Answered step by step

Verified Expert Solution

Question

1 Approved Answer

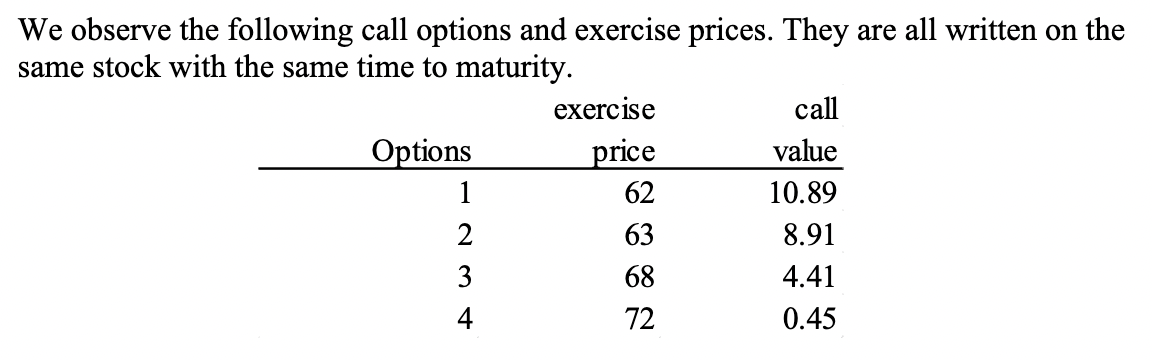

We observe the following call options and exercise prices. They are all written on the same stock with the same time to maturity. exercise call

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Course In Derivative Securities

Authors: Kerry Back

2005th Edition

3540253734, 978-3540253730