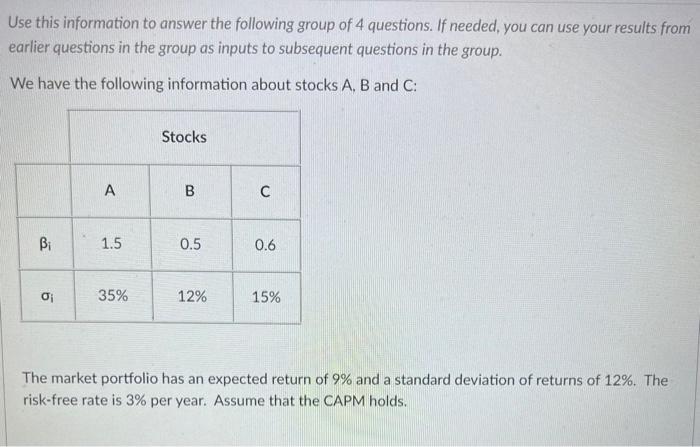

Question

What is the beta of a portfolio that invests 35% in A, 35% in B, 10% in C and 20% in the riskless asset? When

What is the beta of a portfolio that invests 35% in A, 35% in B, 10% in C and 20% in the riskless asset?

When performing the calculations, do not round any inputs or interim results until you get the final answer.

Round your final answer to four places after the decimal point.

What is the expected return for that portfolio?

When performing the calculations, do not round any inputs or interim results until you get the final answer.

Round your final answer to four places after the decimal point.

If you create a mean-variance efficient portfolio that has the same expected return as that portfolio, what is the standard deviation of this new portfolio?

When performing the calculations, do not round any inputs or interim results until you get the final answer.

Round your final answer to four places after the decimal point.

Suppose that the correlation between the returns of A and B is 0.25. What is the standard deviation of another portfolio that invests 1/4 in A, 1/4 in B and 1/2 in the riskless asset?

When performing the calculations, do not round any inputs or interim results until you get the final answer.

Round your final answer to four places after the decimal point.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Communication Essentials For Financial Planners

Authors: John E. Grable

1st Edition

1119350786, 978-1119350781