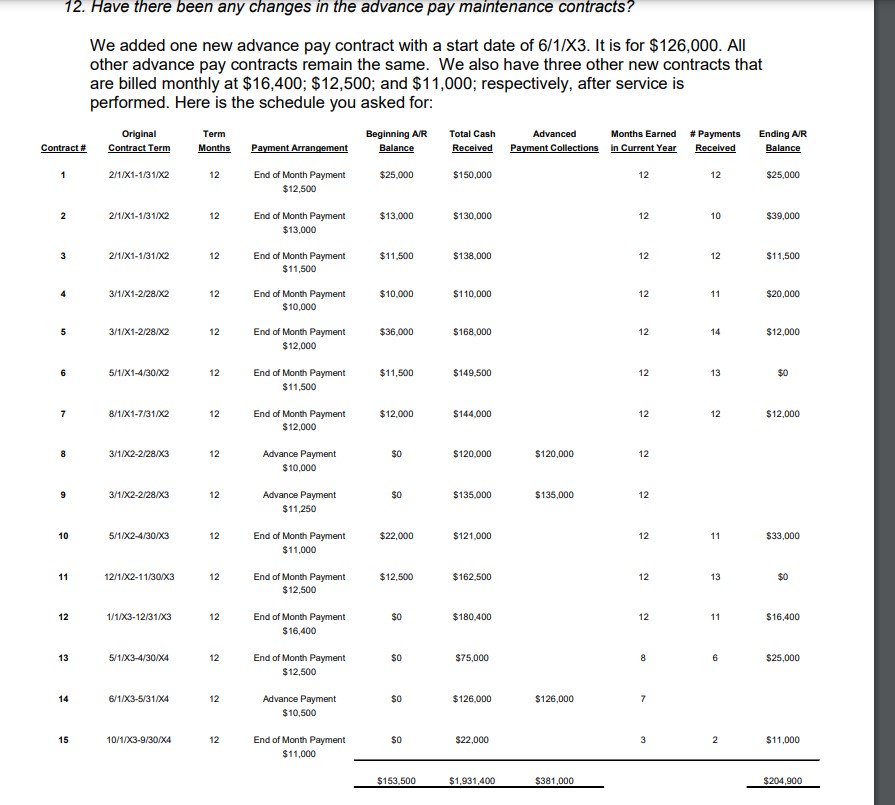

HYDROQUAL, INC. Preliminary Financials 20x3 During the rst week of January 20x4, Torn Fasbee called you to his ofce and asked if you would be willing to review HydroQual's nancial statements one more time. The company had decided to offer a benets package (medical insurance and pension) to try to keep its good employees. You remember there was some discussion of these matters during last year's engagement. Additionally, the company was finding it necessary to replace pumps, valves, and other equipment when performing maintenance. Initially, HydroQual simply arranged for the customer to purchase repair parts, and HydroQual then would install them. However, in late August, Rick and Kay decided that the company should carry its own equipment inventory. They both felt condent that their market would eventually extend beyond their current maintenance customers so they went ahead with the purchase of computerized pressure-monitoring pumps and valves inventory. Since these instruments are not bulky, they can be stored in the current shop space. They felt this line of parts would best meet their customer needs in terms of price and quality. In addition, they are offering to make good on any problems encountered by their customers on these items. Although not a large client, you liked the people at HydroQual and readily agreed to the assignment. Tom handed you the draft 20x3 nancial statements that Jerry Loos had prepared and sent over. Jerry was expecting some questions from you tomorrow morning (Thursday), and indicated that he would have his responses ready for you the next day. You decided to consult with Martha Mason about the tax consequences of the pension plan. Martha was fairly certain that the plan and its funding were approved by ERISA. Thus, its benefits were insured and any expense computed was fully deductible for tax purposes. She also told you that you should be aware that any cash contributions in excess of the pension expense for the current year are not deductible according to the Internal Revenue Code Sec. 404(a)(1)(A)(ii). Additionally, Martha recalled that management planned to allocate prior service costs over the next 10 years beginning in 20x3. In addition, during your preliminaLy analytical costs over the next 10 years beginning in 20x3. In addition, during your preliminary analytical review of HydroQual's general journal, you noticed two new investments in marketable equity and debt securities. You asked Martha whether an unrealized gain was taxable. She assured you that such gains would not be taxable until the securities were sold. REQUIRED: The journal entries and nancial statements prepared by Jerry Loos are attached. Review these data and prepare a list of additional information needed from Jerry. Be as specic as possible and phrase your requests in the form of questions as they normally would be asked of a client. You should also be prepared to explain your reasons for asking specific questions. As you determine the data needed, be aware that once again, Jerry has asked you to prepare the statement of cash flows, statement of changes in stockholders' equity, nancial statement notes, and earnings per share disclosures. He also reminded you that the bank wants comparative statements and requires the fair value of all nancial instruments and information on major customers be disclosed. HYDROQUAL, INC. BALANCE SHEET DECEMBER 31, 20X3 ASSETS 20X3 CURRENT ASSETS Cash $ 27,875 Accounts receivable 204,900 Allowance for doubtful accounts (23,500) Inventory 180,708 Supplies on hand 12.905 Prepaid insurance 290 Total Current Assets 403,178 PROPERTY, PLANT, AND EQUIPMENT Equipment 44,500 Accumulated depreciation-equipment (19,071) Vehicles 268,000 Accumulated depreciation-vehicles (89,333) Total Property, Plant, and Equipment 204.095 RIGHT OF USE ASSETS Operating lease-equipment 7,345 Operating lease-building 286,103 Total Right of Use Assets 293,449 INTANGIBLE ASSETS License 36.000 Total Intangible Assets 36.000 OTHER ASSETS Long-term investments 304,000 Deferred income tax 11,030 Total Other Assets 315,030 TOTAL ASSETS $ 1,251,752 LIABILITIES AND STOCKHOLDERS' EQUITY LIABILITIES CURRENT LIABILITIES Accounts payable $ 22,850 Wages payable 20,770 Interest payable--note 7,586 Income tax payable 23,075 Short term portion of long term debt 56,098 Shor 3.765Wages payable 20,770 Interest payable--note 7,586 Income tax payable 23,075 Short term portion of long term debt 56,098 Short term portion of equipment operating lease payable 3,765 Short term portion of building operating lease payable 38,000 Deferred contract revenue 42,500 Total Current Liabilities 214,644 LONG-TERM LIABILITIES Note payable 127,803 Operating lease payable-equipment (185) Operating lease payable-building 210,103 Total Long-term Liabilities 337,722 Total Liabilities 552,366 STOCKHOLDERS' EQUITY Common stock 160,000 Retained earnings 539,386 Total Stockholders' Equity 699,386 TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY $ 1,251,752HYDROQUAL, INC. STATEMENT OF INCOME FOR THE YEAR ENDING DECEMBER 31, 20X3 20X3 Service revenue $ 1,982,800 Sales revenue 193,010 Total revenue 2, 175,810 Cost of services sold 897,007 Cost of goods sold 132,147 Cost of goods sold 1,029,154 Gross profit 1,146,656 Operating expenses Selling and administrative 674,760 Depreciation and amortization 54,024 Total operating expenses 728,783 Other income (expense) Dividend income 3,600 Interest revenue (expense) (7,236) Total other income (expense) (3,636) Operating income before income taxes 414,237 Income tax expense (86,990) Net income $ 327,247HYDROQUAL, INC. GENERAL JOURNAL DECEMBER 31, 20X3 WE # DATE ACCT # ACCOUNT NAME DEBIT CREDIT 1/1/X3 409 LEASE PAYABLE-SHOP EQUIPMENT 3,765 101 CASH 3,765 To record shop equipment operating lease payment for 20X3. 2 1/1/X3 410 LEASE PAYABLE-BUILDING 38,000 101 CASH 38.000 To record building operating lease payment for 20X3. 3 1/2/X3 616 SELLING & ADMIN-PENSION SERVICE COST 170,000 101 CASH 170,000 To record payment to pension fund trustee. 4 2/1/X3 552 SERVICE COSTS-DIRECT-LEASE EXPENSE-TRUCKS 28,774 101 CASH 28,774 To record lease payment on new truck 5 2/1/X3 311 INTEREST PAYABLE-NOTES 10 800 401 LONG-TERM DEBT-NOTES 56,098 101 CASH 86.898 To record annual payment on note. 6 2/1/X3 610 SELLING & ADMIN-INSURANCE 3.480 101 CASH 3.480 To record renewal of insurance policy. 7 2/12/X3 554 SERVICE COSTS-DIRECT-R AND M 22,234 101 CASH 22,234 To record repairs and maintenance expense. 8 3/15/X3 314 INCOME TAX 67,422 101 CASH 67.422 To record income tax payment for 20X2 amount due. 9 101 CASH 381.000 105 ACCOUNTS RECEM 1,601,800 505 SERVICE REVENUE FROM CONTRACTS WITH CUSTOMERS 1,982,800 To record maintenance service sales for 20X3. 10 101 CASH 1,550,400 105 ACCOUNTS RECEIVABLE 1,550,400 To record collection on account for service sales. 11 560 SERVICE COSTS-DIRECT-CREW WAGES 491,673 305 WAGES PAYABLE 7,450 305 WAGES PAYABLE 14,990 101 CASH 484,133 To record crew wage expense.12 561 SERVICE COSTS-INDIRECT-SHOP WAGES 225,900 306 WAGES PAYABLE 3,410 305 WAGES PAYABLE 5,780 101 CASH 223,530 To record shop wage expense. 13 631 SELLING & ADMINISTRATIVE-OTHER 7,850 611 SELLING & ADMIN-OFFICERS SALARIES 168,000 612 SELLING & ADMIN-OTHER SALARIES 37,600 609 SELLING & ADMIN-PROFESSIONAL FEES 7,560 615 SELLING & ADMIN-PAYROLL AND OTHER TAXES 86,513 607 SELLING & ADMIN-SUPPLIES 14,250 101 CASH 321,773 To record various S&A expenses. 14 562 SERVICE COSTS-INDIRECT-SHOP UTILITIES 22,964 601 SELLING & ADMIN-UTILITIES 4,593 101 CASH 27,557 To record utilities expense. 15 553 SERVICE COSTS-DIRECT-FUEL 60,511 101 CASH 60,511 To record fuel expense. 16 302 ACCTS PAY-SUPPLIERS-OTHER COSTS 42,449 101 CASH 42,449 To record payments on account 17 603 SELLING & ADMIN-MEDICAL BENEFITS 35,000 101 CASH 35,000 To record payment of health insurance. 18 6/30/X3 205 DEBT SECURITIES-AFS MARKETABLE 100,000 101 CASH 100,000 To purchase River Energy bond investment 19 121 MERCHANDISE INVENTORY 312,855 101 CASH 312,855 To record purchase of pump and valve inventory 20 105 ACCOUNTS RECEIVABLE 193,010 501 SALES REVENUE 193,010 To record sale of inventory. 21 521 COST OF GOODS SOLD-INVENTORY 131,247 121 MERCHANDISE INVENTORY 131,247 To record cost of inventory sold. 22 101 CASH 193,010 105 ACCOUNTS RECEIVABLE 193,010 To record receipt of cash on account for inventory. 23 201 EQUITY SECURITIES-LONG TERM MARKETABLE 204,000 101 CASH 204,000 To record purchase of REP preferred stock shares.GENERAL JOURNAL (continued) DECEMBER 31, 20X3 24 101 CASH 3.600 804 DIVIDEND INCOME-MKT EQ SEC-LT 3,600 To record REP dividend income 24 524 COST OF GOODS SOLD-MERCH INVENTORY WARRANTY EXPENSE 900 121 MERCHANDISE INVENTORY 900 To record repair of merchandise inventory sold to customer. 20 314 INCOME TAX PAYABLE 63.915 101 CASH 63,915 To record estimated tax payment based on 90% of 20X2 current tax payable. 27 129 SUPPLIES ON HAND 6,045 564 SERVICE COSTS-INDIRECT-SUPPLIES 44,951 302 ACCTS PAY-SUPPLIERS-OTHER COSTS 50.996 To record supplies expense 28 12/31/X3 101 CASH 1.250 750 INTEREST REVENUE-AFS DEBT SEC 1,250 To record receipt of semi-annual interest on AFS bond investment. 29 12/31/X3 616 SELLING & ADMIN-PENSION SERVICE COST 140,000 101 CASH 140,000 To record payment to pension fund trustee. 30 12/3103 751 INTEREST EXPENSE-NOTE PAYABLE 8.486 311 INTEREST PAYABLE-NOTES 8.486 To accrue interest expense on note at year end. 31 12/31/X3 701 TRUCK DEPRECIATION 44.667 182 VEHICLES-ACCUMULATED DEPRECIATION 44.667 To record 20X3 depreciation on vehicles. 32 12/31/X3 704 EQUIPMENT DEPRECIATION 6,357 172 EQUIPMENT-ACCUMULATED DEPRECIATION 6.357 To record 20X3 depreciation on shop equipment. 33 123103 710 AMORTIZATION OF LICENSING COSTS 3,000 197 LICENSE 3.000 To amortize license agreement. 34 12/31/X3 132 PREPAID INSURANCE 86 610 SELLING & ADMIN-INSURANCE 86 To adjust prepaid insurance to year end balance. 35 12/31/X3 821 INCOME TAX EXPENSE 86.990 314 INCOME TAX PAYABLE 86,990 To record income tax expense for 20X3. Totals 6,693,864 6,693,864HYDROQUAL, INC. Questions for Bookkeeper 20x3 Jerry Loos called Friday afternoon to tell you that he had completed his responses to your questions. Bright and early on Monday morning, you Showed up at HydroQual. Once again, you began satisfying yourself as to whether the financial statements were prepared in accordance with GAAP. Incidentally, Jerry confirmed that the pension plan had been approved by the Department of labor and was covered by ERISA. During your examination of HydroQual's financial records, certain additional information came to your attention. 1. Fcr tax purposes, HydroQuaI is entitled to a dividend received deduction of 50 percent on the equity securities they own. This is treated as a permanent tax difference according to Martha Mason. The actual return on pension assets equaled the estimated return. On Tom Fasbee's advice, and after conversations with the Bank, the Company has chosen to provide pension benet disclosures required for public entities. Martha also told you that pension expense for nancial reporting is fully deductible for tax purposes. Cash paid in excess (prepaid pension expense) of the current year expense is not deductible, and the liability recognized on the balance sheet is not recognized for tax purposes. The unamortized prior service cost held in accumulated other comprehensive income results in a deferred tax benefit, which offsets any deferred tax asset resulting from differing tax treatments for reporting and tax purposes. For tax purposes. the "addition" to crew trucks is treated as a new investment in 20X3. The MACR's percentages are to be applied to this addition as would be to any new piece of equipment starting in 20X3. The nance lease concept is not recognized for tax purp0ses. For tax purposes, finance leases are treated as if they were short-term leases, with any prepaid amount treated as an asset. As with operating leases, the tax law does not recognize liabilities connected with nance leases. The IRS recognizes investments in equity and debt securities at cost, with no consideration for unrealized gains and losses. 6. The IRS recognizes warranty costs only as they are incurred. 7. Jerry informed you that he had learned that the current market interest rate for a note similar to the Company's outstanding note on the trucks had decreased to 4.25% early last year. REQUIRED: Your questions and Jerry's responses are summarized below. Using this information, prepare all necessary adjusting and correcting journal entries for HydroQual's year ending 20X3. All corrections must be supported by thoughtful analyses, complete with calculations and/or authoritative sources. The FASB Accounting Standards Codification (ASC) should be the primary authoritative source used. YOUR QUESTIONS AND CLIENT RESPONSES 1. Do you anticipate any significant collection problems? Is an increase in the allowance required at year-end? Did you collect the late payments from the contracts in question last year? We did a calculation and determined that the allowance to accounts receivable ratio decreased by about 25% percent, so we are thinking that the allowance may be too low. We collected the late payments from last year in full. Currently, we have two late amounts of $10,000 and $12,500, both "in the mail" I am told. Two other monthly contracts are two months behind, and one is one month behind for a total of $60,500. Of course, if you consider the December payments as being late, which they are not, yet, the total owed on these latter three contracts would be $97,000. We don't think that more than one of these accounts will be a problem. I talked to Rick about these accounts and we recommend a total allowance of no more than half of the $60,500 amount. Since we collected all the late payments last year, we are not that concerned about these late accounts either. Also, none of our new inventory sales accounts are late-those customers pay quickly.2. Were shop supplies inventoried at year-end? How were they costed? Did you adjust the financial statements to the inventory count? Shop supplies were inventoried on December 31 and their costs were computed from the latest invoices. We adjusted the books to the count. 3. What securities were purchased? We noticed that you had two separate transactions to purchase debt and equity securities, respectively. Are the securities recorded at market value on the books at year-end? Please provide a list of the securities, giving the original cost, the number of equity shares purchased, and the year-end market value of each investment so that we can verify the balance sheet values. We purchased preferred stock from Regional Electric Power (REP) and River Energy bonds, both over the counter. I recorded them at the amount we paid for them. The market values for each at year-end are listed in this schedule: Number of Market Equity Shares Shares Cost Value REP Preferred Stock 1,800 $ 204,000 $ 205,770 Bonds River Energy Bonds $ 100,000 $ 98,8004. What is your intent in hoiding these securities? Did you invest in them because interest rates are so low on savings accounts these days? How long do you expect to own them? The investment in the preferred shares was Kay's idea. It was actually a great idea since we received dividends and the market price also increased. She plans to hold on to these shares and gures that it is a relatively safe place to park some cash that could be used for expansion sometime in the future. We are pretty excited about the effect these shares had on our bottom line this rst year. We could always sell them if we need the cash. but we do not intend to sell them any time soon, especially if they keep performing the way they did this year. The bonds provided us with a nice interest payment at year end, but they lost value in the market. We plan to hold the bonds for at least a few years and hope they will also increase in value. allowing us to reap a gain later on down the road. Until then, you are correct in assuming the idea is to earn quite a bit more cash than any bank account would yield. 5. We noticed that you are now carrying a iine of inventory and setting these items in addition to performing maintenance. Did you do a count and cost the new pump and valve inventory from the latest invoices at year end? Do you use a periodic or a perpetual inventory system for these items? Yes. we counted all items at year end and used the latest invoices. We are using a perpetual inventory system. You know, these are highly technical products. Like other such products. prices are volatile and sometimes take a nosedive. A couple of the instrument categories did this year, and we got caughtif we had just waited. which, by the way, I suggested we do, we could have bought them at a lower price. This purchase did not turn out nearly as well as the REP investment. I guess when you need inventory though, you need it now. 6. Based on what you just shared with us, we need to know it' you calculated the lower of cost or net realizable value on these inventory items. We will need several details concerning the inventory. For each item, please provide us with the cost, the expected selling price, and the direct selling costs, if any. I didn't consider anything but the cost at year-end in my financials. I can give you all those details if you need them. Merchandise FIFO Selling Costs of Completion. InventoryI Cost Price Disposal 8. Transport 4" instruments $ 21,095 $ 25,500 $ 2,304 6" instruments 20,390 22,560 2,039 8" instruments 39,500 39,800 3,582 12" instruments 4?,335 51,000 4,590 15' instruments 50,090 63,450 5,711 $ 178,410 $ 202,510 $ 18,225 7. Did you have any inventory purchases in transit at year end? We also need that same information on any inventory sales that were in transit at year end. Nothing was in transit at year end. This was a one-time purchase and as I said before. we sell these items as part of our maintenance work, so we don't ship these items out to anyone. 8. We noticed that you booked a warranty expense for $900 when you xed inventory parts. How long is the warranty on these parts? We need to know if there is a possibility that you will continue to have to cover future repairs on the parts you sold this past year. We have a three-year warranty on these parts. We don't expect to have many repairs, but if needed. we will always replace or repair any parts over the three-year warranty period. 9. if this is a three-year wananty, we need to estimate the cost that will be incurred to fulll the warranties on ail equipment sold this past year. We need to make sure that we get the applicable warranty expense accrued in the same year the sates were made. Can you come up with an estimated amount for the three-year warranty period? Actually, we discussed that just last week. but I did not think it had to go on the current year's nancials. Over the three year warranty period, we expect to spend about 2% of the cost of parts sold. l have no idea how to record that before we actually incur the costs, to. We noticed a big increase in the ofcer salaries--is HydroQual still in compliance with the loan covenants? Also, it appears that you did not aoiust the short term portion of the truck loan due in 2OX4 ? The Bank approved salary increases for both Ms. Mallard and Mr. Bailey. No other covenant is in question since our current ratio is almost at 2.0 and our long-ten'n liabilities-to- equity ratio is very low this year. I guess I forgot to adjust the short-term portion of the long- tenn debt. 11. We noticed a reduction in other salaries. Did someone leave? Annie, our assistant bookkeeper resigned last year, which means I have been doing all her work and mine ever since. However, thankfully, Rick's wife Rochelle has bookkeeping experience and has agreed to help me with the bookkeeping starting this January at the same rate of pay that Annie was makingalthough, come to think of it, she has not done anything yet. Also, they decided that to be fair, they would pay Kay's partner Pat the same amount we pay Rochelle. Pat won't actually be doing a specicjob for HydroQuaI, but he often accompanies Kay on business trips to meet with potential new customers and they don't want him to think his contributions in this respect are not valuable. You might want to talk to Rick and Kay about this if you have more questions. Actually, I am wondering if they ran this past our loan ofcer at the Bank, 12. Have there been any changes in the advance pay maintenance contracts? We added one new advance pay contract with a start date of 6/1/X3. It is for $126,000. All other advance pay contracts remain the same. We also have three other new contracts that are billed monthly at $16,400; $12,500; and $11,000; respectively, after service is performed. Here is the schedule you asked for: Original Term Beginning AIR Total Cash Advanced Months Earned # Payments Ending A/R Contract # Contract Term Months Payment Arrangement Balance Received Payment Collections In Current Year Received Balance 2/1/X1-1/31/X2 12 End of Month Payment $25.000 $150,000 12 $25,000 $12,500 2 2/1/X1-1/31/X2 12 End of Month Payment $13,000 $130,000 12 TO $39,000 $13,000 3 2/1/X1-1/31/X2 End of Month Payment $11.500 $138,000 12 12 $11,500 $11,500 3/1/X1-2/28/X2 End of Month Payment $10.000 $1 10.000 12 11 $20.000 $10,000 3/1/X1-2/28/X2 12 End of Month Payment $36.000 $168,000 12 14 $12,000 $12,000 5/1/X1-4/30/X2 End of Month Payment $11,500 $149.500 12 13 $0 $11,500 7 8/1/X1-7/31/X2 12 End of Month Payment $12,000 $144,000 12 12 $12,000 $12,000 8 3/1/X2-2/28/X3 Advance Payment $120.000 $120,000 12 $10,000 3/1/X2-2/28/X3 12 Advance Payment So $135.000 $135,000 12 $11,250 10 5/1/X2-4/30/X3 End of Month Payment $22,000 $121,000 12 11 $33,000 $11,000 11 12/1/X2-11/30/3 End of Month Payment $12,500 $162.500 12 13 $12,500 12 1/1/X3-12/31/X3 12 End of Month Payment SO $180.400 12 11 $16,400 $16,400 13 5/1/X3-4/30/X4 12 End of Month Payment $75,000 $25,000 $12,500 6/1/X3-5/31/X4 Advance Payment SO $126.000 $126,000 $10,500 15 10/1/X3-9/30/X4 End of Month Payment $22,000 3 2 $11,000 $11,000 $153.500 $1,931,400 $381,000 $204,90013. We noticed that you paid medical benefits this year. Does this plan include medical benefits to employees after retirement? Medical has not been promised as a postretirement benefit. We can't afford that. 14. Can you give us a copy of the new insurance policies? Did you only purchase them for one year this time? Yes, the discount was not worth paying the cash up front for those any more, so we are just doing one year at a time now. It also allows us more flexibility in shopping around for the best rates as the business grows. 15. What was included in the charges to repairs and maintenance? It seems like a lot and we may be able to capitalize some or all of those costs. Those costs were for repairs on the trucks we purchased last year and consisted of the following: Feb 12, 20X3 -- Installed special tooling on each of the two trucks $ 20,400 Various dates -- Tires, tune-ups, and other repairs $ 1,834 16. Did these costs increase the useful life or the efficiency of the trucks? None of these costs affected the useful life of the property, but the trucks are definitely more efficient now, since we really needed the tooling to do the work needed for several of our new customers.17. When will the actuarial and trustee reports on the pension plan be available? In the meantime, can you provide us with a summary of these reports, as well as a description of the defined benefit plan? Specifically, we need the service cost for 20X3. We also need to know if you set the plan up such that you have prior service costs? Also, we need to know what your discount rate is, the return on your plan assets, and the expected rate of compensation increase for future years. And, we need to know the fund allocation percentages for the plan assets you have invested. The plan was adopted on January 1, 20X3, and all employees were granted benefits for prior service. This action immediately created a projected benefit obligation of $210,650. HydroQual immediately contributed $170,000 to the plan. In 20X3 employees earned benefits resulting in a service cost of $130,900. On December 31, 20X3, HydroQual provided additional funding in the amount of $140,000. Interest on the PBO that was outstanding all year long was accrued at 3.5 percent. The return on plan assets invested in January was expected to approximate 10 percent. The plan is administered by the trust department of Midwest American Bank. The plan assets are invested in exchange-listed equity securities (35%), corporate bonds (25%), and U. S. government bonds (40%). I don't know how to compute pension expense, so I just expensed the cash payments. There was one other interesting thing about this pension plan. They set it up with an expected rate of compensation increase of 4 percent, yet I did not get a raise at all this year. 18. We noticed that the wages payable at year end doubled this year. Didn't you close up during the holidays this year? We would like to see the time cards for this accrual again this year. Yes, we did close up, but we are now in a position where we can pay our employees for those days we are closed. As a result, the wages payable balance is the normal amount for a two week period at year end. I can give you the time cards and the schedule showing the normal pay for the days we were closed. We based our calculation for the accrued December wages on both of those items this year

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts