What do you mean by yes?? The due date has passed now

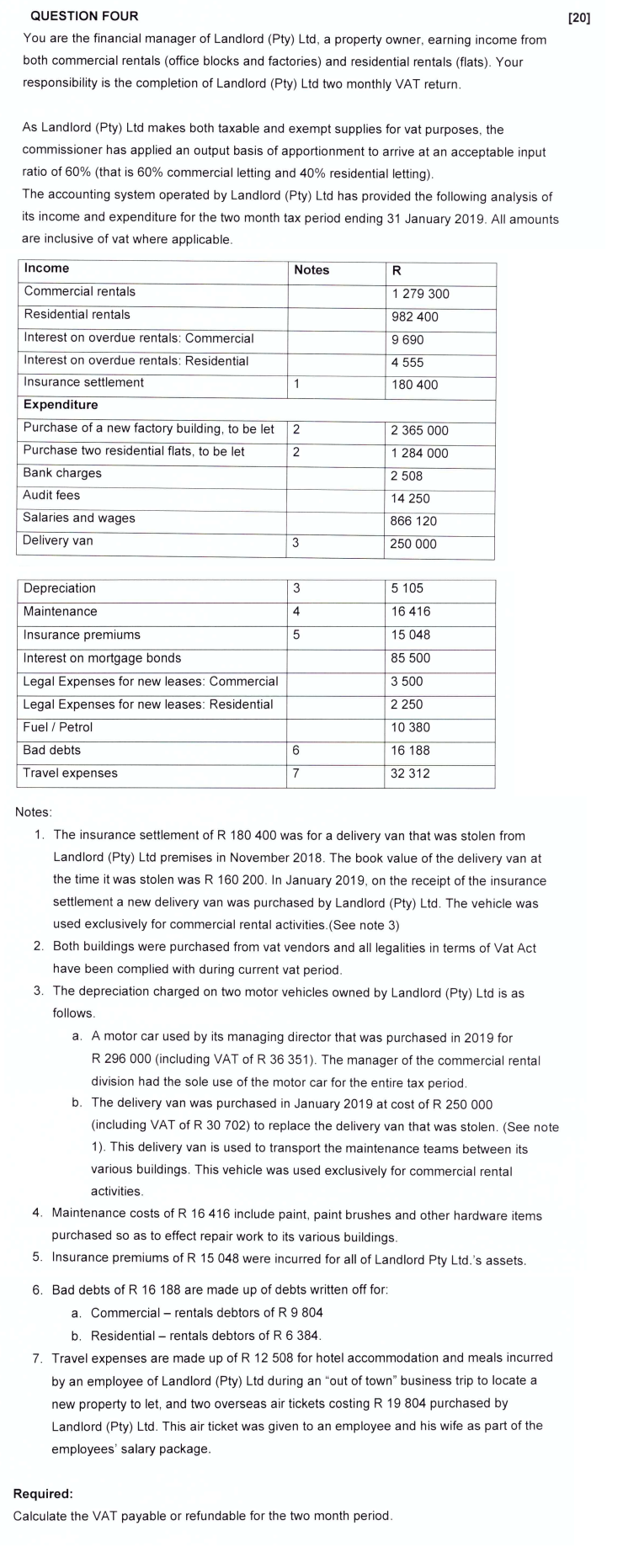

[20] QUESTION FOUR You are the financial manager of Landlord (Pty) Ltd, a property owner, earning income from both commercial rentals (office blocks and factories) and residential rentals (flats). Your responsibility is the completion of Landlord (Pty) Ltd two monthly VAT return. As Landlord (Pty) Ltd makes both taxable and exempt supplies for vat purposes, the commissioner has applied an output basis of apportionment to arrive at an acceptable input ratio of 60% (that is 60% commercial letting and 40% residential letting) The accounting system operated by Landlord (Pty) Ltd has provided the following analysis of its income and expenditure for the two month tax period ending 31 January 2019. All amounts are inclusive of vat where applicable. Notes 1 279 300 982 400 9 690 4 555 180 400 Income Commercial rentals Residential rentals Interest on overdue rentals: Commercial Interest on overdue rentals: Residential Insurance settlement Expenditure Purchase of a new factory building, to be let Purchase two residential flats, to be let Bank charges Audit fees Salaries and wages 2 2 365 000 1 284 000 2 508 14 250 866 120 Delivery van 250 000 Depreciation Maintenance Insurance premiums Interest on mortgage bonds Legal Expenses for new leases: Commercial Legal Expenses for new leases: Residential Fuel / Petrol Bad debts Travel expenses 5 105 16 416 15 048 85 500 3 500 2 250 10 380 16 188 32 312 Notes: 1. The insurance settlement of R 180 400 was for a delivery van that was stolen from Landlord (Pty) Ltd premises in November 2018. The book value of the delivery van at the time it was stolen was R 160 200. In January 2019, on the receipt of the insurance settlement a new delivery van was purchased by Landlord (Pty) Ltd. The vehicle was used exclusively for commercial rental activities. (See note 3) 2. Both buildings were purchased from vat vendors and all legalities in terms of Vat Act have been complied with during current vat period. 3. The depreciation charged on two motor vehicles owned by Landlord (Pty) Ltd is as follows. a. A motor car used by its managing director that was purchased in 2019 for R 296 000 (including VAT of R 36 351). The manager of the commercial rental division had the sole use of the motor car for the entire tax period. b. The delivery van was purchased in January 2019 at cost of R 250 000 (including VAT of R 30 702) to replace the delivery van that was stolen. (See note 1). This delivery van is used to transport the maintenance teams between its various buildings. This vehicle was used exclusively for commercial rental activities 4. Maintenance costs of R 16 416 include paint, paint brushes and other hardware items purchased so as to effect repair work to its various buildings. 5. Insurance premiums of R 15 048 were incurred for all of Landlord Pty Ltd.'s assets. 6. Bad debts of R 16 188 are made up of debts written off for: a. Commercial - rentals debtors of R 9 804 b. Residential rentals debtors of R 6 384. 7. Travel expenses are made up of R 12 508 for hotel accommodation and meals incurred by an employee of Landlord (Pty) Ltd during an "out of town" business trip to locate a new property to let, and two overseas air tickets costing R 19 804 purchased by Landlord (Pty) Ltd. This air ticket was given to an employee and his wife as part of the employees' salary package. Required: Calculate the VAT payable or refundable for the two month period. [20] QUESTION FOUR You are the financial manager of Landlord (Pty) Ltd, a property owner, earning income from both commercial rentals (office blocks and factories) and residential rentals (flats). Your responsibility is the completion of Landlord (Pty) Ltd two monthly VAT return. As Landlord (Pty) Ltd makes both taxable and exempt supplies for vat purposes, the commissioner has applied an output basis of apportionment to arrive at an acceptable input ratio of 60% (that is 60% commercial letting and 40% residential letting) The accounting system operated by Landlord (Pty) Ltd has provided the following analysis of its income and expenditure for the two month tax period ending 31 January 2019. All amounts are inclusive of vat where applicable. Notes 1 279 300 982 400 9 690 4 555 180 400 Income Commercial rentals Residential rentals Interest on overdue rentals: Commercial Interest on overdue rentals: Residential Insurance settlement Expenditure Purchase of a new factory building, to be let Purchase two residential flats, to be let Bank charges Audit fees Salaries and wages 2 2 365 000 1 284 000 2 508 14 250 866 120 Delivery van 250 000 Depreciation Maintenance Insurance premiums Interest on mortgage bonds Legal Expenses for new leases: Commercial Legal Expenses for new leases: Residential Fuel / Petrol Bad debts Travel expenses 5 105 16 416 15 048 85 500 3 500 2 250 10 380 16 188 32 312 Notes: 1. The insurance settlement of R 180 400 was for a delivery van that was stolen from Landlord (Pty) Ltd premises in November 2018. The book value of the delivery van at the time it was stolen was R 160 200. In January 2019, on the receipt of the insurance settlement a new delivery van was purchased by Landlord (Pty) Ltd. The vehicle was used exclusively for commercial rental activities. (See note 3) 2. Both buildings were purchased from vat vendors and all legalities in terms of Vat Act have been complied with during current vat period. 3. The depreciation charged on two motor vehicles owned by Landlord (Pty) Ltd is as follows. a. A motor car used by its managing director that was purchased in 2019 for R 296 000 (including VAT of R 36 351). The manager of the commercial rental division had the sole use of the motor car for the entire tax period. b. The delivery van was purchased in January 2019 at cost of R 250 000 (including VAT of R 30 702) to replace the delivery van that was stolen. (See note 1). This delivery van is used to transport the maintenance teams between its various buildings. This vehicle was used exclusively for commercial rental activities 4. Maintenance costs of R 16 416 include paint, paint brushes and other hardware items purchased so as to effect repair work to its various buildings. 5. Insurance premiums of R 15 048 were incurred for all of Landlord Pty Ltd.'s assets. 6. Bad debts of R 16 188 are made up of debts written off for: a. Commercial - rentals debtors of R 9 804 b. Residential rentals debtors of R 6 384. 7. Travel expenses are made up of R 12 508 for hotel accommodation and meals incurred by an employee of Landlord (Pty) Ltd during an "out of town" business trip to locate a new property to let, and two overseas air tickets costing R 19 804 purchased by Landlord (Pty) Ltd. This air ticket was given to an employee and his wife as part of the employees' salary package. Required: Calculate the VAT payable or refundable for the two month period