Question

What is the expected return of the optimal risky portolio? What is the standard deviation of the optimal risky portfolio? How much should Mrs Moneybags

What is the expected return of the optimal risky portolio?

What is the expected return of the optimal risky portolio?

What is the standard deviation of the optimal risky portfolio?

How much should Mrs Moneybags invest in Stock FundA?

How much should Mrs Moneybags invest in Stock FundB?

How much should Mrs Moneybags invest in T-bills?

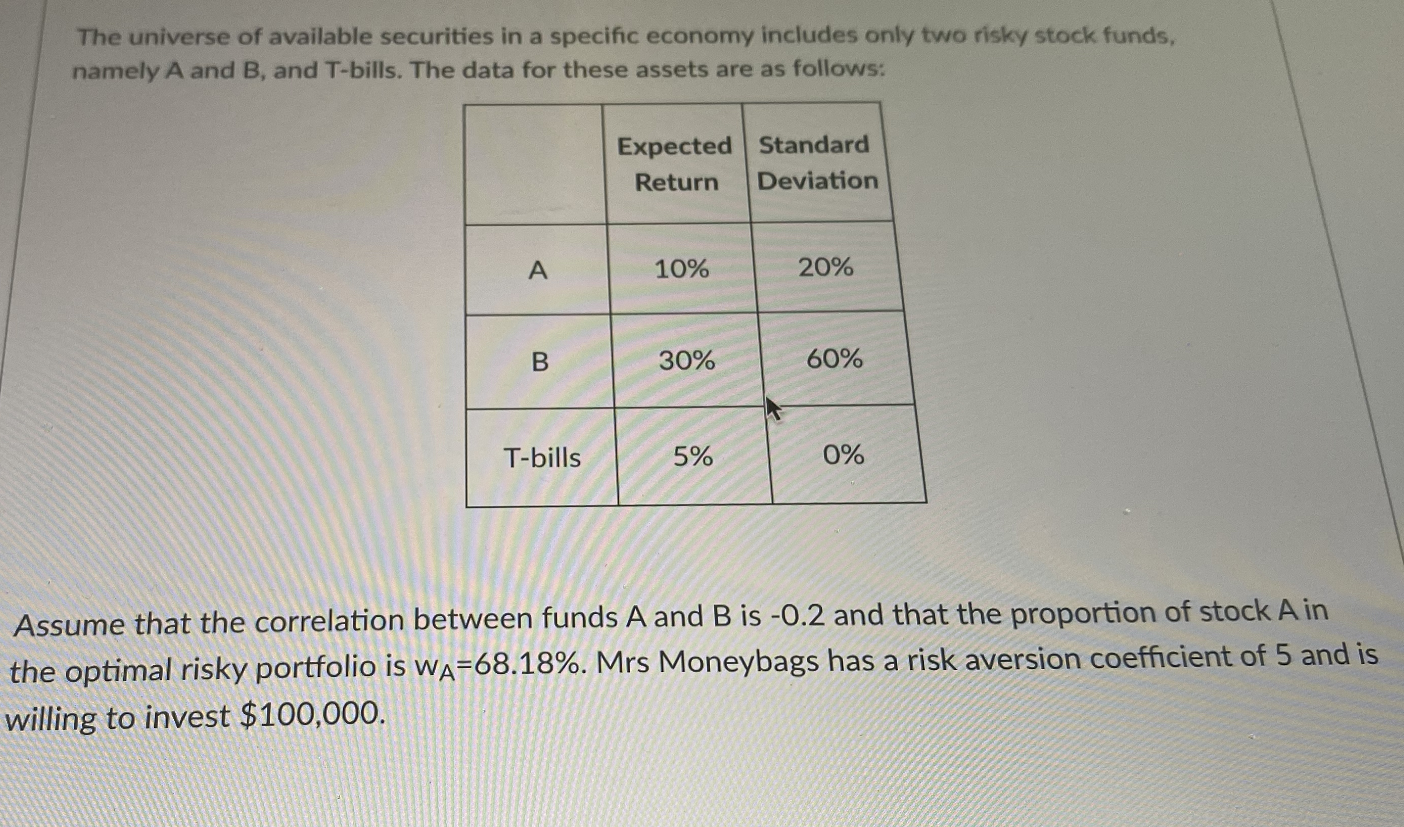

The universe of available securities in a specific economy includes only two risky stock funds, namely A and B, and T-bills. The data for these assets are as follows: Expected Standard Return Deviation A 10% 20% B 30% 60% T-bills 5% 0% Assume that the correlation between funds A and B is -0.2 and that the proportion of stock A in the optimal risky portfolio is wa=68.18%. Mrs Moneybags has a risk aversion coefficient of 5 and is willing to invest $100,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Lombard Street A Description Of The Money Market

Authors: Walter Bagehot

1st Edition

1504017293