Answered step by step

Verified Expert Solution

Question

1 Approved Answer

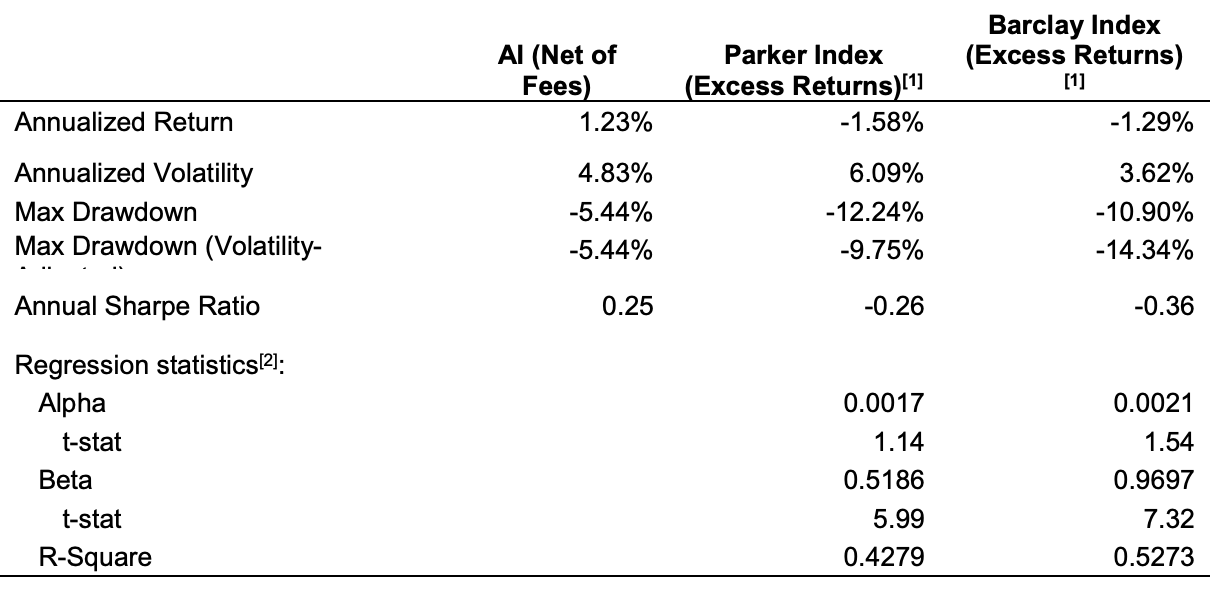

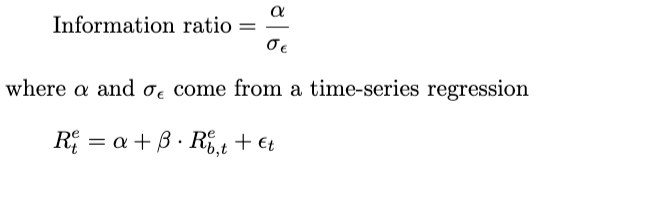

What is the information ratio of TOM using the Barclay Index as the benchmark? begin{tabular}{lrrr} & Al (Net of Fees) & Parker Index (Excess Returns)

What is the information ratio of TOM using the Barclay Index as the benchmark?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Growth Linked Securities

Authors: John Williamson

1st Edition

3319683322,3319683330