Question

Whaley Crop purchased property coverage with a minimum premium of 100% from Zurich during a hard market. 4 months later, market pricing softenedand Whaley suggested

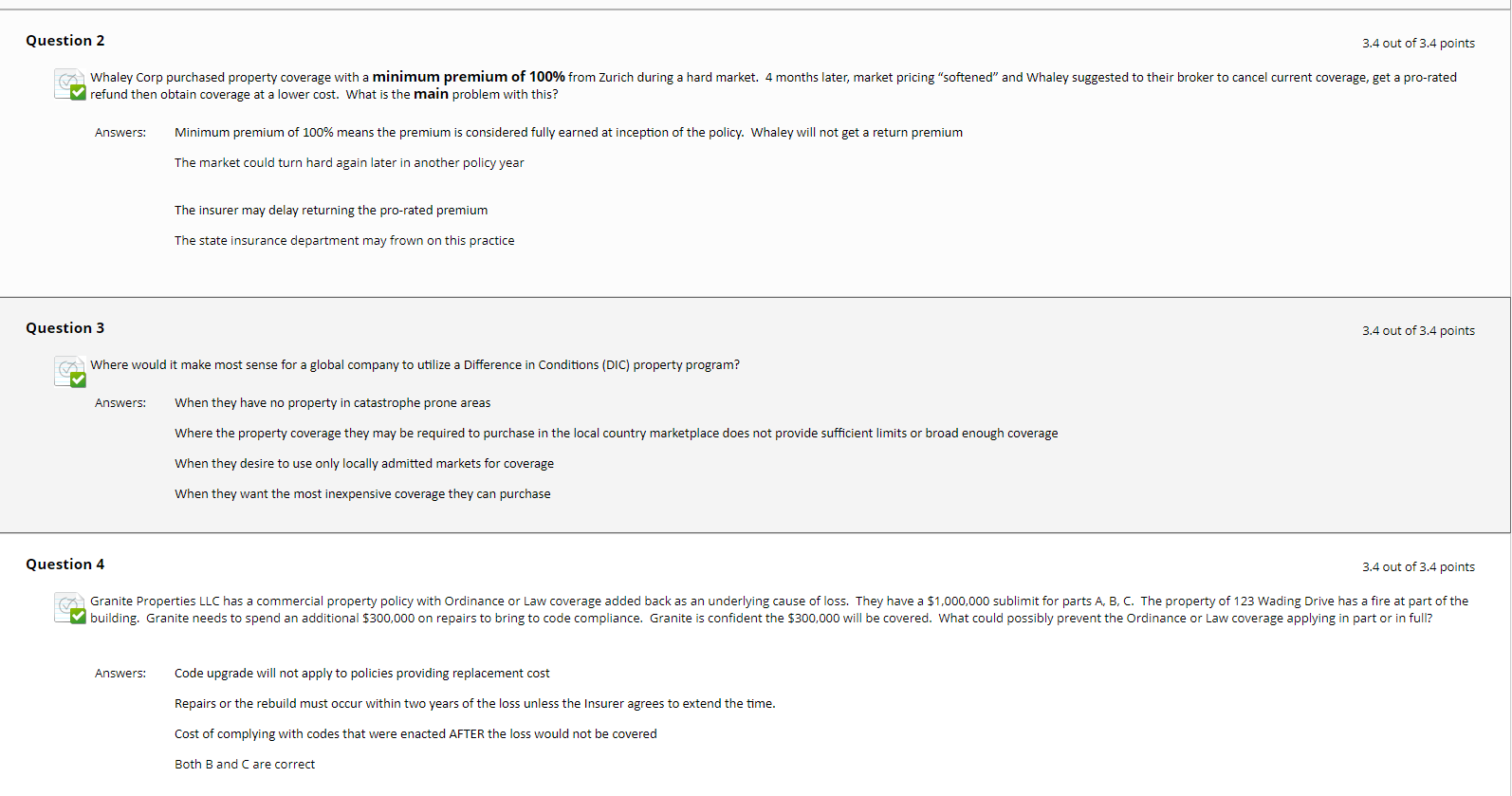

Whaley Crop purchased property coverage with a minimum premium of 100% from Zurich during a hard market. 4 months later, market pricing "softened"and Whaley suggested to their broker to current coverage, get a pro-rated refund the obtain coverage at a lower cost. what is the main problem with this?

minimum premium of 100% means the premium is considered fully earned at inception of the policy. Whaley will not get a return premium

the market could turn hard again later in another policy year

the insurer may delay returning the pro-rated premium

the state insurance department may frown on this practice

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: Strayer University

1st Edition

0470603526, 978-0470603529